Bilt, the neighborhood rewards program that offers the opportunity to earn points on rent, mortgage, and with a plethora of neighborhood merchants, has officially announced their new “Bilt Card 2.0” credit card lineup today. Those who followed leaked details last week won’t find many surprises here, as the new cards are more or less what they were rumored to be.

Three new Bilt cards: Bilt Blue, Bilt Obsidian, Bilt Palladium

Bilt, in conjunction with Cardless, has officially announced the launch of three new credit cards today. All three cards will be available for use beginning on February 7, 2026, but existing cardholders can choose their new card today (if they wish to keep a Bilt card), or it will be possible to “pre-order” by applying for one of the new cards now in order to have it at launch.

Details of each card are as follows:

Bilt Blue card

| Card Offer and Details |

|---|

ⓘ $25 1st Yr Value Estimate$100 Bilt Cash valued at $25 Click to learn about first year value estimates $100 Bilt Cash $100 Bilt Cash when you apply & are approvedNo Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Earning rate: 1X points + 4% Bilt Cash on everyday purchases if you choose Bilt Cash rather than housing-only rewards ✦ 0.5X-1.25X points on rent & mortgage payments (if Housing-Only Earnings selected) ✦ 1X points on rent & mortgage payments when redeeming Bilt Cash (if Bilt Cash earning option selected) Base: 1X (1.55%) Card Info: Mastercard World Elite issued by Column NA. This card has no foreign currency conversion fees. Noteworthy perks: Transfer points to airline and hotel partners ✦ Earn points on rent or mortgage payments |

- Annual fee – $0

- Bilt points earning rate – 1x on everyday spend (including unlimited 1x on mortgage and rent, subject to a 3% fee that can be offset with Bilt Cash)

- Bilt Cash earning rate – 4% on everyday spend (excludes mortgage & rent)

- Card features/benefits:

- No foreign transaction fees

- Access to the Neighborhood Benefits program

- Redeem Bilt Cash to waive mortgage and rent transaction fees

Bilt Obsidian Card

| Card Offer and Details |

|---|

ⓘ $-20 1st Yr Value Estimate$200 Bilt Cash valued at $50, $100 Bilt Travel hotel credit ($50 per six months) valued at $25 Click to learn about first year value estimates $200 Bilt Cash $200 Bilt Cash when you apply & are approved$95 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Earning rate: 4% Bilt Cash on everyday purchases if you choose Bilt Cash rather than housing-only rewards + 3X points on dining or grocery (Limit $25K per year for grocery) ✦ 2X points on travel ✦ 1X points on everyday purchases ✦ 0.5X-1.25X points on rent & mortgage payments (if Housing-Only Earnings selected) ✦ 1X points on rent & mortgage payments when redeeming Bilt Cash (if Bilt Cash earning option selected) Base: 1X (1.55%) Travel: 2X (3.1%) Flights: 2X (3.1%) Hotels: 2X (3.1%) Grocery: 3X (4.65%) Dine: 3X (4.65%) Card Info: Mastercard World Elite issued by Column NA. This card has no foreign currency conversion fees. Noteworthy perks: Transfer points to airline and hotel partners ✦ Up to $100 in Bilt Travel hotel credits ($50 per six months, two-night stay required) ✦ Earn points on rent or mortgage payments |

- Annual fee – $95

- Bilt points earning rate:

- 3x on dining or grocery (you can choose within 30 days of approval and then change once per year in January). 3x grocery earning is capped at $25K spend per year

- 2x on travel

- 1x on everyday spend (including unlimited 1x on mortgage and rent, though be aware that you will need to use Bilt Cash to offset the credit card transaction fee to earn points on rent/mortgage)

- Bilt Cash earning rate – 4% on everyday spend (excludes mortgage & rent)

- Card features/benefits:

- $100 Bilt Travel Hotel credit (twice annual i.e. $50 Jan-Jun & $50 Jul-Dec). Two night minimum stay required.

- Cellphone protection

- Redeem Bilt Cash to waive mortgage and rent transaction fees

Bilt Palladium Card

| Card Offer and Details |

|---|

ⓘ $505 1st Yr Value Estimate$300 Bilt Cash valued at $75, $200 Bilt Cash valued at $50, $400 Bilt Travel hotel credit ($200 per six months) valued at $100 Click to learn about first year value estimates 50K points + $300 Bilt Cash 50K Bilt points + Gold elite status after $4K non-housing spend in the first 3 months, plus $300 Bilt Cash when you apply & are approved$495 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Earning rate: 2X points + 4% Bilt Cash on everyday purchases if you choose Bilt Cash rather than housing-only rewards ✦ 0.5X-1.25X points on rent & mortgage payments (if Housing-Only Earnings selected) ✦ 1X points on rent & mortgage payments when redeeming Bilt Cash (if Bilt Cash earning option selected) Base: 2X (3.1%) Card Info: Mastercard World Legend issued by Column NA. This card has no foreign currency conversion fees. Noteworthy perks: Transfer points to airline and hotel partners ✦ $200 Bilt Cash annually ✦ Up to $400 in Bilt Travel hotel credits ($200 per six months, two-night stay required) ✦ Earn points on rent or mortgage payments ✦ Priority Pass (excludes restaurants) |

- Annual fee – $495

- Bilt points earning rate:

- 2x on everyday spend

- Unlimited 1x on mortgage and rent, though be aware that you will need to use Bilt Cash to offset the credit card transaction fee to earn points on rent/mortgage).

- Bilt Cash earning rate – 4% on everyday spend (excludes mortgage & rent)

- Card features/benefits:

- $400 Bilt Travel Hotel credit (twice annual i.e. $200 Jan-Jun & $200 Jul-Dec). Two night minimum stay required.

- $200 Bilt Cash annually

- Priority Pass

- Redeem Bilt Cash to waive mortgage and rent transaction fees

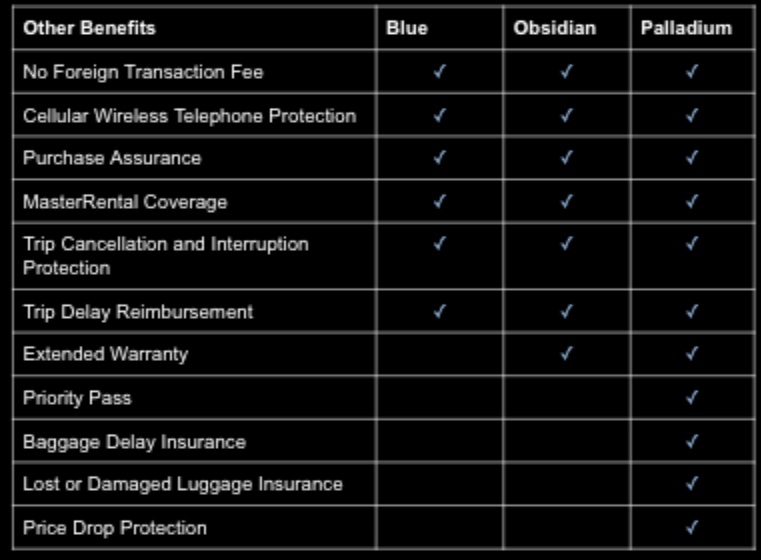

Mastercard benefits

It is worth mentioning that all three cards will carry some Mastercard-related benefits as the Blue and Obsidian cards will be World Elite Mastercards and the Palladium card will be a World Legend Mastercard. This chart shows benefits at a high level, though we don’t yet have full details regarding coverage limits:

Quick Thoughts

We’ll have far more analysis to come, but the short story here is that those who primarily used Bilt to earn points on rent with no fee and just a few small transactions per month will be unhappy (as will those who care about 5/24 and now may be on their 3rd “new account” from Bilt and be facing a new Wells Fargo account as well if they keep that line open). That stinks.

On the other hand, depending on the applications and limitations of Bilt Cash, the new cards could be compelling to a new segment of customers. On the surface, they will unlock the ability to earn unlimited points on rent and mortgage (you can even pay rent/mortgage on multiple homes or for family and friends).

To be clear, it will still be possible to pay rent (and now mortgage) without a fee (including any mortgage lender.

Earning rewards on rent or mortgage is a bit more complicated:

- You can unlock up to 1x on rent by using Bilt Cash at a value of $30 in Bilt Cash for each 1,000 points (you can use more or less Bilt Cash depending on the total cost of your rent or mortgage

- If you don’t have enough Bilt Cash to unlock all of the available points from your rent or mortgage payment, you can choose to pay a 3% fee on the amount not covered by Bilt Cash or choose not to earn points on the full payment. For instance, if your rent costs $3,000 and you have $60 in Bilt Cash, you can use that $60 to unlock 2,000 points on that rent payment. You can then choose to pay $30 if you want to earn a full 1x (3,000 total points).

While Bilt marketing materials reference using $30 of Bilt Cash to earn 1,000 points on rent or mortgage, we are told that there are no minimums and that cardholders can apply any amount of Bilt Cash that they wish. For instance, if you spend $1,000 on your Bilt Card, you’ll earn $40 worth of Bilt Cash. You could then pay your mortgage or rent with your Bilt Card and use that $40 in Bilt Cash to earn up to 1,333 points on your rent/mortgage payment (if the total payment is higher, you can either pay the difference without a fee and no additional rewards or you can pay the fee in order to earn rewards). I wouldn’t buy Bilt points at a 3% fee, but the option is there.

Note that you cannot offset the credit card transaction fee for non-Bilt cards. In other words, if you pay your rent with your Alaska Airlines Visa Signature card (which currently incurs a 3% fee), you will not be able to offset the fee with Bilt Cash. You can only use Bilt Cash to earn rewards when using your Bilt card to pay rent/mortgage.

We will have a full FAQ post out shortly with the answers to additional questions.

Ultimately, the value proposition relies on your valuation of Bilt Cash, and that valuation of Bilt Cash depends heavily on the rules and redemption options. What we know so far is that Bilt Cash will expire at the end of the year (even Bilt Cash earned as late as November and December), with the ability to roll over up to $100 in Bilt Cash. We are told that Bilt Cash can be used dollar-for-dollar toward things like Lyft rides, home delivery, hotel bookings, and “more to come” (including the ability to unlock status for a day to take advantage of a Rent Day transfer bonus). However, the mechanics and limitations are mostly unknown. If it turns out to be easy to use Bilt Cash, that will obviously strengthen the value proposition of the new cards. If not, some may still find the new cards useful if they have enough otherwise unbonused spend each month, but the utility of Bilt Cash is a big factor.

Bilt Cash redemptions for BLADE will be a fixed $350 amount, even if flight cost is cheaper")

Assuming your rent/mortgage is high enough, then isn’t the $495 card a 3.33x point per dollar card? Which seems pretty decent.

And does that make the $95 card:

– 4.33x on Dining or Groceries

– 3.33x on travel

– 2.33x on everything else

Help! How much non-mortgage spend would I need to make on the Basic Blue card if my monthly rent is $4,000?

Thank you!

Reddit has links to calculators.

Isn’t this not true anymore “will need to use Bilt Cash to offset the credit card transaction fee” didn’t the do away with that?

Apologies if this has been posted below, but I do believe the 2026 Bonvoyed Award has already been locked up–not for the card refresh itself, necessarily, but for the heinous rollout. From the lack of concrete information about Bilt Cash and the future benefits, to the seemingly stratospheric number of current cardholders who either had their credit limits slashed to irrelevantly small numbers or were rejected entirely, all paired with Bilt’s (i.e., Kerr’s) utter contempt for the disappointment of Bilt’s many regular users. An utter masterclass on how to alienate customers.

I’m not sure what Phil is talking about. It took me 2 minutes to apply and be approved for the Palladium card. My CL went up from 10k (old card) to 12k (new card). The account number stays the same and my rent payment continues to be drafted automatically.

Exactly this. The used car (I mean, credit card) salesmen like TPG, FM, and the like were all pimps in this whole process and honestly, still are trying to “sell” the cards while playing both sides. It’s amazing how quickly they sold out to Blit and continually have done for the last couple years. Makes me wonder why anyone would click thru from any affiliate links for anything ever again, unless you were just a mindless idiot who couldn’t see what was really going on.

I’m not a fan of the 2-night minimum hotel stay to use the hotel credit. Was considering the Palladium card because I value Alaska and Hyatt points, and the ability to earn 2x on my “everything else” spend. I also have a large mortgage payment and would like to earn points on it, and could offset the fees with my other spend, but… the value of this card (for me) was contingent on being able to offset tye annual fee by using the hotel credits. I have a lot of one-night stays. $200 off of a 2 or more night stay doesn’t feel like a big enough discount when I could otherwise book the hotel on points.

What’s the best exit strategy for someone who’s been only using the card for 5 one-dollar purchases and their rent payment in the past? No annual fee version or cancel the card?

The transition will likely be a +1 to your 5/24. So probably best to close it unless you are going to commit to Bilt. Your points don’t go away or expire just by canceling the card.

Restaurants!

“2. Earn points and 4% back in Bilt Cash

Bilt has the only cards that earn both points and 4% back in Bilt Cash on everyday spend.

Bilt Cash is a new rewards currency which gives you even richer rewards inside Bilt’s ecosystem. You can spend it on monthly credits on restaurants, hotels, rideshare and more – or use it to unlock access to housing rewards, transfer bonuses, and more.”

I think focusing on the value of Bilt Cash doesn’t make sense for most mortgage holders. The Bilt Cash is like points on “Whose Line” (don’t mean anything). I see the value prop/math as quite similar to Mesa actually.

For example, I was thinking of the middle tier card. My mortgage is $1865, but when you account for the $200 Bilt cash on signup, monthly spend of ~$1k offsets the fees on mortgage. Then you spend exactly $1k in the highest bonused category (say, grocery) for 3×1000 + 1×1865 in mortgage spend=4,865 points per month from $1000 in spend you’ve taken away from another card.

Compared against 4x on groceries from my AmEx Gold, it’s actually a slightly better return for $1k spend. However, your return diminishes on every subsequent dollar spent beyond the minimum necessary to earn the Bilt Cash to offset mortgage fees. The question then is: Is it worth the hassle of tracking monthly spend to switch back to the gold after spending $1k?

If you account for the AF of $95, consider the net 865point/mo in my case (compared to AmEx) x 12 mo, and value the points at 1.5c per point, you’re actually only getting $60 in net value compared to just using the AmEx gold. On the other hand, I’m not in bed with the Chase UR ecosystem, so Bilt is my best opportunity to get Hyatt points. So is getting the card and tracking the spend worth it for about 60k Hyatt points per year compared to about 50k AmEx MRP?

Overall good analysis! But isn’t the Amex Gold annual fee $395? Why isn’t that part of the equation.

When I factor in the Amex coupons and 4x on dining (plus the gold is how I access the Amex membership rewards which has some intangible value too), that covers the membership fee. So then in my specific circumstances I’m really comparing the Amex 4x grocery multiplier vs the Bilt 3x grocery+mortgage points.

You would only earn 1,333 points from your mortgage with $1k spend. You need to spend $1,398.75 each month to earn enough Bilt Cash to offset the full mortgage payment fee. If you update your math, based on $1k spend, you lose $35/year by having the Bilt Card.

Confused if I missed something. My mortgage is 1865, so points earned would be 1865. The $1k per month spend needed to cover mortgage fee is based on the fact that the mid-tier card gives you $200 per year in Bilt Cash to start. So for year 1, 3% of $1865 x 12 months is $671.44. Minus the $200, I actually only need to earn $471 in Bilt cash to cover the fee to get mortgage points. At 4% earning rate that’s $1178ish for the year or almost $1000 spend needed per month. No?

Oh, I missed this part in your first comment: “…but when you account for the $200 Bilt cash on signup.” I was referring to ongoing value. I take it back. You’re all good.

My numbers will work for describing someone who keeps the card after the first year.

Though you do allude to “60k Hyatt points per year” in your last sentence.

I suppose if you considered the ongoing value of the card, which is what I was writing about, you might end up canceling/downgrading the card after a year? In that case, you’d have the net benefit of ~$60 that you calculated, which is pretty weak for a sub, even if it like the idea of earning Hyatt points instead of Amex MR.

Makes sense! I thought that might be where your math differed from mine. It’s funny because I was leaning away from applying given how weak the math-based argument is for the Bilt card…and then listened to the podcast episode where Nick said, effectively, “I’d pay the $95 fee just for the opportunity to earn 3x Hyatt or Alaska points on groceries, to say nothing of potential rent day transfer bonuses.” Which has me rethinking the whole thing. Effectively, how much more valuable is the *opportunity* to earn points with occasionally very outsized value. I haven’t checked the RRV on Bilt vs Amex lately, but I assume they’re fairly close, though there’s definitely a more intangible value to Bilt ecosystem that’s hard to quantify.

One downside to Bilt that you’ve already touched on, but is worth mentioning again, is that you’re effectively committing $12k/year of spend (potentially much of it grocery) in the first year and roughly $16.8k/year if you keep it beyond that.

If you cancel after the first year due to the ongoing spend requirement (without that $200 Bilt cash), then it’s no better than a 58,380-point signup bonus after spending $12k in 12 months. From that perspective, it probably doesn’t look very attractive.

For your interest in Hyatt/Bilt, I’d suggest thinking about dipping your toes into Chase ecosystem for Hyatt, or directly signing up for an Alaska/Hawaiian card and starting there. I know it’s not a single currency that can convert to either, but you’d also get to continue earning plenty of 4x on your Amex Gold because their spending requirements are a lot lower, and you wouldn’t be diverting so much spend.

So far you’ve been comparing the opportunity cost of spend on Bilt vs. the Amex Gold you already have, but you might want to think about the opportunity cost of the new credit cards you might not be signing up for if you’ve already committed 12k/16.8k of spend to Bilt.

You’re cherry picking benefits in this comparison. You’re highlighting Amex gold’s 4x multiplier but not acknowledging that Bilt can earn off a mortgage payment that Amex gold is leaving on the table since it can’t earn off it.

Well that was the whole point of sharing my math. In my particular circumstances, the additional mortgage points vs the higher grocery multiplier are almost a wash (particularly when you account for the annual fee of another new card). For a more extreme example, someone who pays $1000 or less in mortgage actually earns fewer points from the Bilt card if they have to move spend from a 4x earning card in order to earn enough Bilt cash to get the mortgage points. Of course, higher mortgage makes the Bilt card increasingly appealing

Will we get 2 new accounts for 5/24 if we get a new Bilt card? For example, 1 for the Autograph and 1 for the Bilt card.

Yes, I would assume you would.

Wait, is this right? I assumed that the move to the Autograph would just be a product change since it’s still with WF and not count toward 5/24.

I would think that too. It would be like getting a new card number due to fraud – that isn’t a 5/24 event.

WF says the Autograph card will have a new account number and will switch from MasterCard to Visa; so Nick’s assumption would seem likely correct to me.

Ouch.

If you accept both. A lot of people will likely drop WF as they are not showing the initiative to market the ‘Journey’ at ex-BIlt customers.

Yikes, according to their reddit AMA, Bilt Cash will have limits when used for non-housing payments. That makes the value proposition vs the VX much worse.

Yup. Palladium for a one year churn and burn seems like an option, or just giving up.

Depends on wheher the constraint is binding.

The Palladium Card is compelling for mortgage holders and higher spenders. I personally have a modest mortgage of $1,400 per month, so my non-rent spend would only need to be $1,000 to earn the BILT cash to offset. Using it as a catch-all is intriguing as our family spends well over $25k of 2x miscellaneous spend in a year, which would keep the Gold status after it expires with the card. That will allow us to keep the 1:1 ratio with Rakuten and hopefully get better transfer bonuses. Since I’m way over 5/24, this will allow us to capture some of those Hyatt points and having ATMOS options are not bad either. I think as long as we’re able to use the hotel credit, I think it’s a win and may just well replace my Venture X card…

Correct me if I am wrong, but let’s say a valuation of 2 cents per point. Lets say you get the palladium and do a $3,000 transaction and you come up with $120 of fee free credit via bilt cash for rent/mortgate. Then you can take that amount and pay a 5k monthly mortgage…netting an extra 5k points. Let say you transfer to Hyatt…it may accrue at 2 cpp $100…why would I take the $100 equivalent in points compared to just using the bilt cash for uber or lyft or some other benefits that I am guaranted cash. I understand when hyatt is 5cpp for park hyatt or you get a great first class or business class redeption, but getting the minimum 2cpp may be harder to justify. Let me know if I am wrong in that a redeption would have to be higher 2.4cpp for it to be worth it to pay rent/mortage with card.

It doesn’t sound like “using the bilt cash for uber or lyft or some other benefits that I am guaranteed cash” is going to be as easy as that. It sounds like there will be limits. I definitely don’t think you should think of Bilt Cash as cash money cash. Time will tell how useful it is, but if you’re able to make that $3K transaction and pay a $4K mortgage (at $30 per 1K points, that’s where you’d max out), you’d end up with 6K points from the spend (assuming Palladium as per your example) + 4K from the mortgage for a total of 10K points. If you wouldn’t have otherwise earned points on the mortgage, that’s not a bad deal. If you could have otherwise earned more points on the $3K spend, then account for that. Don’t think of the Bilt Cash as cash cash.

True I was typing quite fast on mobile and noticed some errors in my original message, but yes there will probably be certain restrictions for bilt cash. It does seem like the mortgage does generate a 3.33 point return (2 being from card and 4/3=1.33 pt being from the bilt cash to be used for the mortgage point accrual method. at 2 cpp, effectively 4% and 2.67% via mortgage (granted 4% this fake cash cash of bilt cash was used to yield this 2.67%). I think if it was not for the lucrativeness of hyatt, I would have passed on bilt. The Chase Freedom unlimited does come close to the 2pts per dollar, but I think the difference also lies with unique partners bilt has. Japan airlines is a unique one that Chase does not have (RIP korean air with chase). There will always be pros and cons and being in the credit card and point space for a few years now, I have to say that I am still fortunate Bilt is not a huge coupon book card as compared to amex. I have been with bilt for years and they have reached higher and higher valuations and growth through funding rounds and partnerships. I think there new card structure is more sustainable (RIP Mesa). I guess time will tell how the new bilt cards will play out. Random question, but how did you guys post this article quickly like was it prewritten with reddit information and waiting a final verification. Also random not sure if you know me, but I saw your article on the Jetblue 25 for 25 and how you proposed a family flight. I am actually the first person to finish the challenge. Not sure if you will go to the January event (maybe I will go, but I have some things that may get in the way). If you do, I hope to see you.

@Gurnaj Johal: 1.3c/$. 1x on the mortgage itself and 1.3x (Blue Card) on the covering spend. The base is 2x mortgage amount, not 1x mortgage amount. The amount has to be spent, and covered. That is the point of the new point-earning scheme.

@Gurnaj Johal: 1x on the mortgage itself and 1.3x (Blue Card) on the covering spend. The base is 2x mortgage amount, not 1x mortgage amount. The amount has to be spent, and covered. That is the point of the new point-earning scheme.

Paying a mortgage with Bilt is effectively making Bilt a 2.33x card.

On (say) a $4K mortgage payment I will be short 120 Bilt cash, so I will have to spend $3K (at 4%) just to zero that out. For my trouble I will earn 4K (1x on the mortgage) +3K Bilt points on the spend, so 7K for a 3K spend that would otherwise be used to earn 6K MR (assuming $0 AF Blue Business Plus at 2x MR). Each incremental $ will earn 100 Bilt points and $0.04 Bilt cash.

So if you spend exactly 75% of your mortgage each month you will be at 2.33x. Beyond that you are trading off 1x in points for 4% in Bilt Cash – whether it’s worthwhile depends on how much the cash is worth.

This neglects category bonuses but there are plenty of other cards that have similar bonuses for the same categories.

Mildly interesting, but I would only consider using up a 5/24 if Chase and Amex slow down their approval rates (which they have been doing), and Barclays/BofA/Wells Fargo are offering alternatives.

“For my trouble I will earn 4K (1x on the mortgage) +3K Bilt points on the spend, so 7K for a 3K spend ”

You also paid your mortgage. So, $7k spend for 7k points. A 1.0x card.

Your MR to AF comparison example should include $120 for the 3% mortgage fee not covered.

B2 sounds like it could be a loser unless youn consider Bilt Cash and its usability at restaurants.

I’m assuming the mortgage would otherwise be paid by auto debit or check. So only $3K spend.

I think the changes can be summed up as this: earing points on your rent is no longer a low-effort affair. For existing rent customers, this is obviously a big downgrade; however, this will be a big upgrade for others who can make the math work, especially mortgage payers.

Normally I’m not a fan of big corporations fattening their profits, but in this case I don’t mind and am actually appreciative of how flexible the new system is, even if it’s convoluted. Given the massive losses that Wells Fargo suffered and the demise of Mesa, it’s obvious that the old system was too good to last and would have eventually bankrupted Bilt after Wells Fargo stopped absorbing their losses. The new system rewards you for big spend on the card without punishing you if you don’t meet a minimum spend requirement. Don’t met the 75% minimum spend requirement to unlock your full rent/mortgage points? No problem, you’ll still get a prorated amount or can pay the difference.

My head is still buzzing with this announcement, and I would love if the FM team could do some analyses to help us out! Below are some of my ideas.

1. Does anything about today’s announcement change anyone’s mind on whether to use Bilt cards for rent/mortgage vs using the Atmos card?

2. Elsewhere I’ve read that you can only have one of these cards. I can’t think of a single good use case for applying for the Blue Card; that card seems almost totally worthless given the high-spend requirements to unlock fee-free points. However, the Obsidian and Palladium both have strong use cases. Which would you guys prefer?

3. Now that Bilt Gold is easy to get, would you consider going for Platinum to be worthwhile if you wouldn’t otherwise acquire it organically?

4. The Palladium card is obviously a copy of the Venture X card. Given that Bilt points are more valuable than Capital One points, is switching from the Venture X to the Palladium a no-brainer? As things currently stand, does this hurt Capital One’s long-term usefulness due to opportunity costs from the Palladium? I know that the Venture X has a travel credit that’s leagues better than the Palladium, but is that enough to keep it?

Thank you!

Palladium is indeed like a knockoff VX with better transfer partners (but, no C1 lounge access).

I don’t see why this beats Vx. The $300 spend is relatively easy (though I’m still struggling with $30 left through March), coupled with the 10K annual bonus points that compensates for the $95 net fee. 2x everywhere and no nonsense about trying to stop on the .75x mortgage dime. C1 lounges are icing on the cake or key benefits depending on your travel patterns.

We’ll surely have more analysis to come, and I expect the podcast this weekend will likely be about it, too. We’ve all had spirited discussion about all of this behind the scenes, so no one of us has a single opinion of all of us.

To hit a few key points from your questions:

1) I think you can only pay mortgage with the Bilt card. You’ll still be able to pay rent with other cards, but I don’t think the Atmos card is a comparison point for mortgage.

2) I can definitely see a crowd for the Bilt Blue card: someone who doesn’t spend a ton and isn’t heavily into travel rewards but does spend on rideshare, home delivery, and Bilt Dining restaurants. A single young person living in a city (where there may be fewer places that code as grocery stores) might not spend enough on grocery for the $95 AF to make sense on the Obsidian card, but if they can get 4% back that they could use for things they are paying for anyway and also get 1x that they could maybe one day learn to use or use to book occasional travel for 1.25x, that might be as good to them as a 2% cash back card. However, the real question mark is how easy it will be for them to use the Bilt Cash: I think there are going to be limits that might not make it as useful as I’d hope. So this is only a theoretical use case — I’d probably not be recommending it to that young single city dweller until we know more.

Between Obsidian and Palladium: I easily spend more than $25K per year on otherwise unbonused purchases. With the Palladium card, that would be enough to get Bilt Gold status, 50K points based on 2x spend and $1100 in Bilt Cash ($1,000 from spend + $50 for every 25,000 points). Together with the $200 in Bilt Cash that the card provides every year, that would be $1,300 in Bilt Cash. I could theoretcially use that to offset the fee to pay up to $43,333 in rent/mortgage, which would yield me a total of 93,333 points each year. Even if I didn’t use the hotel credits, that seems like a pretty good ongoing return for the $495. And with Gold status, maybe I’ll be able to take advantage of a compelling transfer bonus. I think that’s a pretty clear winner for me personally.

That said, 3x on $25K of groceries that I could transfer 1:1 to Hyatt, Alaska, JAL, etc also sounds nice (and it would earn $1,150 in Bilt Cash ($1,000 on $25K spend + $50 for each 25K points). That’s certainly not a bad alternative.

I *think* what we’ll likely do is have one of us go Palladium (probably me) and one go Obsidian in my household. But don’t necessarily take that to mean that *you* should. At this point, I think Bilt Cash is a big gamble if you don’t either have a mortgage/rent or know someone whose mortgage/rent you could pay.

Sorry, hit post before I was done with that comment.

3) I don’t know. I think Gold is certainly attainable for many people. The $50K bar for Platinum is obviously a tougher bar to clear. I think the answer on this will really depend on how difficult it is for you and whether you can pay enough in rent/mortgage to make it worthwhile.

4) I don’t think it’s a no-brainer between VX and Palladium. I think it’s actually a tight race. There are reasons I might prefer Palladium, but there are reasons I might recommend VX for many people. Stay tuned — there will be more of that debate to come.

Yeah, I decided that the first year SUB made the Palladium OBVIOUSLY positive value (I have hotel stays in H1 and H2 2026 where Bilt Cash + hotel credits can be put to obvious use) and I could use 2026 to evaluate which one stays, VX or Palladium.

I also have zero intent to pay rent with the Palladium because I will use the Bilt portal for Atmos points + SUBs in 2026. The 3% charge is a charge no matter what.

Your math is wrong. 25,000 * 4/3 = 33,333.

Given that you could earn 50,000 points at 2x on $25,000 of unbonused spend, you’re effectively buying 33,333 Bilt points for $495 (1.49 cpp).

Math gets even worse if you divert spend for any reason. Let’s say you spend $15k one year. Now you’re buying 20,000 points for $495, or 2.475 cpp.

Long story short, to make these cards make sense, you have to spend nearly exactly 1.333x your rent/mortgage amount every month on unbonused spend. Too much, and you’re earning 1x, which is garbage. Too little, and you’re wasting money on annual fees.

Realistically, this is too much micromanaging for the marginal potential benefit over the various 2x or better cards.

I hate to reply to myself multiple times, but this sentence needs editing: “Too much, and you’re earning 1x, which is garbage.”

That’s true for the $0 and $95 cards.

For the $495 card, it’s safer to overspend since your floor is earning 2x. There is still the risk of paying $495 and having to commit to a certain level of unbonused spend on this card for an entire year.

I think this is the best tl;dr so far: the $495 card could be worth it, especially for low(er) mortgage payments, but the holy hell the micromanaging, on TOP of all the AMEX plat/gold couponing, on top of all the chase/usbank cashbacks. I’d love an additional points of necessary (vs MS) spend, but my god, what an absolute time suck.

More should be clear within a few days, but this has radically shifted the Bilt landscape where rent/mortgage seems to really be the secondary option and the primary question for optimizing value is “how useful is that Bilt cash?”

If you have a card with the $50 or $200 Bilt portal hotel credit I’d be trying to stack that with redeeming the 4% Bilt cash to get two free stays a year. If that can hopefully all be used on loyalty eligible stays, I’d also get elite nights, status benefits, and hotel chain points from my covered stay which really adds to the value proposition there. 2-night minimum stinks but with no luxury hotel requirement I’d be burning it on something more basic like a Hyatt Place or Regency, Residence Inn, Marriott Courtyard, etc. There are enough times where I’m booking a cash stay at one of these because the points value isn’t there that I could easily switch to making the booking through Bilt and have that stay use up credits and get covered by Bilt cash.

With the Lyft partnership the remainder of the 4% would probably cover my domestic rideshare needs for a year when traveling.

Somehow Bilt has made me more interested in their cards while simultaneously nerfing the old rent payment scheme and most of the interest in mortgage payments.

Slow down: as I’ve noted in other comments, I don’t think it’s going to be as simple as using Bilt Cash to cover all your domestic rideshare needs. I think there are going to be limits.

Fair, there’s still quite a bit of unknowns. Which is not exactly trust building for a new product launch – I’d say Bilt should have figured this out already, but they aren’t exactly unique lately as US Bank still has us waiting on our exciting new Altitude Reserve transfer partners.

It’s still the same question – how useful is the Bilt cash? We don’t know yet. It could be exciting, or more tepid.