Have you ever had a credit card issuer deny your application for “too many inquiries”? I invariably tell people that the “too many inquiries” reason is completely meaningless (and, to that point, if the results of the complex algorithms used for credit scoring could be summed up so simply, the bureaus would have nothing to sell to the banks). However, a recent report from a well-versed reader indicates that Citi may have a previously unreported rule leading to a denial if you have had any inquiries from other banks in the 5 days leading up to your Citibank application. We’d love to get reader input if you have recent experience with this as described in the post below.

Possible Citi five-day rule

Let’s call our reader “Bob”. “Bob” is someone who I know generally understands the rules of the game and has been a rewards card enthusiast for years. Bob applied for a Chase Ink Preferred card on 10/13/23 and was approved. Chase pulled a credit report from Experian for that application.

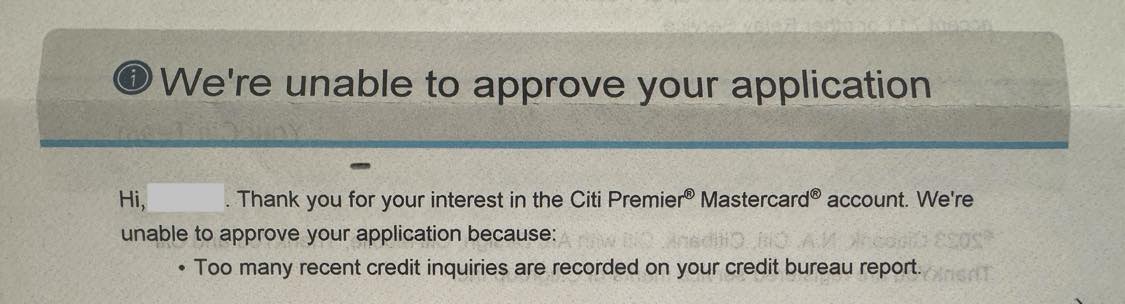

On 10/18/23, Bob applied for a Citi Premier card and after Citi pulled his Experian credit report, his application was denied. The reason given for the rejection was that Bob had “too many recent inquiries”.

Interestingly, Bob’s Experian report only showed two inquiries before Citi’s:

- 11/6/2022 (a Chase application from nearly a year ago)

- 10/13/2023 (The Chase Ink Business Preferred application)

- 10/18/2023 (The Citi Premier application)

Since Bob only had two previous inquiries in two years, the “too many inquiries” reason seemed highly suspect. As noted at the top, I generally advise readers to completely ignore the reasons given in a letter declining an application. We once had a reader report getting denied for a card for “too many inquiries” and she had zero inquiries on her credit report over the previous 24 months. That just proves to me that the reason given on a letter is at least sometimes (if not frequently) entirely fabricated to satisfy the customer’s desire to “know” a reason.

However, maybe there is something more to the “too many inquiries” response that many have gotten from Citi.

On Monday, 10/30/23, Bob called the reconsideration line, which is something you should always consider doing if your application is denied (we keep the reconsideration numbers for each bank on our Best Credit Card Offers page). That’s where things got interesting. The reconsideration representative told Bob that his application was declined because Citi will not approve an application if there has been an inquiry from any other bank within 5 days of applying for a Citi card. The rep went on to say that if he applied again within 60 days, he would get the same result because Citi would use the same credit report for 60 days.

Bob contacted me to ask if I had heard of such a rule before. I hadn’t and I assumed that it was likely not true. Phone representatives often make things up on the fly either when they don’t know the true answer or sometimes when they just think (or assume) they know something. I can not count the number of times that a phone rep has fed me information that I knew was incorrect. I encouraged Bob to call again.

The second time Bob called, the agent reconfirmed the existence of the 5-day rule and said that Bob’s application had been denied because of the fact that there was an inquiry from another bank within 5 days of his Citi card application. After understanding all of the above information, this second representative offered to run Bob’s credit again, confident that this would remedy the situation and lead to an approval since the 10/13 inquiry was now more than 5 days old. Bob agreed, the reconsideration rep pulled his credit again, and his application for the Citi Premier card was approved!

Bob verified that Citi pulled his credit from Experian both on 10/18/23 and again when he called reconsideration on 10/30/23.

I then went to our Frequent Miler Insiders Facebook group to ask for data points from folks who had applied for a Citi card recently. I asked readers who were willing to share to provide the following information:

-

Which Citi card you applied for

-

Date you applied

-

Considering *only the credit bureau Citi pulled*, date of your most recent past inquiry *on that bureau’s report* prior to applying for the Citi card. I don’t need an entire history of all of your pulls, and I don’t need to know the source of the previous pull, just the date of the last one before applying for a Citi card.

-

Were you approved or denied?

We had reports of approval within as short a window as 2 weeks since most recent inquiry, but only one report from a reader who had applied within 5 days of an inquiry from another bank. That reader reported being denied:

1)AA Executive2)Date applied: 10/173)Last inquiry 10/12 Experian4) Hardest denial ever witnessed

I always hesitate to take one or two data points as a firm rule, but backing up to the reader who first reached out about this, the dots seem to connect since Bob’s credit was pulled on both 10/18/23 and 10/30/23 and the only thing that changed was being more than 5 days since the previous inquiry, which was enough to turn the denial into an approval. The case is further bolstered by two representatives citing the same rule and the second one even offering to pull his credit again, clearly confident enough that the end result would be different the second time (one would think that if that second rep reviewed the application and thought that Bob looked like a good candidate for approval, which was obviously the case, she would have pushed through the approval manually……the need for a second pull seems to indicate that the system won’t allow it with an inquiry within 5 days). It certainly seems plausible that in Citi’s case, the key word in “too many recent inquiries” is recent.

All that said, we don’t yet have enough data to be sure that a 5-day rule exists (and not all denials for “too many recent inquiries” will be related to the 5-day rule). I would love to hear from readers with recent experience. Have you recently applied for a Citi card? In the comments, please share:

- Date you applied for a Citi card.

- Consumer or business (I’m just wondering if this makes a difference)

- Date of your most recent inquiry before the Citi application on the same credit report that Citi pulled

- Was your Citi application approved or declined?

I am particularly interested in any data points of approval despite an inquiry from another bank on the same credit report within five days since that would prove that this is not a firm rule.

The possible existence of the 5-day rule may explain why some people have been declined despite having excellent credit. I wouldn’t be surprised if many people have tossed the Citi Premier application at the end of a series of applications for elevated Chase or Amex card offers and gotten declined since they had inquiries from other banks within the previous 5 days. At the very least, until we prove otherwise, it may be best practice to make sure to wait at least 5 days after applying for a card with any bank before applying for a Citi card.

")

")

Here’s my data point that seems to support this theory.

5/12 –

applied for a consumer card with one inquiry from another bank on the same day (thought I’d try the old app-o-rama). there were no other hard inquiries at this credit bureau.

Result: Declined.

Letter in the mail says: “Declined due to too many recent inquiries.”

5/18-5/20 –

Called the recon line 3 times on separate days just to see what they knew.

None of the 3 reps knew about a 5-day rule; they all advised that I apply in 30-60 days, lest I get declined again.

I figured I’d bite the bullet with the third rep and authorize them to rerun the app with another inquiry.

Rep originally said this wasn’t even possible and the only way was to put in another application.

But just as I hung up, they called me back to tell me it worked and I was approved!

Thanks so much for the info, hope this helps.

[…] I have been around the block hobby for a long time and this was news to me: Possible Citi 5-day rule causing denials for “too many inquiries”. […]

[…] Frequentmiler has some studies indicating a doable new rule which auto-declines functions if there was a tough pull carried out in your credit score report from any financial institution previously 5 days. This additionally might trigger a decline for one more 60 days afterward since Citi will simply use the previous credit score pull for as much as 60 days. (After 5 days you’ll be able to name reconsideration and ask them to run your credit score report once more for approval.) […]

[…] Frequentmiler has some reports indicating a possible new rule which auto-declines applications if there was a hard pull done on your credit report from any bank in the past 5 days. This also may cause a decline for another 60 days afterward since Citi will just use the old credit pull for up to 60 days. (After 5 days you can call reconsideration and ask them to run your credit report again for approval.) […]

This post just reopened the wounds from all of the Citi rejections I’ve collected over the last couple years, none of which appear to be due to this possible inquiries-within-5-days rule.

I’ve been denied for the Premier twice (applied 1.10.22, most recent inquiry 11.20.21; and 12.15.22 / 6.1.22) and the Citibusiness AA card several times (which pulled a different credit bureau, never with an inquiry within several months of the application).

I was approved for the Citi AA Executive card on 5.2.22, most recent inquiry before that being the denied Premier on 1.10.22.

I’m not sure what I have done to make Citi hate me, lol. (I have had no trouble getting approvals from Chase/Amex/Barclays over that same period, both business and personal).

One day, Citibusiness AA. One day.

Would it also be useful to gather data on which reports were pulled for each particular card application? For example, if Experian was pulled by Chase on Oct 1, and Equifax by Citi on Oct 4.

No. If Citi pulled Equifax, they won’t see that Chase inquiry on Experian. That’s why I specifically only asked for most recent inquiry on the same report that Citi pulled.

1. 04/26/23

2. Consumer (CCC)

3. 04/21/23 (Chase Ink application)

4. Denied due to too many recent inquiries.

Nick,

I applied for the Citibank Premier card in early August and was denied, and one of the reasons was too many inquiries and that my mortgage had too high of a balance relative to the original loan amount. My last inquiry before August was in April 2023. I couldn’t get a rep to explain to me what my mortgage had to do with it, but when I pushed them saying my credit score was almost as high as it can go 2 different reps mentioned that they have their own formula/score that they use besides a credit score. I’m going to try again in a couple of weeks because I really want the card but if they deny me again, I am through with Citibank along with Capital One who apparently doesn’t like me either.

Buddy, per this piece, was your most recent reporting inquiry on the date of your Citi Premier denial within five days prior?

This happened to me last year, although the reconsideration rep told me it was because another pull the same day triggered their fraud prevention algorithm.

Applied for mortgage pre-approval on 10/16. Applied for Freedom Flex 10/18. Received a “We’ll review your Chase Freedom FlexSM credit card application and be in touch soon.” Caught me by complete surprise, b/c have sky-high credit, very good rapport with Chase, credit history for 49+ years (yes, that is since the early 1970’s. Some parents were smart enough then, too) and have never not been immediately approved for a cc. I guess that 5-day rule goes beyond Citi.

No, Chase definitely doesn’t have a 5-day rule. My wife and I have both been approved for plenty of Chase cards within 5 days of an inquiry from another bank (including recently). There are lots of other reasons someone might be turned down. What was notable here was not only that two reps cited the same rule but that the second rep offered to pull the credit again from the same bureau (presumably) knowing that would work.

Did you call reconsideration? Sometimes it is as simple as calling to verify that you submitted the application, sometimes it was a typo, or you may have just hit the max exposure in terms of how much credit they are willing to extend but you may be able to move credit line from another card. I’d definitely call Chase.

I second that. Got Amex then chase cards within 5 days of each other. Approved for both.

I applied for the Citi Premier CC and was declined for the same reason as above. This was the fourth card I applied for in my recent app-o-rama after being approved for an AMEX, Chase, and Barclays. I called recon before receiving the denial letter and the rep seemed very hesitant to discuss the reason for the denial without me first receive the letter. I don’t think calling Citi to pull another credit report will work for me due to my new credit inquiries and new accounts on my credit report.

app-o-rama is dead in some cases.

I was under the impression that banks are required by law to give you a reason for denying you credit. Therefore it’s not (only) to satisfy the curiosity of the applicant that they provide this information.

I can imagine that, while banks are probably frequent tweaking their approval algorithms, that getting a brand-new reason added to the list is probably very time consuming, involving both Legal (“no, you can’t say that”) and Risk Management (“no, that gives away too much information about our internals”). In that case, where an algorithm change is desired without all the trouble, the software team is incentivized to simply pick “something close” off the existing list of reasons for denial.

Great reporting here Nick. I especially appreciate your gathering data before publishing this post, as well as using it to request yet more corroborating data!

FWIW, I actually think Cit’s policy makes some sense here. An easy way for a bank to screen for bust-out risk, as well as extreme gamers (who tend not to be valuable customers), is to deny folks credit who have been shoping for other credit cards within the past week.

Suggestion: refine your question #3 to ask for date of most recent inquiry, specifying whether for a credit card or other. It wouldn’t surprise me if the rule doesn’t prohibit approvals when the inquiry is for mortgage shopping, or for a student lender, for example.

Then again, their algorithm may not be able to distinguish types of inquries..in which case, Citi applicants should be sure they have no inquiries of any kind before firing off an application.

Again, thanks for reporting on this! It will save many of us mistimed applications going forward.

I genuinely thought this was a well-known rule throughout the community. I had a friend who was denied a citi card for the same reason and same situation, over a year ago. They tried to tell me that the rule applied only to Citi cards – as that’s what “almost all of the bloggers” say on their websites regarding the 8 in the 8/65 rule. In my opinion this is an example of unfortunate circular reporting, without folks using their own personal experience – or experience of those close to them. Hopefully awareness of this rule can grow so people don’t potentially waste time applying for an auto-denial.

Interesting Jeff.

FWIW I’ve been applying strategically for 25 years, have had > 100 cards, and am a member of several groups, public and private, who follow these issues. Despite that, this was brand new information to me.

DoC has written about the 8/65 rule before

I’m familiar. But where did their discussion ever address this issue? Not in their main post, at https://www.doctorofcredit.com/citis-application-rule-explained-865-rule/# …

(They just last night amended that post to include reference to this piece)