NOTICE: This post references card features that have changed, expired, or are not currently available

Update: Based on reader comments below, my situation is an anomaly and there is not a new Freedom rule. Thanks for adding your recent data points!

Yesterday afternoon, we reported on a disconcerting piece of inside information we received about Chase’s continued exploration of an end to Ultimate Rewards points pooling across accounts (See: Leak: Chase may end Ultimate Rewards pooling). I certainly hope that doesn’t come to fruition, though the timing was interesting as it lined up with another potential negative change I ran into this week: I applied for the Freedom Unlimited 3X offer and was told several times this week that Chase has a new restriction that disallows customers from opening a new Freedom product if they currently have any Freedom card. It would be rash to declare a new rule based on anecdotal evidence, but my experience over several days this week indicates that this rule may indeed be a reality. Chase Sapphire cards have a similar approval restriction (See: Chase ends ability to double up Sapphire Reserve and Sapphire Preferred bonuses). If the Freedom cards are now also restricted to one per customer, it would certainly be a blow to those who don’t currently have both Freedom cards. This process is a work in progress and will need an update, but here’s the story so far…

Day 1: Product Change from Freedom Unlimited to Freedom

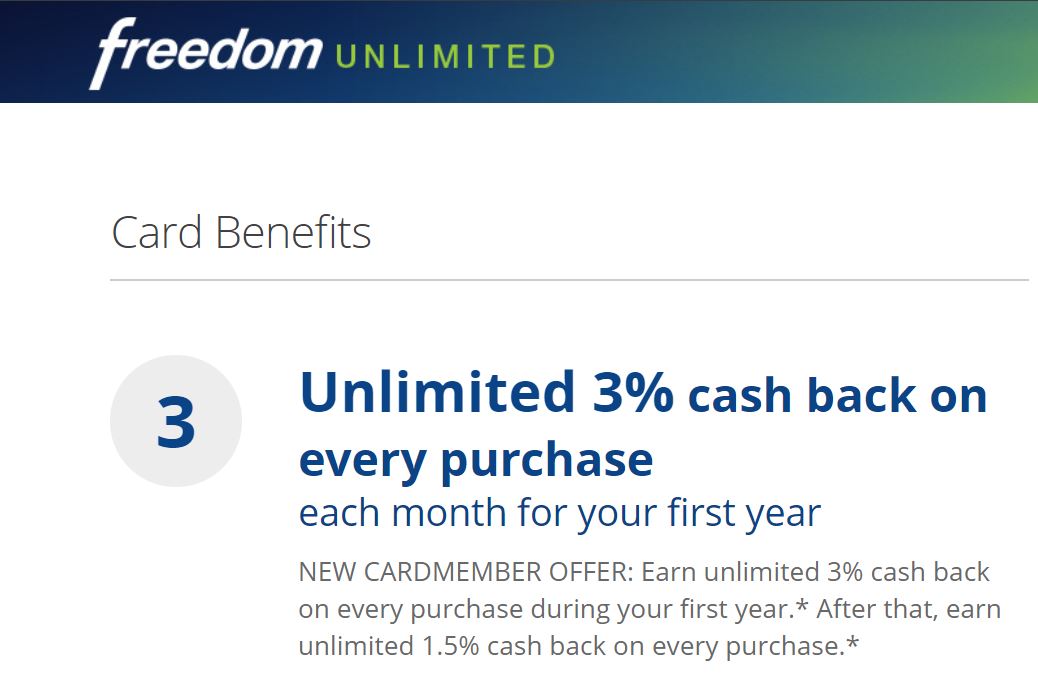

I began the week with a Freedom Unlimited card in my collection of Chase cards. I had previously downgraded to the Freedom Unlimited, so I have never gotten a signup bonus on the Freedom Unlimited. When the new 3x offer came out (See: Holy smokes….Chase Freedom Unlimited 3x everywher first year), I saw too much value in it to pass it up. Three percent back for one year with no annual fee is already a great deal even without point pooling; the fact that I can also (currently) combine those Ultimate Rewards with a premium Chase card like the Sapphire Reserve to get 1.5 cents per point towards travel booked through Chase Travel℠ or send them to Chase transfer partners via any of the premium Chase cards (Sapphire Preferred, Sapphire Reserve, or Ink Business Preferred) makes it an incredible deal in my book.

Knowing that Chase will not allow you to open a product that you already have, I knew I would have to first product change my Freedom Unlimited to something else in order to apply for the new Freedom Unlimited 3x offer. My no-annual-fee options were the Chase Freedom card (with rotating 5x categories) or the no-fee Chase Sapphire card (which is only available for product changes, not new applications). I wouldn’t have much use for a no-fee Sapphire card, but figured the Freedom would come in handy (especially considering the great 5x categories this quarter). So I called Chase in the afternoon of Day 1 to request the product change. The rep confirmed that the change might take a couple of days to show in my account, but if I continued using my card it would earn based on the Freedom structure and I would receive my new Freedom card within 3-5 days.

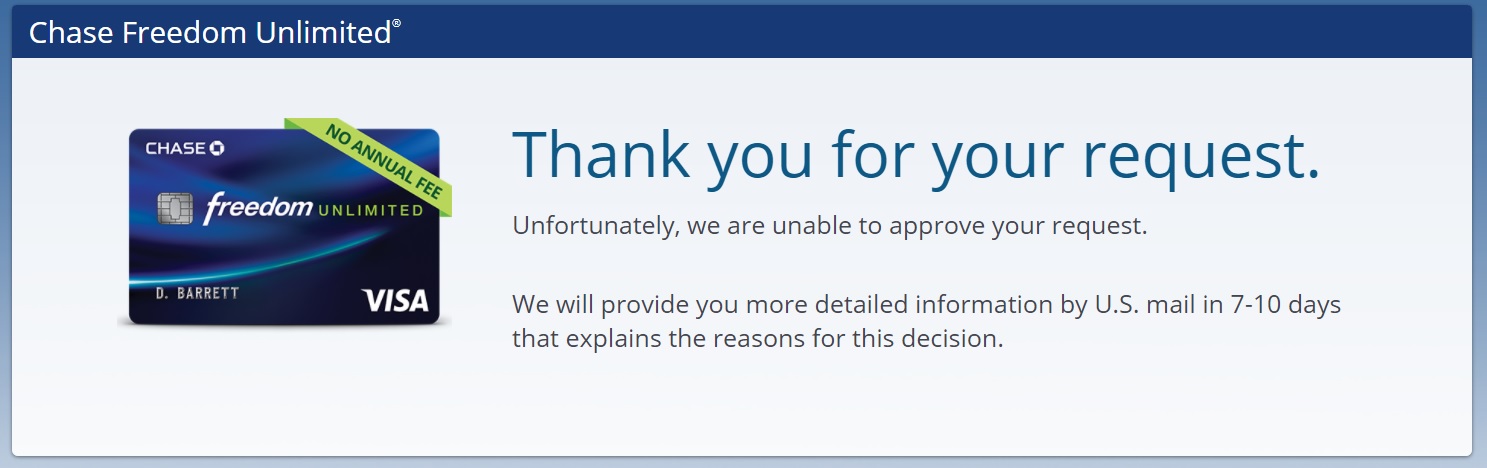

For the next few hours, the card still showed as a Freedom Unlimited in my online account. However, late in the evening (sometime after 8pm Eastern), the account changed to a regular Freedom card. I was able to successfully activate the current quarter’s 5% categories. I took this as a sign that the product conversion was complete, so a few minutes later I applied for the Freedom Unlimited. As shown above, I received an instant rejection saying that Chase was unable to approve my request and I would hear more by mail in 7-10 days.

Day 2: Reconsideration call

First thing the next morning, I called the Chase reconsideration line (you can find the phone number at the top of the “Chase” section on our Best Offers page). After verifying my identity, the rep put me on hold to look at my application. She came back a couple of minutes later to say that my application wasn’t approved because I already had a Freedom product. I responded that I have a Freedom, but I was applying for a Freedom Unlimited. She acknowledged that she could see that I had the Freedom with rotating 5% categories, but since I already had a Freedom product, I could not be approved for another Freedom product.

This didn’t make sense to me as I know plenty of people (including many readers) have both cards. I pushed back for more information. The representative told me that policies are changing all the time and that there had recently been a change that prevents a customer from opening a second Freedom product. This caused my application to be instantly declined without even pulling my credit.

I offered to close my Freedom if it would facilitate the approval of the Freedom Unlimited application. The rep put me on hold and came back to say “Good news” – this would be possible. I next asked her to confirm the new cardmember bonus I would be receiving. I wanted to make sure I would still be getting 3x for a year and it wouldn’t be treated like a new application without the signup bonus attached. She put me on hold and came back to say that I would not qualify for any new cardmember offer because I currently hold a Freedom card. She was essentially offering to product change me rather than closing a card to approve my application (which makes sense since they hadn’t pulled my credit). I politely ended the call without making any changes to my accounts.

Day 2: Product change Freedom to Sapphire

In the afternoon on the same day, I called Chase (via the customer service number on the back of one of my cards) to product change my now regular Freedom card to a no-fee Sapphire card. This change was no problem and only took as long as it takes to read the many necessary disclosures.

I logged into my account a few minutes later and it was now a plain Chase Sapphire account.

Day 2: Evening Freedom Unlimited application

Day 2: Evening Freedom Unlimited application

In the early evening on Day 2, I decided to go ahead and apply again. My online account was reflecting a plain Sapphire card and I was hopeful that this would free me up to be approved for a Freedom Unlimited. Unfortunately, I got the same instant rejection I had gotten the first time.

I called the reconsideration line and I spoke with a rep who told me that application #2 was also denied because I already have a Freedom card. I told her that I didn’t have a Freedom card. She sounded surprised (“Are you telling me you don’t have a Freedom card??”), so I explained that I had product changed it earlier in the day to a Sapphire card. She told me that it was common for the computer system to still show the old card account for a while after product changing, even though my online banking showed the Sapphire card. I asked her if she knew a timeline for when my Freedom card would be out of the system and she couldn’t say. She did say that there would be no harm in waiting and then applying again. She confirmed that Chase had not pulled my credit because the system issued an instant denial for already having a Freedom account — repeating the line that a customer can not have two Chase Freedom accounts.

Day 3: Another day, another application

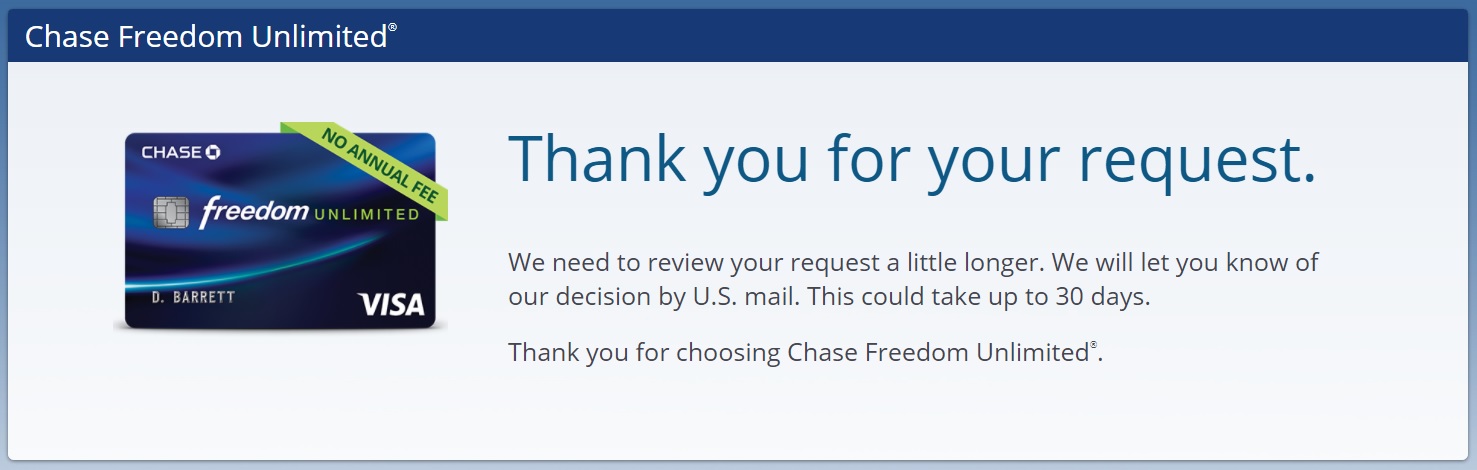

I decided to wait it out more than a full 24 hours after my product change to the Sapphire card before attempting a third application for the Freedom Unlimited. I had product changed from the plain Freedom to the plain Sapphire in the afternoon on Day 2. I waited until late evening on Day 3 and decided to take another shot at a Freedom Unlimited application. This time, I got a different result after submitting the application.

Now that’s something I can work with. Sure, an instant approval would be nice – but I’m hopeful that at the very least I can shift a chunk of credit from my plain Sapphire card to open a Freedom Unlimited.

At the time of writing, the application status line still says I will hear from them in two weeks, which is a good sign according to this flow chart, so I am going to wait this one out.

The takeaways

When the first rep told me that I couldn’t get approved for a Freedom Unlimited because I currently held a Freedom product, I didn’t initially believe it. I find that phone reps are often incorrect and that banks will tell you a convenient reason for denying your application (e.g. “too many inquiries”) rather than the real reason (our risk model predicts you’re going to spend like a sailor and then use your rewards balance to disappear to a small tropical island that doesn’t have an extradition treaty). I was skeptical about a new policy limiting customers to a single Freedom card until I found that they hadn’t pulled my credit – a sign that they had no intention of approving me for some reason.

When the second application, a few hours after a product change to the no-fee Sapphire card, was also denied and I received the same rationale from the reconsideration rep, it started to really get some teeth in my eyes. The fact that the third application actually went through, when the automatic approval system clearly recognized that I no longer had a Freedom card, seems to back up the existence of a new rule.

Things we don’t know

1) Is this indeed a new rule or just my anecdotal experience?

It’s always hard to determine whether or not a rule exists based on one or two datapoints. If any readers have either a Freedom Card or a Freedom Unlimited card and recently applied for a second Freedom card (let’s say within the last month), I’d love to hear your results. Comment with the approximate date and your success/failure in applying for a second Freedom product. It’s certainly possible that my experience is an anomaly.

2) Can you still product change your way into two Freedom cards?

While I think it may be true that Chase won’t allow you to open a new Freedom product if you currently have any Freedom product, I’m not sure whether or not it is still possible to product change your way to a second Freedom product. In other words, if my Freedom Unlimited application is ultimately approved, can I then product change my Sapphire card back to a Freedom card?

I certainly intend to test this if and when I am able to get my Freedom Unlimited approved. To be continued here….

Bottom line

Update: Based on reader responses below, the auto-denials were likely due to how soon I applied after product changing. There clearly isn’t a new rule, which is great news for those pursuing both Freedom cards.

I hesitate to declare a new rule has been confirmed based on my experience alone. Still, with two instantly-denied applications without even a credit pull and then a third application that ultimately went through after my Freedom cards were out of the system, it seems reasonable that the reps may have been correct. If true, this would be a blow to those looking to Amass Ultimate Rewards as having both a Freedom card for its rotating 5x categories and a Freedom Unlimited for 1.5x everywhere is a great way to rack up rewards without an annual fee (provided you also pay an annual fee on a third premium Chase product in order to combine points to transfer or use for greater value).

The good news is that I do not currently see language on the Freedom applications limiting the signup bonus based on having other Freedom products. When Chase instituted the new restrictions on the Sapphire cards, they ended the ability to get the signup bonus on a new Sapphire product if you have received a signup bonus on any Sapphire product in the past 24 months. The absence of that type of language on the Freedom cards means that Chase does not appear to be restricting you to one Freedom signup bonus in the past 24 months, though they may be limiting your ability to open a second Freedom product. To be continued…

Rakuten credit card bonuses (Bank of America boosted up to $275)")

I really don’t understand Chase. I am retired with no outside income other than Social Security and rental property income (don’t even take income from retirement funds). Applied for the CSR and CFU within 2 weeks of each other and was instantly approved for both. My wife is employed with FICO scores from all 3 credit bureaus over 800. She applied for the Ink Business Cash (rental properties) and had to jump through all kinds of hoops to get approved – took more than 2 weeks of phone calls and sending in documentation. As I am 7/24 and really want the Freedom for the 5X bonuses, applied for one for my wife thinking she now has a history, albeit a short one, with Chase and shouldn’t be a problem considering her income and credit score. She wasn’t rejected but didn’t get instant approval either. Still waiting on Chase to make a decision. They did do a HP on Experian on her so I am hoping she gets approved but still can’t figure out why she doesn’t get instant approval and I did??????

[…] A new card is said to be coming, and Greg makes some interesting speculation about what it all means — and what card might be coming next after that. If you are under 5/24, you will definitely want to check this out as it should play into your strategy moving forward. I am still under 5/24 myself, but I think I’ll pass on the new offer in the hopes that Greg’s guess about the next one to come materializes in the next few months. At the moment, I’m still patiently awaiting an outcome on my Chase Freedom Unlimtied 3X everywhere app…. […]

Can you hold the CSR and the no-fee Sapphire?

[…] Is Chase now restricting Freedom cards? […]

[…] was an interesting post today on Frequentmiler looking for data points about whether Chase is stopping to allow users to apply for a second card […]

I’ve got both Freedom cards. So just waiting for a better signup bonus for the CSR card. I’m hoping for at least 75k. Is that hoping for too much…

Probably, considering they lost a ton with the 100k offer.

[…] was an interesting post today on Frequentmiler looking for data points about whether Chase is stopping to allow users to apply for a second card […]

I downgraded my CSP to a Freedom Unlimited last month. I originally got the CSP in 2012, so I am planning to reapply. In the course of doing the downgrade, the chatty rep said to wait until after the next statement closing before applying, so that everything is “cleared.”

You were just too trigger happy.

Hi Nick: Is there any reason to just close the existing FU and move credit line to existing F card? Wouldn’t this be easier?

I just successfully product changed my Sapphire to a second Freedom card.

Definitely 4/24 here with a Freedom, Ink Cash, and CSR. Applied for CIP (auto approved a few days later) and then CFU on 4/20. CFU took 5 days (3 bus) for auto approval. Brings me to 5 pers and 2 business Chase cards. Being CPC may have helped, don’t know.

Yet another data point: My wife has held the Chase Freedom since 2014 and applied for the Freedom Unlimited on Saturday 4/21. Instant approval with the card showing since Monday in her account.

What’s your 5/24 status before applying? I thought the FU was subject to 5/24 rules. Is it not?

It is. I’m under 5/24.

“I’m under 5/24.”

Respect!!!

If you get shutdown will you let us know…

I hope you aren’t shutdown Nick, but I wouldn’t be surprised if you are. Poking the bear

I was instantly approved with another Freedom open since 2006 (was a different WaMu card that was converted by Chase into a Freedom around 2012 IIRC). I would guess there’s either a time between new Freedom products rule or you simply tried to move the process along too fast.

This is just stupid. You applied too fast 2 times. And then doubled down by writing this article too fast. Ridiculous…prove something more than idiocy before you write “click-bait” next time…

This times 1000. Nick, chill. Lay off the coffee or whatever you’re on.

The system probably still saw your Freedom as a CFU on your first app.

And putting out articles like this just encourages noobs to go fast and break things. You have to be patient and stealthy in this game.

I understand what you’re saying. We discussed what system might see or not see and I certainly considered whether re-applying would do more harm than good. We decided it made sense to find out and that there wasn’t much harm to be done if they were instantly declining without actually considering the app. If they had pulled my credit on the first app, I’d have stopped there and waited to see. Since there was no pull on the first two, it seemed notable and worth finding out whether there was something to what they were saying.

Thanks for replying, I see you added the update saying there isn’t a new rule from Chase. And thanks for “taking one for the team” It is good to test things out from time to time, but keep in mind that if there were a list of MS rules, “go slow” would be at the top.