There’s an oft-repeated joke in travel circles that goes something like this: “Want to know what United is planning for next year? Look at what Delta did last year.”

Yesterday, United MileagePlus made significant changes to how its members earn and redeem miles. Essentially, it is following Delta’s lead in using award discounts to encourage customers to hold a United credit card, then going a step further by also giving improved earning rates on paid travel to cardholders.

As it stands, if you want to engage with United MileagePlus in any significant way, you’ll probably need a credit card.

Changes to United MileagePlus

Cardholders earn more miles; everyone else earns much less

The biggest change to the United MileagePlus program is in how miles are earned on paid flights. All United elite members who are not cardholders will see their earnings slashed by 2 miles per dollar. Cardholders’ earnings, on the other hand, increase by 1 mile for every dollar.

Here is a summary of the changes:

| Elite level | Pre-April 2 | Non-cardholder | Cardholder |

|---|---|---|---|

| Member | 5 miles/dollar | 3 miles/dollar | 6 miles/dollar |

| Silver | 7 miles/dollar | 5 miles/dollar | 8 miles/dollar |

| Gold | 8 miles/dollar | 6 miles/dollar | 9 miles/dollar |

| Platinum | 9 miles/dollar | 7 miles/dollar | 10 miles/dollar |

| Premier 1K |

11 miles/dollar | 9 miles/dollar | 12 miles/dollar |

Non-cardholders are really taking a hit here, and it’s not just the absolute numbers, but also the difference between the two: across the board, cardholders earn 3 more miles per dollar on paid flights than non-cardholders.

Note that this makes a much bigger difference the lower someone’s status is. A Premier 1K member can increase earnings by 33% with a United card; a run-of-the-mill regular member will have their earnings doubled. This is undoubtedly intentional, as United and Chase know that most elite members (especially high-level ones) probably already have a United credit card. The most in need of encouragement are the masses on the bottom rungs of the ladder.

This change makes United by far the least-rewarding major domestic airline for non-cardholders, as both Delta and American have nearly identical earning schemes to United’s previous rates.

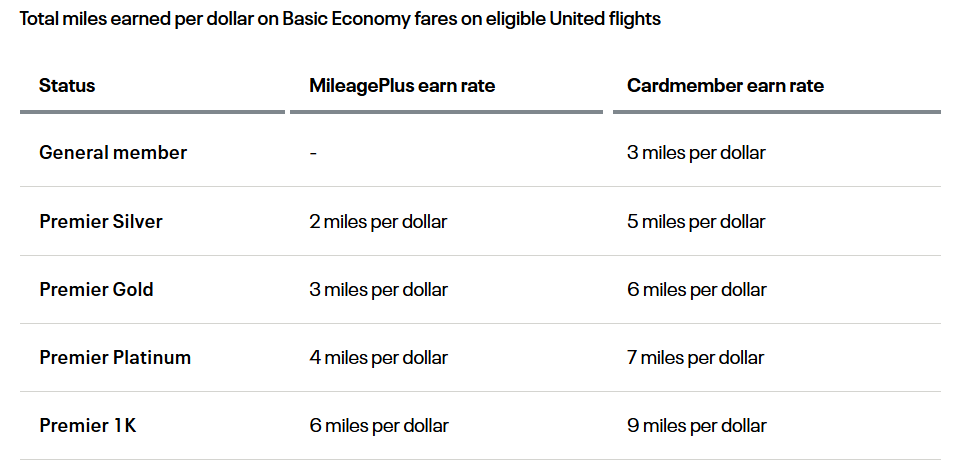

Non-cardholders earn nothing when flying basic economy

Exacerbating the earning rates themselves, United now also requires you to hold a credit card to earn miles when flying basic economy. Elite members and cardholders earn reduced rates, with both categories taking a 3-mile per dollar hit from non-basic tickets, as shown in the table below:

Cardholders will get discounts on awards and better availability

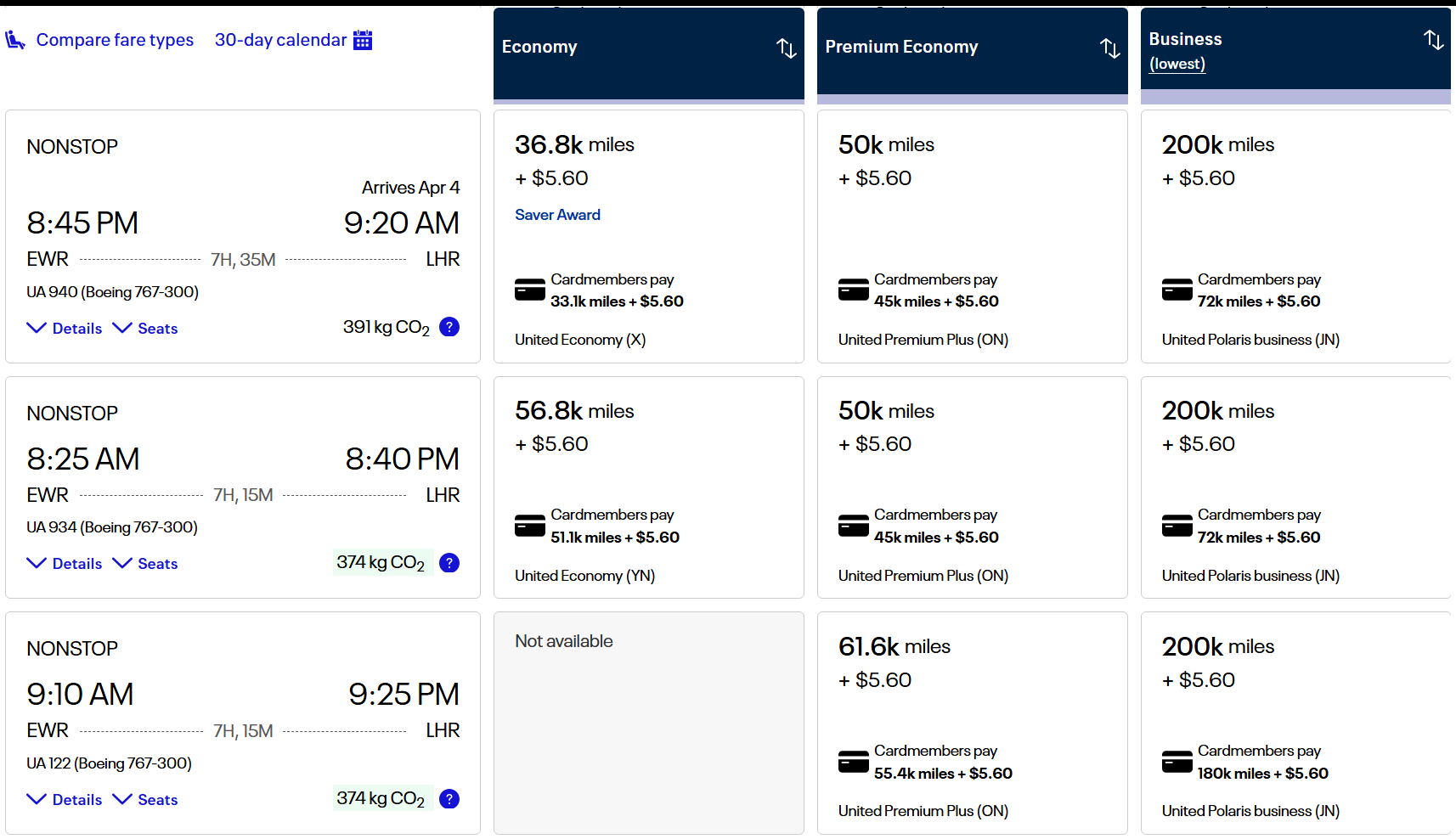

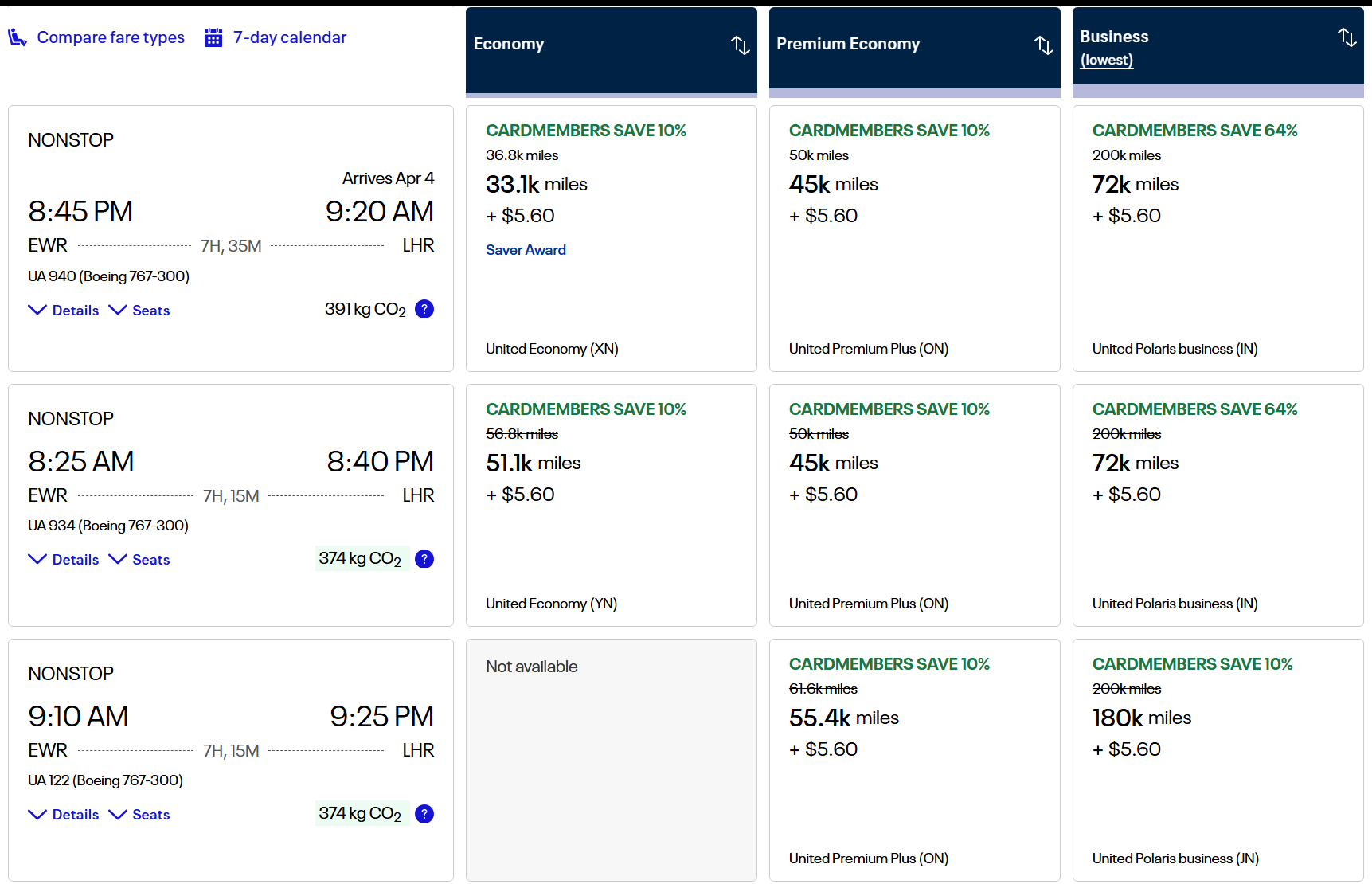

United now gives cardholders at least 10% off all award flights, similar to the 15% discount Delta offers its cardholders. United cardholders who are also elite members get a 15% discount. United is also following Delta’s lead by showing its discounted prices to everyone, regardless of whether they’re a cardholder, to juice credit card customer acquisition:

In contrast, here’s what United shows a cardholder when searching for the exact same award flights:

Not only is there an award discount, but United also says that it will increase the proportion of Polaris business-class saver awards it reserves for elite members and cardholders. From what I understand, that’s currently at ~33% of all saver awards.

Yesterday, Greg searched on a random date and found that 6 out of 7 nonstop flights between Newark and London were available at saver pricing in business class to cardholders. None were available at saver pricing to non-cardholders. Regardless of where it settles out, this change almost certainly means that non-cardholders will be fighting over fewer seats.

Quick Thoughts

This is about as surprising as a sunrise. In our points and miles forecasts for 2026, I predicted that at least one more domestic carrier would “Delta-rize” its credit card portfolio by giving award discounts to cardholders. United didn’t make me wait long, and I’ll be interested to see if American follows suit once the transition of Barclays cardholders to Citi is settled.

These days, the major domestic carriers are essentially rewards programs that happen to fly airplanes, and their credit cards are a massive revenue driver; the yearly dollars spent on Delta’s portfolio of credit cards are staggering. It only makes sense that United would try to wrangle every last customer and dollar of spend into its suite of cards.

What I find really interesting here is that United has become the first airline that I can think of to take two additional steps. First, it’s taking Delta’s card-acquisition strategy and going a step further by using cardholder status as the single biggest factor in setting earning rates on paid flights. A non-elite cardholder now earns more miles per dollar on United flights than someone with Silver status and no credit card, and that same pattern holds as you go up the elite ladder.

Second, instead of simply adding incentives to get a credit card, it’s actually punishing those who don’t by cutting their earning rates. It’s not just that cardholders earn more; non-cardholders also earn less. I’m a little surprised by that from a PR standpoint, but it creates a wider gap in benefits between those with a United credit card and those without one than what any other carrier has had the hutzpah to implement. If it works, the other carriers will undoubtedly follow suit.

United is making it clear that it cares far more about whether you have one of its credit cards than about whether you fly its airline. That’s a pretty dramatic statement.

More and more status is overrated, and these programs find ways to devalue; whether it’s by punishing non-card members (United), or via excessive redemptions (SkyPesos). I’ll naturally earn entry-level status each year with the US3, and elevated status with a few, based on annual travel plans. However, it’s not something we should be actively chasing anymore. PlusPoints and Systemwide Upgrades rarely clear. GUCs and Move to Mint are far better for confirming in-advance, but RUCs have taken a hit lately.

I’m lifetime gold and have Gateway card with historic minimal spend. My display still says “cardmembers save” but doesn’t say “cardmember’s save 10%” and indeed I don’t have access to the extra 10%. I do assume I have full access to the expanded Saver inventory but can’t prove/disprove that without seeing someone else’s search results.

Surprising United hasn’t figured some way to show people in my situation that there is further discounted pricing out there – and try to push a card upgrade or additional spend to reach the $10,000 point. (obviously I know because I follow these things closely but I assume others would not know).

I had been hoping for upgrade offers for the past few weeks but no luck. I went over $10,000 spending on the Gateway yesterday so should start seeing the additional 10% in the next few days/few weeks/soon.

Just looked up terms for the discounted pricing… As far as I can tell this is only for United operated flights, not partners. Also the no annual fee card only gets discount pricing after spending $10k in the year, cheapest card with the discount automatic is the $150 annual fee card

> “In our points and miles forecasts…I predicted that at least one more domestic carrier would “Delta-rize” its credit card portfolio by giving award discounts to cardholders. … I’ll be interested to see if American follows suit…”

Actually American invented this!

They offered a 10% award rebate to cardholders as documented on FM.

https://frequentmiler.com/10-mileage-rebate-ending-on-american-airlines-credit-cards/

When it ended, Citi stepped in to offer 10% back on ThankYou cards, which also ended a few years ago.

Everything old is new again. Let’s see how long it lasts.

So, which would be the best card for me?

1) I don’t care about earning miles by flying United paid fare.

2) I am interested only in United international business class awards.

3) I have plenty of Chase UR points to transfer to UA.

4) I don’t care about lounges as I have Centurion and Priority Passes. .

5) I need the award prices to be as low as possible (as in this example shown here). I am NOT willing to pay 200,000 miles for a trip from USA to LHR as an example, but 72K is great as well as more availability.

Obviously I don’t care much about spending on the card, and a low annual fee would be great – as well as a decent initial bonus.

To me it looks like the United Business card for 100K points and $150 annual fee.

United Airlines – “ Come spend with me “

So I sometimes have a United card for the point, but the problem is the Delta cards are actually nice cards with some useful benefits. The United card options are a bit meh. Their lower level card isn’t as useful, and their higher level card is overpriced with no realistic way to justify the annual fee unless you’re constantly flying United and need full lounge access. With access to Centurion Lounges, United lounges are not very alluring, whereas Delta tends to be as good or better than Centurion. If they’re going this route, they really also need to make their cards more attractive at the same time.

And then there’s the fact that my local hub is Delta, and I fly United only occasionally — probably isn’t going to make sense for me to have a United card unless it’s just to get a points bonus and then cancel later.

I find the UA Explorer card to be great. You get a $5 a month rideshare credit, two $50 credits each cardholder year for United Hotels, and not only the increased earnings rate but reduced price MP awards. They also run frequent promotions where you can earn bonus miles by category or by meeting some minimum spend. Is it a great card, nope but is it a must have if you plan to earn and burn on UA, absolutely!

I have a United Club Business Card, United Business Card, and Personal Quest Card. I travel with United frequently for work and frequent personal travel (homes in USA and Australia, I go back and forth about six times a year). This card lineup provides massive ROI. A summary of why I hold these,

I’m also thinking about getting and holding the personal Club card for the initial SUB bump and then overlapping credits and the extra 1,500 PQP.

does the $200 united travel bank credit on the Quest cc have the standard 5 year expiration (in other words, is it bankable so you can accrue amounts)?

It acted like other funds I’ve added to my travelbank, such as the $200 I add with my Amex Platinuk each year.

You mean the amex plat airline credits that you “use to” be able to add to your United travel bank, don’t you?….. (sad face emoje)

That’s correct! the travel bank is a bit of a dumping ground like that. Lol

Do we know if we get the old earning rates if we booked before April 2nd but travel is after April 2nd? Chatted with United and the rep contradicted themselves in the very same chat!!!

If I am looking at buying 3 united tickets with cash in the high 4 to low five figure range, should I wait till April 2nd to open an explorer card to get the higher 3 points per dollar spent? I’m confused on if the earning rate is changing for flights flown after April 2nd or if they are also changing for the earnings rate for the spend on the cards on united flights as well.

I guess now i should even fly United since i can never get the credit card due to lifetime ban from Chase

How did you get a lifetime ban?

“I guess now i should even fly United since i can never get the credit card…” Huh?? Why is it that you “should” fly them?

Curious why would they do this to business travelers who don’t have a choice but to make bookings with their business credit card (often provided by employer)

UA doesn’t require you to use the Chase UA card for paying for the ticket, you just need to have it.

Imran, I am in the same position with my employer. They make use Navan, which is an OTA for work related travel bookings. I still get my status and benefits from my UA cards even though I am not purchasing tickets using my own card. The only downside is that the my employer claims whatever points they earn from the card spend itself.

If I had zero personal travel and only business travel, I would still consider getting a UA card and keeping it in the sock drawer. Club membership (employer sadly doesn’t pay for this) is cheaper, affects upgrade priority, etc. are all benefits that come to mind.

Does this change make me more likely to get the United credit card or less likely to fly United? My first thought is that it makes me less likely to fly United.

Can one product change another chase card to the no AF United card? I might consider that. I’m sure not paying an extra $100 year in AF to earn double miles …

It says in the fine print holders of the no annual fee Gateway card have to spend $10K on the card before the cardholder benefits apply. Not worth it.

Would be nice if the cards offered alternative benefits for elites who already get free checked bags and priority boarding.

I poked around some domestic itineraries this week and found quite a few 30k roundtrips in first. If that’s an ongoing repeatable thing and I haven’t just gotten lucky, that’s a real alternative to AA on spoke to spoke value routes. They hadn’t been that low before, and they’re showing cheaper than coach when they do.

Gold for life with Gateway card. We’ll see if Saver awards become more restricted. I’m not spending 10 grand on that card. I might have to product change.