One of the best methods for gaining a large chunk of points or miles is to earn welcome bonuses on credit cards. This usually involves meeting a minimum spend requirement.

In this post we’ll be explaining what a minimum spend requirement is, potential pitfalls to be aware of, and other tips to ensure your minimum spend requirement success.

What is a minimum spend requirement?

When you apply for a credit card and there’s a welcome offer attached to it, you usually earn those bonus points or miles when spending a certain amount on the credit card within a specified amount of time. That amount you have to spend—and the time in which you have to spend it—is the minimum spend requirement.

For example, an airline might offer 75,000 bonus miles when spending $5,000 within the first 90 days on one of their credit cards. A hotel might offer 150,000 bonus points when spending $3,000 within the first 3 months on one of theirs. Meanwhile, a bank might offer 175,000 points in their transferable points currency after spending $10,000 within the first 6 months on one of their credit cards.

You might occasionally come across credit cards that don’t have a minimum spend requirement, or they have a minimal minimum. For example, at the time of writing this post, some of the Bilt and Amazon credit cards are awarding their welcome offers upon approval of the card rather than requiring any amount of spend. Somewhat similarly, the old US Airways and American Airlines Aviator Red credit cards (neither of which are available for new applications) often awarded their welcome bonuses after making a single purchase on the card and paying the annual fee. Those types of setups are far less common though as banks and loyalty programs want to incentivize you to actually spend on the card.

Tiered minimum spend requirements

You might sometimes come across minimum spend requirements that have two or more spending tiers.

For example, the IHG One Rewards Premier Business credit card sometimes awards 140,000 bonus points after spending $4,000 in the first 3 months, then an additional 60,000 bonus points after spending a total of $9,000 (i.e. an additional $5,000) in the first 6 months.

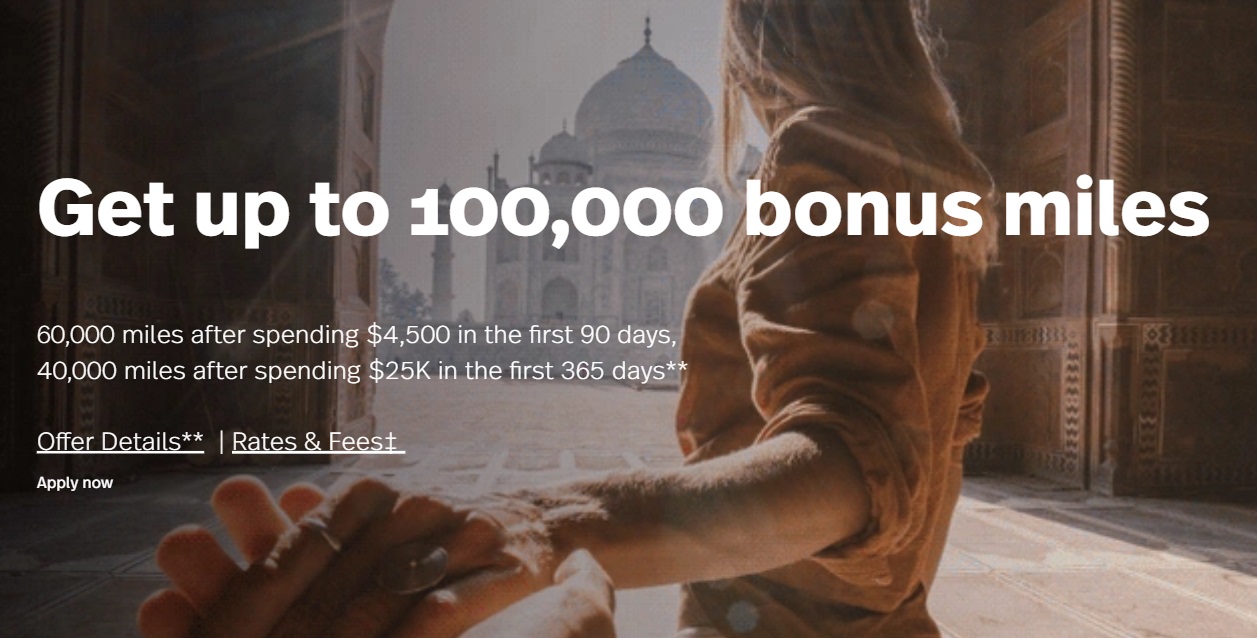

Similarly, at the time of publishing this post the avianca lifemiles American Express® Elite Card has two tiers for its welcome bonus. You earn 60,000 bonus miles after spending $4,500 in the first 90 days, with the ability to earn an additional 40,000 miles after spending a total of $25,000 in the first 365 days.

In the first example, spending all the way to the second tier would make sense for quite a few people as you’d be earning an additional 60,000 IHG One Rewards points on that additional $5,000 of spend, so an effective 12X return in addition to the card’s regular earnings whenever that particular welcome offer is in effect.

With the Avianca card example though, that’s much less of a good opportunity. After initially earning 60,000 miles by spending $4,500, you’d have to spend $20,500 more in order to earn only 40,000 additional bonus miles. That’s less than a 2X return on that spend (in addition to the card’s regular earnings) which is a poor return on a very significant amount of spend for most people.

Days vs months

The timeline you’re given to meet a minimum spend requirement is usually measured in either days or months. Most commonly you’ll be given 90 days or 3 months to hit the required spend, but sometimes it’ll be longer than that (and very occasionally shorter).

Something important to bear in mind is that 90 days isn’t the same as 3 months. For example, let’s say you apply for a credit card on June 19. If the bank gives 3 months to meet the spend requirement, you’d have until September 19 to achieve that. If you’re given 90 days though, you’d have until September 17. That’s only a two day difference, but it could make all the difference if you had in your mind that 90 days meant you had until September 19 and you left some element of the spending until the last minute.

When does a minimum spending timeline begin?

With nearly every minimum spend requirement, the clock starts from the date that you apply for the card, not the date your application is approved (if that’s different), and not the date that you activate the card.

For example, when applying for a new credit card you might get a message that your application has gone to pending review. That happened to me just the other night with Chase. I received a call from them the very next day to verify that it was indeed me who’d applied for the card. After confirming that it was, the phone agent pushed my application through and I was approved, so there was very little delay involved.

However, other times you might not hear from the bank for several days, or perhaps it’s even a week before you receive a letter in the mail stating that they need more information in order to proceed with your application. You submit that, then it’s another couple of days before it’s processed and approved. You then have to wait up to five business days for the card to arrive. That means you might’ve lost a couple of weeks in the timeline, so bear in mind that the timer doesn’t wait until you activate the card in the vast majority of cases.

Minimum spend requirement trackers

One of the most important factors in meeting a minimum spend requirement is keeping track of how much you’ve spent. Thankfully, many banks now have trackers to easily see at a glance the progress you’re making.

For example, I was approved last month for another Business Platinum Card® from American Express. I was approved on March 7 and have 3 months to spend $20,000 on the card. When logging into my Amex account and selecting that new card, this tracker is displayed (this is the version in the app; you can see something similar on the desktop site):

Here’s what the tracker looks like after completing the spend requirement on a Barclays JetBlue credit card; this can be found under the ‘Rewards & Benefits’ menu item:

Annual fees don’t count

If the bank that issued your new card doesn’t offer a tracker like that, or if you prefer to manually calculate how much you have left to spend, be sure not to include the cost of the annual fee in your calculations. Despite having to pay the annual fee, that amount paid doesn’t count towards your minimum spend.

For example, with my Amex Business Platinum card, it has an annual fee of $895. Spending $19,105 and also paying the $895 would earn me zero bonus points; I have to spend $20,000 plus pay the $895 annual fee.

Minimum spend requirement tips

Here are some tips that could make your life easier whenever you’re approved for a new credit card and have to spend a certain amount to earn the welcome offer.

Take screenshots

Whenever I’m about to apply for a new credit card, I take screenshots of the welcome offer. In fact, usually I take two. When getting ready to apply for a new card, there’s usually a landing page where the bank lists all kinds of card details, benefits, the welcome offer, etc., then there’s a button to apply and on that page the welcome offer requirements are also detailed.

I take screenshots of both of those pages and save them to Dropbox; that way I’ve got a copy of them in the unlikely situation that there’s some kind of issue with the bonus not being awarded or the wrong number of points are credited to my account. I don’t think I’ve ever had a problem with points not posting correctly, but I have seen occasional data points where people have had issues, so screenshots can greatly assist in providing the evidence you need that a specific welcome offer was in force when you applied.

Keep a record of your cards

Regardless of whether my wife or I are approved for a new card, I track our applications on a spreadsheet. It’s not an elaborate spreadsheet, but it captures the date we applied, which card we applied for, the welcome offer and minimum spend requirement, the annual fee, and a column for any applicable notes.

If we’re approved, the cells remain white. If the application goes pending, I highlight the background of the row in yellow. If an application is declined, as well as when we cancel a card, I highlight the row in red.

That makes it easier to see at a glance which cards we have and, most pertinently for this post, which cards we’re currently working towards a minimum spend.

Set a calendar reminder

The rest of the Frequent Miler team know how much I rely on Google Calendar for organizing my life. I don’t look at my calendar at all during the day other than to add reminders as necessary, but I use it to set calendar reminders to myself—often repeated each day, week, or month depending on what it is—and have those reminders emailed to me.

One of those is a weekly reminder to check if I still need to complete a minimum spend requirement. Most weeks that point is moot because I’m either not working on a new card welcome bonus, I know that I’ve just completed one, or I know I’m well on course for hitting the spend requirement and so I don’t need to sweat it.

That said, it has saved me once or twice. For example, last year I was working on a Chase Ink Business Cash® welcome offer which, at the time, had two spending tiers. I’d noticed that bonus points had posted and so I hadn’t been using the card further. Thankfully that email reminder via Google Calendar prompted me to look at my card tracking spreadsheet again and I realized that we’d spent enough to hit the first spending tier, but not the second. We would’ve missed out on an additional 40,000 Ultimate Rewards points if I’d not paid attention to that, but thankfully I caught it in time.

Now, that’s not to say that you should use the specific technique that I use to remind myself of things, but I would recommend setting some kind of reminder for yourself to ensure you spend enough on your new credit cards in order to earn the welcome bonuses.

Spend extra

When meeting spend requirements, I prefer to spend at least a few hundred bucks extra on the card beyond what’s required within the timeline given by the card issuer. That’s because occasionally I might need to return an item, or I’ll be given a refund for a purchase for one reason or another. If that happens, there’s a danger that your welcome bonus will be clawed back.

It’s potentially less of an issue if the refund occurs within the timeframe given to meet a minimum spend because you’re able to rectify the situation by subsequently spending more. However, if the refund occurs after your 90 days or 3 months (or however long) to hit the spend are up, the bonus could get clawed back and there’s no way to mitigate that by spending more as it’s beyond the end date.

On a somewhat similar note, be careful with online orders because some retailers won’t take payment until an item ships. If there’s a delay in shipping (e.g. you order a customized laptop from Dell that doesn’t ship for a couple of weeks after the date you place the order), your card won’t be charged until it’s about to be sent. If this happens early on in the minimum spend timeline it’s no biggie, but if you’re bumping up against the time limit to meet the spend, it’d be frustrating to discover that your anticipated purchase didn’t post to your account in time.

Plan ahead

Large expenses such as for home improvements, quarterly taxes, tuition fees, etc. can be a great opportunity to complete—or at least make very good progress towards—the minimum spend requirement for a new credit card (or multiple cards).

If you know in advance that you have upcoming expenses like that, it’s worth applying for a new card (or cards) so that you have them in hand before it’s time to pay for the items or services. While some card issuers will provide an instant card number upon approval and others will let you add the card to a digital wallet immediately, if you have the opportunity to get the physical card before large payments are due, that’s the safest option.

Have a backup plan

If your plan for meeting a minimum spend requirement is contingent upon paying for a large expense, it’s worth considering what your backup option(s) will be if that plan falls through.

For example, a contractor who accepts credit card payment for your kitchen renovation might fall ill or pull out of completing the job for some other reason. A payment processor might decline your payment for some reason. You might not be approved with a large enough credit limit to make a large payment in a single transaction and the retailer doesn’t give an option to split the payment with another card. Your company might change their mind about allowing you to pay for business travel with a personal credit card and be reimbursed for it.

Whatever the reason, the best laid plans sometimes fall through, so it would be a shame to forgo the opportunity to earn a welcome bonus due to your day-to-day spending not being sufficient to meet a high spend amount. If you find yourself in that kind of scenario, can you prepay your taxes? Overpay your utilities? Buy gift cards for the store where you always do your grocery shopping? Pay other bills that don’t accept direct credit card payment utilizing Plastiq? We have a post that helps explore your options, so check that out for more ideas: Guide to increasing credit card spend.

An important thing to consider is whether you can cover the cost of those additional payments when prepaying. It’s easy enough to prepay taxes, but if that would mean you wouldn’t be able to pay off the bill in full when it’s due, the interest payments could far outweigh the value you’ll get from the welcome offer bonus points.

Beware ineligible spending

There are occasionally quirks that it’s important to be aware of when meeting a minimum spend requirement with regards to purchases that don’t count. For example, Bilt doesn’t offer rewards when making tax payments which also means that tax spending doesn’t count towards the spend requirement on a new card.

Another important quirk to be aware of relates to cards issued by US Bank. With many of their cards, only spending on the account owner’s (i.e. primary cardholder’s) card counts towards the minimum spend requirement; purchases on an authorized user or employee card will earn rewards as standard, but won’t count towards the minimum spend amount.

Consider spend length in addition to spend amount

Welcome offers with high spend requirements can be off-putting for people with relatively low spending capacity and who don’t want to use other methods for increasing their spend. However, before immediately writing off a card due to how much you’d have to spend, take into account how long you have to meet that spend.

For example, a card that gives you 6 months from approval to meet a $15,000 spend requirement is less on a per-month basis (average of $2,500 per month) than a card requiring $10,000 spend in the first 3 months (average of $3,333). The spend required on the latter card is lower, but the average monthly spend is higher.

That said, you might be able to earn more bonus points overall by earning two or more welcome offers with $15,000 of spend rather than just one bonus.

Don’t spend for the sake of it

When you suddenly have thousands—or possibly tens of thousands—of dollars that you need to spend in order to earn the bonus from a welcome offer, it can be tempting to buy stuff that you wouldn’t otherwise have purchased seeing as it’ll help you towards that spending target.

As a result, it’s worth questioning whether purchases you make are for items you really want/need, or if that high spending target is seducing you into making yourself poorer (in a way) due to making unnecessary purchases.

One key tip is to be aware of timing if you don’t want the bonus until after a certain date. This typically comes up related to the Southwest cards and Companion pass. You don’t want to accidentally hit the minimum spend requirement in December if you are trying to get the Companion Pass in January. Always wait to hit the spend until after January 1 and be careful of accidental charges. With Chase, points typically post on the statement date so you may be safe to spend after your December statement close, but some people hold off on hitting the minimum spend just in case.

This is important to keep in mind with Amex Hilton cards, especially with the current FNCs. With Amex the bonuses are usually awarded immediately and don’t wait for the statement close date. Therefore, if you are planning to use a FNC for travel that is a year away, make sure to wait to hit the minimum spend requirement for the bonus (and FNC) until the date you wish to use the FNC is within 365 days. If you hit the bonus early, you likely won’t be able to extend the expiration of the FNC.

I know missing the deadline is a big risk, but hitting the deadline too soon is a problem for people literally every year. Be careful and know the applicable rules!

Hey Stephen! Here’s a great tip – download the free app Travel Freely and enter your new card every time you open one. You’ll get email reminders when the minimum spending requirement deadline is close. Awesome way to offload the mental load and keep your calendar cleaner. 🙂