When Chase refreshed the Sapphire Reserve® card and launched the Sapphire Reserve for Business℠ card last year, it did away with the previous 1.5 cents per point (cpp) redemptions everywhere via Chase Travel℠ and replaced them with Points Boosts.

This feature gives holders of either card the opportunity to redeem Ultimate Rewards points for increased value for select hotel stays and flights. Over time, Chase has whittled away at the value you can get with Points Boost, and boosted values now seem to have a far lower floor than when they were released, down to as low as 1.15cpp. There’s now a 2.5cpp ceiling as well, but only for a handful of hotels that rotate periodically.

We had assumed that Points Boost rates between the consumer and business versions of the Sapphire Reserve cards were essentially the same. However, reader Hien sent us some screenshots of a search they conducted in Montreal the other day that proved otherwise.

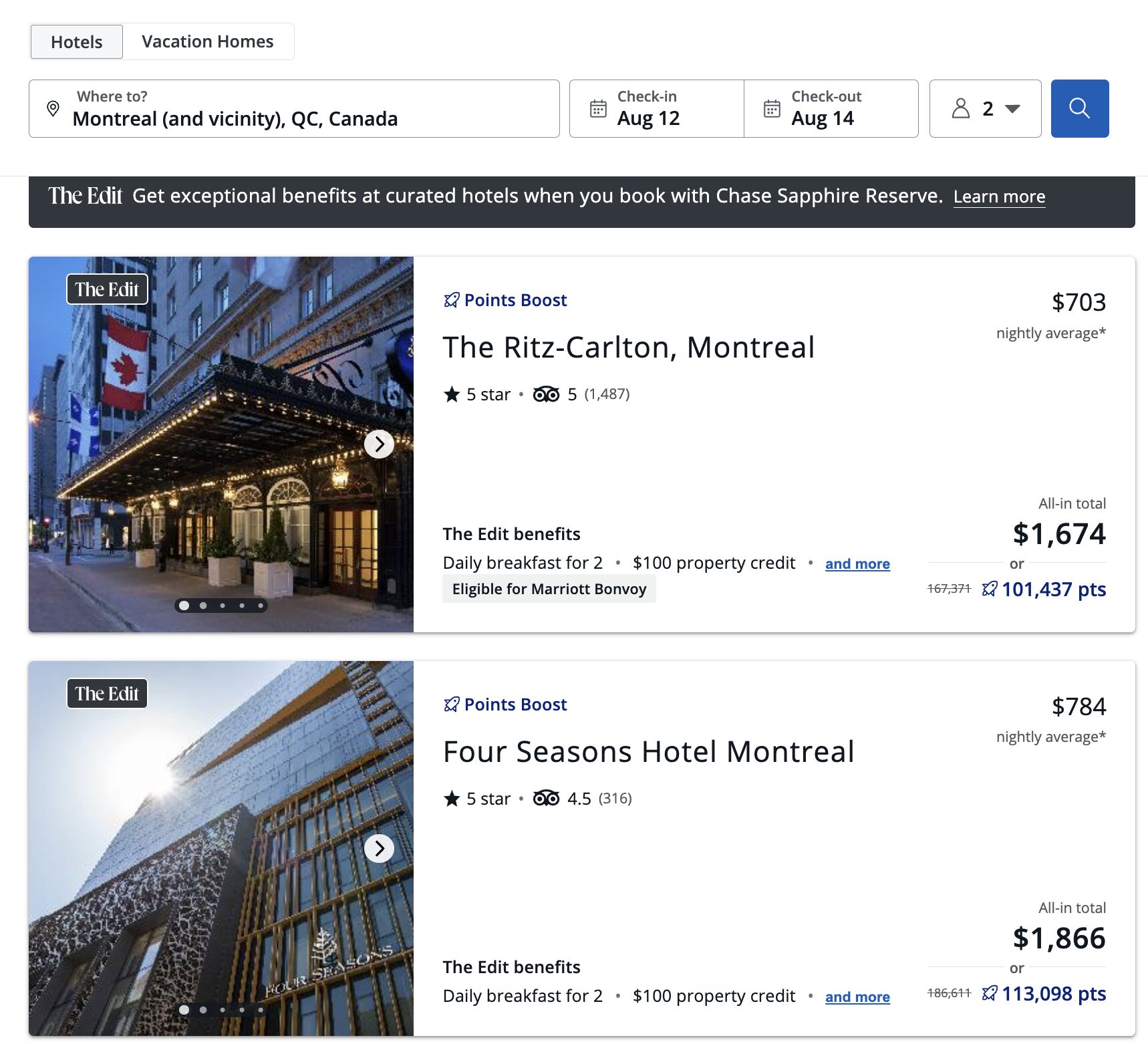

First, they searched for hotels when using their consumer Sapphire Reserve card and found the following results:

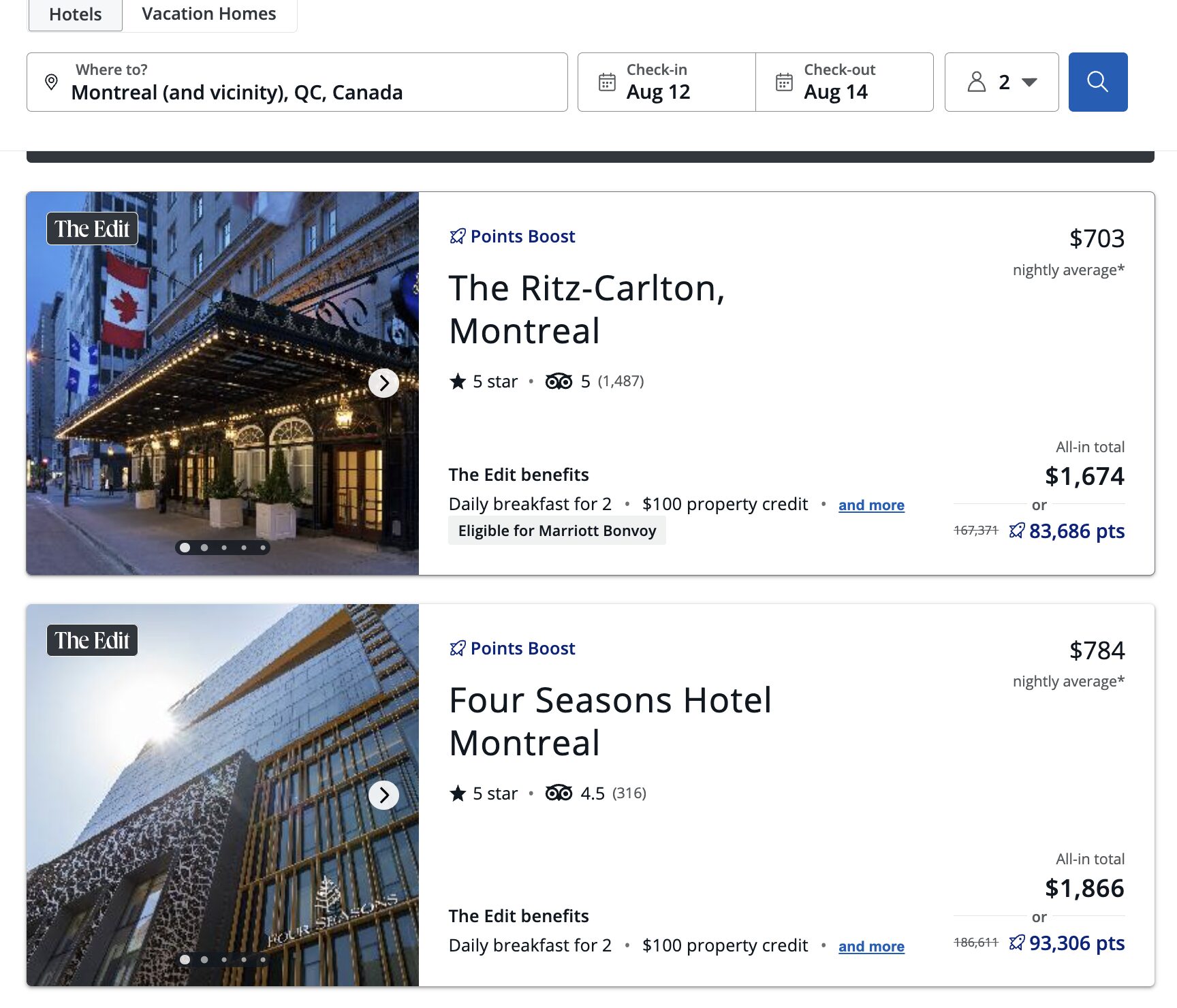

Both properties show a Points Boost redemption value of ~1.65cpp for these two Edit properties, which seems to be the most common rate we see these days. Afterward, they switched over to their Sapphire Reserve for Business and found that the same hotels on the same nights were boosted all the way to ~2 cents per point:

In this case, booking a two-night stay through their business card would save them ~20,000 Ultimate Rewards points when compared with using their consumer card for the same booking.

Greg is the only one on the team who has both a consumer and business Sapphire Reserve card. He looked at a couple of cities and found that in one case the results were identical; in the other, the business card showed higher redemption rates. In addition, he was able to exactly replicate what Hien found on the same dates in Montreal.

Quick Thoughts

Chase’s communication about Points Boosts since the Sapphire Reserve launch/refresh has been bizarre, to say the least, and we’re not certain what equilibrium they’re trying to reach. We initially thought all Edit properties would be at 2cpp, which sounded great…until we discovered that wasn’t the case. Stephen’s analysis showing that many rates had fallen to as low as 1.15cpp had us pining for the good ‘ole days of 1.5cpp everywhere.

We’re not entirely sure what to make of this disparity between the business and consumer cards yet. It might be that these are a couple of isolated, quirky examples… but it could also be a pattern that’s intended, which would be a blow to the consumer Sapphire Reserve and a “boost” to the appeal of Sapphire Reserve for Business.

Greg plans to dig into this with more detail soon. In the meantime, we’d love to hear about any experiences readers have. Has anyone else noticed a difference between Points Boost rates between the two cards? Let us know in the comments!

")

")

I have 2 rooms booked in Vancouver and the biz reserve is showing 1.65 and the reserve 2.0. I ended booking thru the reserve but you can use either card to pay which will trigger the $250 credit.

My JP Morgan Reserve card also has different points boosts from my plain saffire reserve…usually worse.

What would be interesting to learn is whether Chase is doing a type of dynamic pricing with The Edit and Points Boost. That is, whether the cash price for a given property varies from person to person WITH THE SAME CARD. And, whether the Points Boost for a given property varies from person to person WITH THE SAME CARD.

Might Chase be using something called surveillance pricing?

With everything that has been going on with Chase, I wouldn’t be surprised.