NOTICE: This post references card features that have changed, expired, or are not currently available

The PenFed Pathfinder Rewards card has re-launched as a Visa card and it comes with a nice bonus of 50,000 points after $3K spend in the first 90 days (worth ~$425). Opening the card through a referral link will put another $50 in your pocket. This card may certainly be worth opening for a bonus, though it is a snoozer long-term that you won’t want to keep beyond year 1 in most instances.

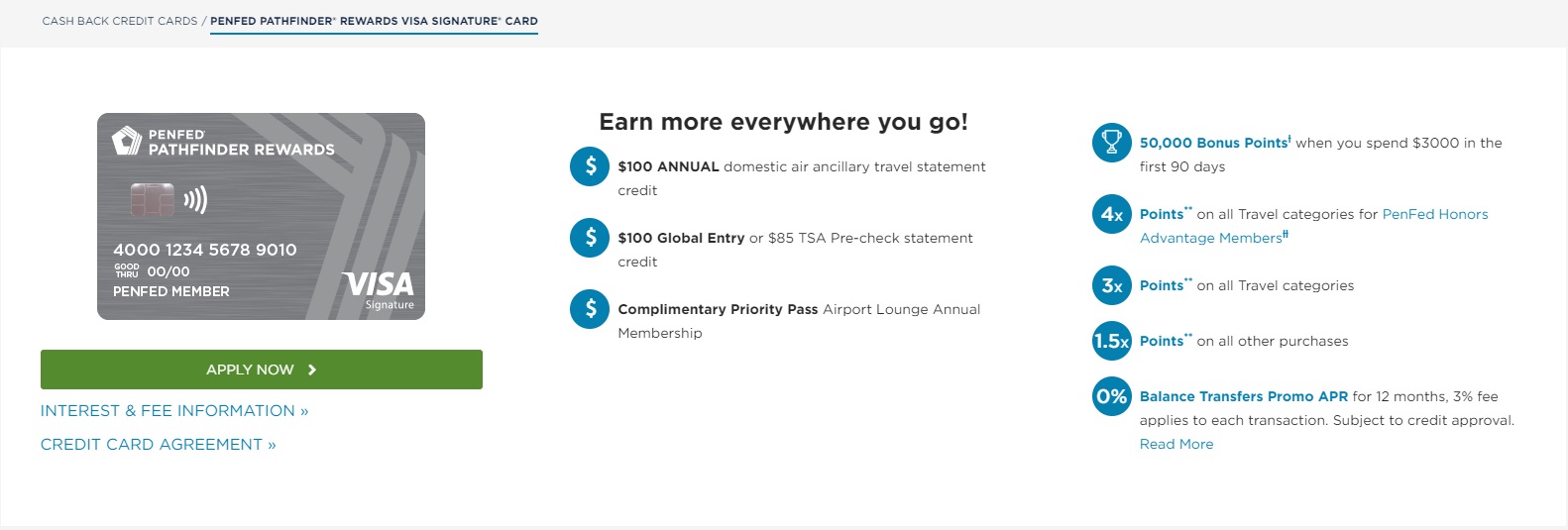

The Offer & Key Card Details

Click the card name below to go to our Frequent Miler card-specific page where you’ll find more information and an application link.

| Card Offer and Details |

|---|

ⓘ $275 1st Yr Value EstimateClick to learn about first year value estimates 50K Points Non-AffiliateThis is NOT an affiliate offer. We always present the best offer even when it means less revenue for Frequent Miler 50K points after $3K spend in the first 90 days$95 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. FM Mini Review: Meh. Points are only worth about 0.85 cents each. I recommended this card when it used to have no annual fee, but not for $95 per year. Earning rate: 4X Travel for PenFed Honors Advantage Members ✦ 3X travel otherwise ✦ 1.5X everywhere else. Advantage membership is available to anyone who opens an Access America Checking account, or to military members. Card Info: Visa Signature issued by PenFed. This card has no foreign currency conversion fees. Noteworthy perks: $100 Domestic Airline Fee Credit ✦ $120 Global Entry credit ✦ Priority Pass Membership ($32 per visit) |

Quick Thoughts

Doctor of Credit lists the following sample point redemptions, which point to a redemption value of approximately 0.85c per point:

- $50 Prepaid Visa card = 5,880 points

- $25 Southwest gift card = 2,940 points

- $100 Delta gift card = 11,760 points

- $10 Amazon gift card = 1,170 points

Assuming you could redeem 50K points at exactly 0.85c per point, that’s $425 in gift cards. Of course, since gift card redemptions are those wacky numbers of points, I imagine using exactly 50K (or however many points you have) will be nearly impossible or require a PhD in calculus, making the points worth a bit less than face value to me (not to mention that gift card redemptions are already questionable to value at face value since there are opportunities to get some of them discounted in the first place).

Still, if you could pull off even $350 or $400 worth of gift cards before hitting your breakage point, the bonus could still be worth a look as that’s a decent return on $3K spend.

Long-term, the card doesn’t offer much value given that it awards 3x on Travel and 1.5x everywhere else for general members (returns of less than 2.83% on travel and 1.275% everywhere else) and it has a $95 annual fee. It may be a bit more interesting for honors members (which must be active duty military or members of Access America based on my understanding), though even then it’s not terribly exciting.

Still, picking up somewhere near $500 for $3K spend is a good enough deal to consider if you’re looking for a new card to flex.

H/T: Doctor of Credit

Hi Nick.

I sincerely disagree and think the card is worth way more long term than the signup bonus. In fact, I’d argue this is one of the best travel credit cards on the market for Penfed members. Why? All the things you skipped over (I get it, you’re busy. $95 annual fee sucks. But the annual fee isn’t really a thing for most people so it’s basically irrelevant. The Penfed people tacked it on at the last minute before launch and it shows when you look at the rewards structure):

#1:

This is a 0-annual fee card for anyone that has an existing or new Penfed checking account. The “access america” checking account only requires a $500 daily balance to waive the monthly fee and pays dividends. If you have a penfed checking or don’t mind opening one and leaving the fee waiver amount in the account, you’re set. And if you are going to apply for a Penfed card, you’re probably a penfed member already, so what’s the big deal?

#2:

The card also earns 4x on travel when you have the above mentioned checking account. So 4*.85=3.4% on travel. That’s pretty competitive. That was designed to be the incentive for having a checking account before the annual fee was added. Now you get both benefits!

#3: They also pay you to keep this card. There’s $100 per calendar year in airline travel credits. They support charges from any domestic carrier. It’s very nice. I’ve used the Amex predecessor credits for years.

#4: There’s a free priority pass membership if you want it (which is pay per swipe at lounge, but the base membership fee is paid for by Penfed. For people without 15 credit cards that don’t travel all that often it’s a pretty nice benefit on this card. Again, this is really designed to be a $0/AF relationship-building card for penfed members. They added the fee to scare away people who won’t be loyal over the long run).

#5: The insurance benefits package that’s on this card is pretty solid when you look at it:

a: There’s trip lost luggage coverage of 3k, which requires only that you pay a portion of the cost of your flight. So book award travel and just pay the taxes on this card and you earn 4x points and are covered. Seems like an easy yes to me.

b: There’s also trip delay coverage. Also requires you to only pay “a portion” of the cost of the trip to your card. That’s pretty nice. Sadly it’s 12 hour clock but still, it’s free.

c. The card actually has car rental insurance. Sure, it should be standard, but that’s becoming less common by the day and many cards now actually lack it (all Citi cards, Discover cards, and many USBank and BoA cards have dropped the benefit). Sure, it’s not “primary” but for the average person it’s more than good enough for how they’re likely to use it.

#6: There’s a $100/85 Global Entry/Precheck credit. Another relationship benefit to banking with Penfed.

#7: They offer a $50/$50 refer a friend program. That’s a nice fringe benefit in and of itself. You can refer anyone to any penfed credit card and get $50 for your trouble. (Self referrals are explicitly banned, sadly. You can see the terms at penfed.extole.io/matt47 and clicking the bottom link for their program. I say it’s a shame because you’d obviously want to self-refer! Penfed has the *best* 2% cash back card on the market hands down – there’s no foreign tx fees, the 2% rewards are available upfront, and the card has a much lower standard interest rate range than the Double Cash. And it also has all the insurance benefits and purchase warranties that its main competitors don’t offer. Between the 2% card and the travel card, you can do very well for yourself just at Penfed)

So, when you go over the value you get off holding this card, the picture starts to look pretty different from what you see at first glance.

If you’re loyal to Penfed and keep a checking account there, you get a 3.4% back on travel credit card with pretty decent insurance benefits. You get a waived annual fee, so the card is free to keep. You get free global entry for yourself and a base priority pass standard membership, which nominally costs $99/year, for free. You get $100/year in airline fees or lounge fees waived from any major US domestic airline. And you get the 50k point sign up bonus to sweeten the deal.

I appreciate your in depth analysis!

Access America is just the name of their checking account. A $500 monthly minimum balance or a $500 direct deposit qualifies you for Honors Advantage benefits, i.e. 4x (3.4% value) for all travel spend, and waiver of the annual fee. There’s also the Priority Pass membership, which might be desirable for some.

And the $100 annual travel fee credit, as others point out.

When did this go to $95 a year? I’ve had this card for several years at no fee. Easy $100 travel credit yearly. They occasionally run deals ($10 statement credit for 3 contactless purchases occurred a month ago or so).

“When did this go to $95 a year?”

A few days ago; hence this new post.

https://frequentmiler.com/penfed-pathfinder-rewards-american-express-card-complete-guide/#comment-2309771

You’re grandfathered in for the no AF.

Mark do you use the card regularly? I have it as well and have never gotten any deals on it. I seldom use so maybe that’s why.

I basically use it to cover $100 worth of airline fees (or $100 worth of $50 Southwest flights booked and cancelled). The deals I get on it are usually stuff like “Get a $10 statement credit if you make three contactless purchases by X date”

Nick,

You are missing one of the best reasons to keep the card, the $100 Airline Travel credit on what was once a no annual fee card. It’s pretty easy to keep this card free (keep $500 in checking or have a $500 direct deposit).