Update – Doctor of Credit has learned some positive news regarding changes for existing Preferred Rewards members: they will retain their current status until 3 months after their first anniversary date post-November 1, 2026. For example, if your anniversary date is 10/1, your 3-month clock won’t start until 10/1/27, and you will keep your current status level through 1/1/28 (provided you meet the current qualification requirements). That’s a bit of a band-aid on a broken leg, but it’s a much better timeframe than what we originally thought.

~~~Original Post Follows~~~

Bank of America tends to fly under the radar when it comes to travel credit cards despite issuing cards for Alaska Airlines/Atmos Rewards, Air France/KLM Flying Blue, Spirit Airlines, and more. A key reason for that is the lack of a transferable points program.

Where it has often drawn people’s attention is when it comes to cashback earnings, particularly due to the way it’s been possible to juice your earning rate by having status in its Preferred Rewards program. If you had high enough status in that program, you could earn 2.625% cashback on all spend on some cards which, historically, had been a very good return.

A few weeks ago, Bank of America started sending out notices to existing Preferred Rewards customers to advise them that changes to the program would be coming soon. Details were vague at the time, but they’ve now provided more details and some people are going to be disappointed.

Program name change

From May 2026, the rewards program will be rebranding from ‘Bank of America Preferred Rewards’ to ‘BofA Rewards’. That BofA branding decision is a bit of a curious choice. Some might say it’s nuts given its context in modern popular culture (I apologize in advance if you were previously unaware of this context).

Branding aside though, what truly matters is how this will affect eligibility in the program and its associated benefits.

Current Preferred Rewards eligibility requirements

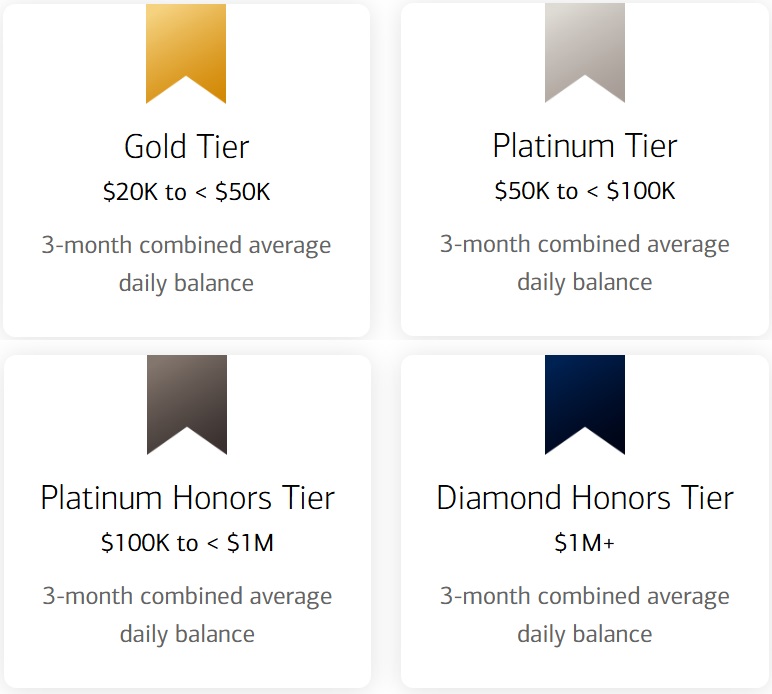

At present, you need to have enough money on deposit in Bank of America accounts and/or Merrill investing balances to earn Preferred Rewards status. The current status tiers and eligibility requirements for the Preferred Rewards program are as follows:

- Member – <$20K

- Gold – $20K to <$50K

- Platinum – $50K to <$100K

- Platinum Honors – $100K to <$1 million

- Diamond Honors – $1 million+

Each tier offers a range of benefits that may be of interest to people, such as waived monthly fees on select checking accounts, discounted mortgage origination fees, and discounted HELOC interest rates.

For many people, it was the bonus earnings available on credit cards that made Preferred Rewards status more worthwhile. Here’s the bonus you’ve historically received at each status level:

- Gold – 25% bonus

- Platinum – 50% bonus

- Platinum Honors – 75% bonus

- Diamond Honors – 75% bonus

It’s that 75% bonus tier for Platinum Honors status that’s been most appealing for people with large enough deposits with Bank of America and/or Merrill. That’s because it’s turned cards that earn 1.5% cashback into cards that earn 2.625% cashback. (n.b. there are some Bank of America credit cards that can earn more than 1.5% cashback, but those all have relatively low caps.)

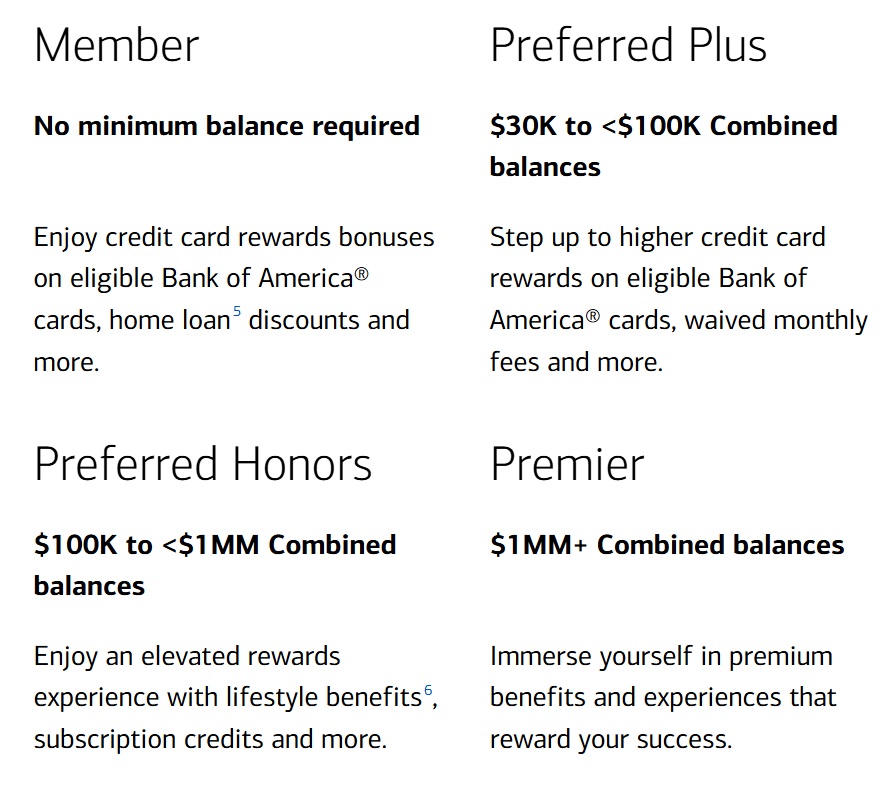

New BofA Rewards eligibility requirements

Under the new BofA Rewards program, the number of status tiers above member level will be reduced from four to three. Deposit requirements will be set higher in order to access the rewards program in the first place, while the bonus earning rates will be slashed for those who currently have Platinum or Platinum Honors status.

Here are the new eligibility requirements:

- Member – <$30K

- Preferred Plus – $30K to <$100K

- Preferred Honors – $100K to <$1 million

- Premier – $1 million+

Existing Gold and Platinum members will be mapped to the new Preferred Plus status, Platinum Honors members will become Preferred Honors members, while Diamond Honors members will become Premier members. For existing Gold members, it’s worth being aware that the required minimum balance on deposit with the bank will be increasing from $20,000 to $30,000.

For existing Gold members, the new Preferred Plus status won’t be a downgrade when it comes to credit card earnings as you’ll still get a 25% bonus. It’s the next two status levels where these changes will sting.

Existing Platinum members will also be getting swept into the Preferred Plus status tier. As a result, you’ll also only earn a 25% bonus from May 2026, rather than the 50% bonus that you currently receive. At present, a 1.5% cashback earning card earns you 2.25% cashback; in the future, that’ll drop to 1.875% – a significant difference.

Platinum Honors members will likely feel even more aggrieved. The credit card bonus rate will be slashed from 75% to 50%. That means your 1.5% cashback card that currently gets boosted to 2.625% everywhere thanks to your Preferred Rewards status will only earn 2.25% cashback under the revamped BofA Rewards program. That reduced earning rate could make a material difference in people’s willingness to put spend on their Bank of America cards rather than a card that earns two transferable points per dollar with select American Express, Citi, Capital One, or Bilt cards.

Although the new status tiers will come into play from May, some of your existing benefits won’t change immediately. For example, in the FAQs it states the following:

Some benefits, like the credit card rewards bonus and no-fee safe deposit boxes, may be subject to change. If this applies to you, you’ll keep your Preferred Rewards benefits for at least 6 months (after May 2026).

That means Platinum and Platinum Honors members will still get the 50% and 75% bonuses respectively through November 2026. That gives you nine months from now to plot your course forward.

New BofA Rewards benefits

There’ll apparently be select new benefits for some BofA Rewards status tiers. For example, there’ll be a subscription credit for Preferred Honors and Premier members which is described as follows:

In order to be eligible for the subscription credit benefit, you must: (1) Be enrolled in the BofA Rewards program’s Preferred Honors or Premier tiers (2) Agree to the full terms of the Subscription Credit Benefit via the Subscription Credit Benefit page within BofA Rewards and (3) Make payments directly to eligible merchants using your Bank of America debit card linked to a checking account that you designate via the subscription credit benefit page. Customers may receive statement credits up to $8 per month for Preferred Honors members and $15 per month for Premier members. Eligible merchants are subject to change without notice. Currently eligible merchants can be found on the subscription credit benefit page.

It remains to be seen as to what type of subscriptions will be eligible for these credits.

Preferred Rewards for Business – no changes, so a good workaround?

At present, there’s nothing indicating that Bank of America will be making imminent changes to the business version of the Preferred Rewards program, appropriately called Preferred Rewards for Business.

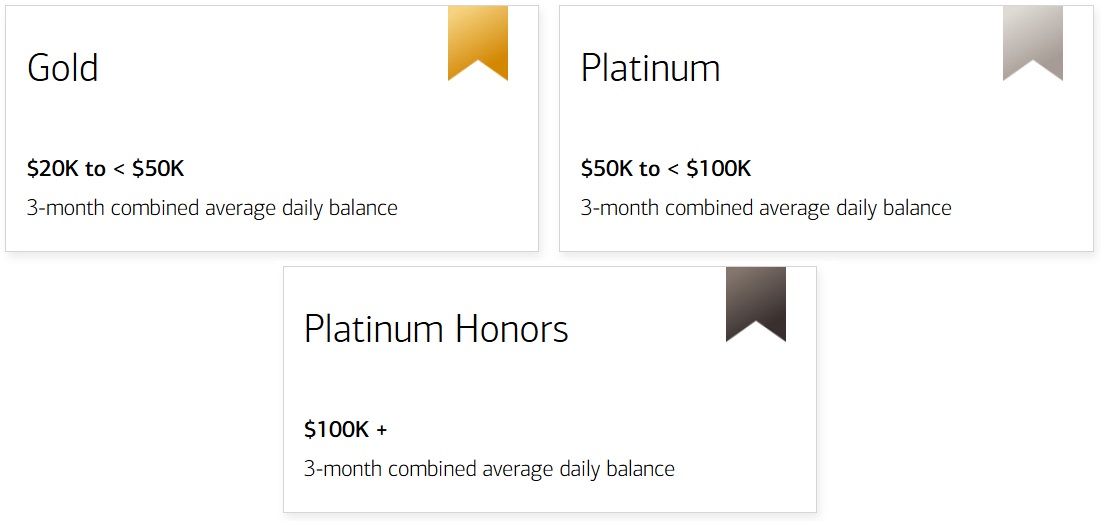

As a reminder, here are the Preferred Rewards for Business requirements:

As you can see, the existing requirements on the personal side map across to the business side identically, albeit without a Diamond Honors level on the business side. If you’re currently a Platinum or Platinum Honors member with your personal accounts and could shift those deposits to business accounts instead, this would be a (somewhat) easy workaround to maintain your existing credit card bonus rates of 50% and 75% respectively.

If you did proceed in this manner, you’d also need to get a business credit card that earns 1.5% cashback everywhere if you want to continue earning 2.625% on all unbonused spend as a result of your status.

Your Thoughts?

Will these Bank of America Preferred Rewards/BofA Rewards changes affect you? Will you be changing your approach as a result, whether that means depositing more money with Bank of America/Merrill, shifting to Preferred Rewards for Business, or putting your everyday spend on a different card? Let us know in the comments below.

Rakuten credit card bonuses (Bank of America boosted up to $275)")

BOA sent out a new email – they seem to have changed their dates? I am currently in the 75% bonus 100k plus…

Future changes to your credit card bonus:

Your 50% card bonus will continue until your next BofA Rewards anniversary in September 2027 and then be reevaluated based on your tier. If you remain in the Preferred Honors tier, your card bonus will become 50%.

I assume if your post above was correct this should read

“Your 75% card bonus will continue until your next BofA Rewards anniversary in September 2027 and then be reevaluated based on your tier. If you remain in the Preferred Honors tier, your card bonus will become 50%.”

Its all pretty confusing tbh

Same for me. Unfortunately.

US Bank Smartly 4% for everything except Taxes and Insurance. Have to stay with BofA for the taxes and insurance.

However, there is a monthly cap of 20k.

In process to get a home loan with BOFA as a Diamond tier member (1m+ in assets). I own a home 3M free and clear.

New Home is 3,3M. I have 2.0M in cash + equities with ML. I make 400K+ a year. Bank called me today, 2 days before loan contingency is due that I do not qualify as my DTI is too high.

Just plain ridiculous.

Scrambling to get a plan B now.

I would not pay much attention to this prefer rewards and empty promises.

what about the Chase business Premier card that give 2.5% cash back on purchases over $5000?

Like Tom, I keep 100k in an IRA at Merrill and get 2.625c cash back.

But before we get worried, look at the numbers.

Platinum Honors 2.625-2.25 = 0.375% difference

Platinum 2.25-1.875 = 0.375% = SAME DROP (unlike the article above)

On $1M spend, (not too many do above that I hope) the difference is $26250 vs $22500 = $3750

For 100k in non-bonus spend each year = typical = 375$ – not much to worry about

Real options are

A

Flexible currencies

Citi or Cap 1 with transferable points @ 2c each vs 2.25c below

B

IRA 100k at BofA with 2.25% Preferred

= $22500 per Million spend = $2250 extra cash vs (20k cash /2M points)

for typical 100k spend each year = $225 cash loss vs having option of 200k points

C

Business at 100k Savings Account = 3% interest – itself has lost cash or investment opportunity – Unlike an IRA, this account will have a real cost – say 3% in return

to get even 1M spend = gain $3750 and lose 3000 – really not worth it.

Between B & C, B wins for simplicity

Between A & B – I suspect that depends on your balances in Citi and Capital One

I will likely change my Venture X to a Cash Plus 2% card for flexibility

or look more closely at Bilt

For typical 100k spend each year – just get SUB from every card slowly and steadily

Right now I keep $100,000 in a Merrill Edge Roth IRA to get the 2.62% cash back, even though I am not impressed with Merrill and prefer Fidelity. I don’t know of a way to get tax-advantaged assets into a Merrill Business account to get to the $100,000 mark. As far as I can tell, if one has a sole-prop Roth 401K with Merrill, there are a lot of fees that eat into the value of the account and cancel out the benefits of 2.62% on the credit cards. But if I am missing something here I definitely want to know. A Frequent Miler post on the best way to keep $100,000 or more with Bofa/Merrill to get 2.62% on the business side would be very worth reading–a future post suggestion? Is the only option $100,000 or more in taxable assets if one wants 2.62% on the business side without fees? Fellow Frequent Miler followers, please let me know. Thank you.

Before expending energy on the business side, ask yourself what the likelihood is that BofA does NOT update the business side as well. I’d hate for you to go through the process only to have it change as well. Like Han Solo, I got a bad feeling about this.

Well luckily now it seems you may have up to 2 years to figure it out. Hopefully you don’t have a November-January anniversary date

By that point we should be able to tell if they’re nerfing business accounts

Not if your anniversary date falls after 11/1. Mine is in December. So my rewards will be nerfed in next February.

The biggest question for me is will the UA TravelBank continue to work for there premium rewards travel card. By making it “free” a card that can to 3% dining/travel and 2.25 catch all is great for simplicity. If that goes away then that plus the rewards nerf is tough to take…

Some recent reports have indicated success and others have indicated failure. Wait for more data points.

To get 4.5% on “online purchases” which is a wide swath of anything bought through a computer or a mobile wallet is still tremendous, even if it is limited to $2500 per quarter per card. Many people have three, four, or more CCRs so that accounts for a majority of regular spending. I will still move some assets in to qualify for 2026 and into the first part of 2027 to the $100k level, but after status runs out in 2027 I will evaluate what is out there then. Maybe it will be a combination of Robinhood 3%, category cards, and whatever sign up bonus I am trying to hit.

where to move for cashback? the sketchy Robinhood 3% card?

See link below

US Bank Smartly

Smartly is awful now if you aren’t grandfathered in

You need to waste money letting a ton of cash sit in a no real interest checking account now

Don’t feel bad. Now that BOA is reducing their % rate, I’m sure that US bank will follow….

I love my Robinhood card. Not sure what’s all the hate is about. I now only use my BoA Premium Rewards card for dining (which includes gift cards bought on DoorDash) for 4.5% cash back.

BofA will absolutely nerf preferred rewards for business. No one said they were required to do it all at same time. Besides, the business version is already to easy/generous.

Definitely no reason to bank with BofA now.

Yet another reason to bail on Bank Of America. 2.25% is better than 2% cash at Citibank but is it better than 2 pts /dollar at Cap One?

You’re talking about an extra 0.25% on how much spending? Whatever that number is, is it worth the effort of maintaining the relationship? Only you can answer that.

2.625% back on 100K in annual spend was pretty good.

citi typ is way more valuable than cap one. dcb plus citi premier is a better combo than cap one venture x

P2 and I have a 4 card setup at Citi – 1 Doublecash, 1 custom cash, 1 Premier, 1 Elite. Great coverage to generate TYP and the AA passes are hugely valuable to us.

The Citi strata elite only offers four individual AA lounge passes each year. My wife and I burned ours on one roundtrip ticket last month. Nice but not incredibly valuable.

They are when you’re bringing kids in! They cover one adult and minors with just one pass. I also fly out of O’Hare where PP, C1, Centurion blah blah blah all don’t exist so I legit love those passes.

As a small business owner I have seen BofA seemingly do anything they could to alienate customers, but I have stuck with them. This will cause me to end my business and personal relationship with them.

https://www.reddit.com/r/CreditCards/wiki/list_of_flat_cashback_cards_with_benefits/

For those looking for pure cash back.

Stephen, you mention an easy work around changing the personal100k account to a business account to keep the 2.6% but wouldn’t there be tax issues involved?

I am not an accountant, but I believe earnings on business accounts can be included on one’s personal return. I treat my BoA business account as a personal account for tax purposes.

Thank you

On the up side, maybe commenters will stop advising people to “just get the 2.65% card.”