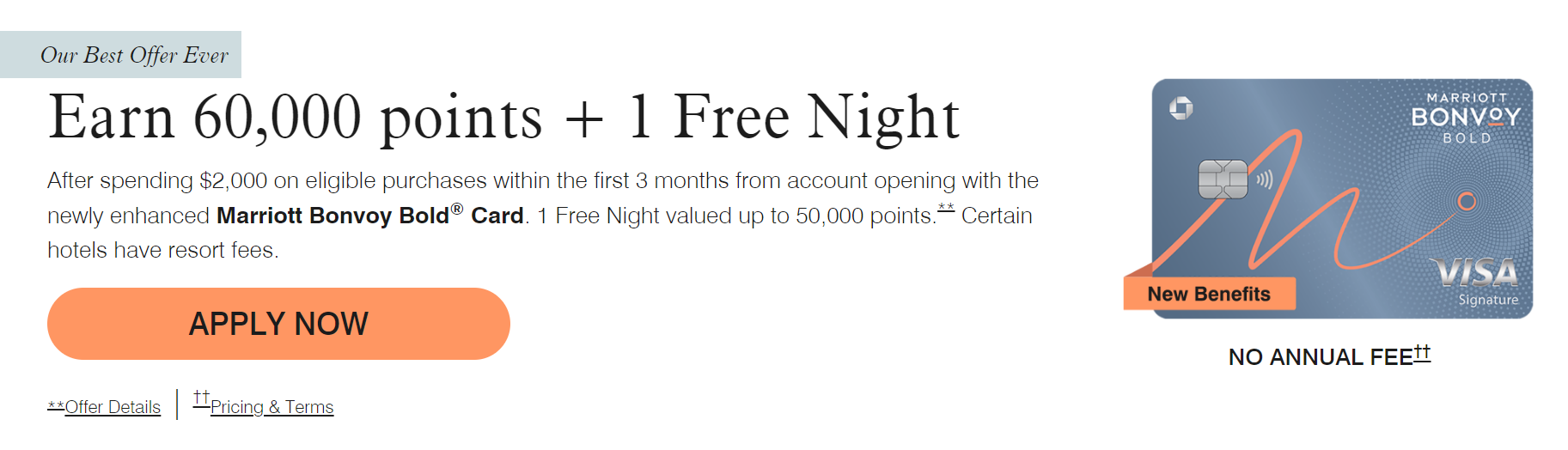

It’s back! The best-ever welcome offer of 60,000 points and a 50k free night certificate after $2K spend has returned on the Marriott Bold card. Given the minimum spend required, this is a very good offer, much better than the previous one of 30k points with no free night certificate.

Chase has also added a modified “Pay Yourself Back” feature the Bold card, where you can use Bonvoy points to pay for up to $750 in airline and Marriott hotel charges per year at a rate of 0.8 cents per point.

The Offer & Key Card Details

Click the card names below to go to our card-specific pages for more information and to find a link to apply.

| Card Offer and Details |

|---|

ⓘ $205 1st Yr Value EstimateClick to learn about first year value estimates 30k Points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer 30K points after spending $1k on eligible purchases within the first 3 monthsNo Annual Fee This card is subject to Chase's 5/24 rule. Click here for details. Recent better offer: 60K points + Free Night Certificate after $2K spend (Expired 7/17/25) FM Mini Review: The best use for this card is probably to downgrade from the Ritz or Boundless card to avoid the annual fee. That way, you can always upgrade again when you need the annual free night or other perks Earning rate: 3X Marriott Bonvoy ✦ 2X grocery stores, rideshare, select food delivery, select streaming, and internet, cable and phone services ✦ 1X everywhere else Card Info: Visa Signature issued by Chase. This card has no foreign currency conversion fees. Noteworthy perks: Automatic Silver status ✦ 5 nights of elite credit each year ✦ Complimentary Instacart+ for 3 months (must activate by 12/31/27) ✦ $10 monthly Instacart credit See also: Marriott Bonvoy Complete Guide |

Bold card now eligible for Pay Yourself Back

Somewhat bizarrely, Chase added a modified “Pay Yourself Back” benefit to the Bonvoy Bold card – but not to any other Marriott cards in its portfolio.

As of now, all Marriott Bonvoy Bold cardmembers can redeem Bonvoy points for a statement credit to cover purchases made directly with airlines or at hotels that participate in Marriott Bonvoy, up to a total of $750 in purchases per year.

Interestingly, the rate that Marriott is offering is 0.8 cents per points (cpp), slightly higher than our current Reasonable Redemption Value for Bonvoy points of 0.7. This creates a situation for lower-value redemptions, where it would actually be a better value to use cash for the hotel and then pay yourself back at 0.8cpp while also earning points on the cash booking.

My assumption is that Chase is using the Bold card as sort of a test case before deciding whether to roll this out on all Chase Marriott cards.

Quick Thoughts

This new offer on the no-annual fee Bold card is actually pretty good, with a maximum value of 110K in points. The 50K free night certificate should get you around $350 in value domestically if you’re able to use it wisely and 60,000 points are worth ~$420 according to our reasonable redemption values. ~$750 in expected return on $2,000 in spend is excellent.

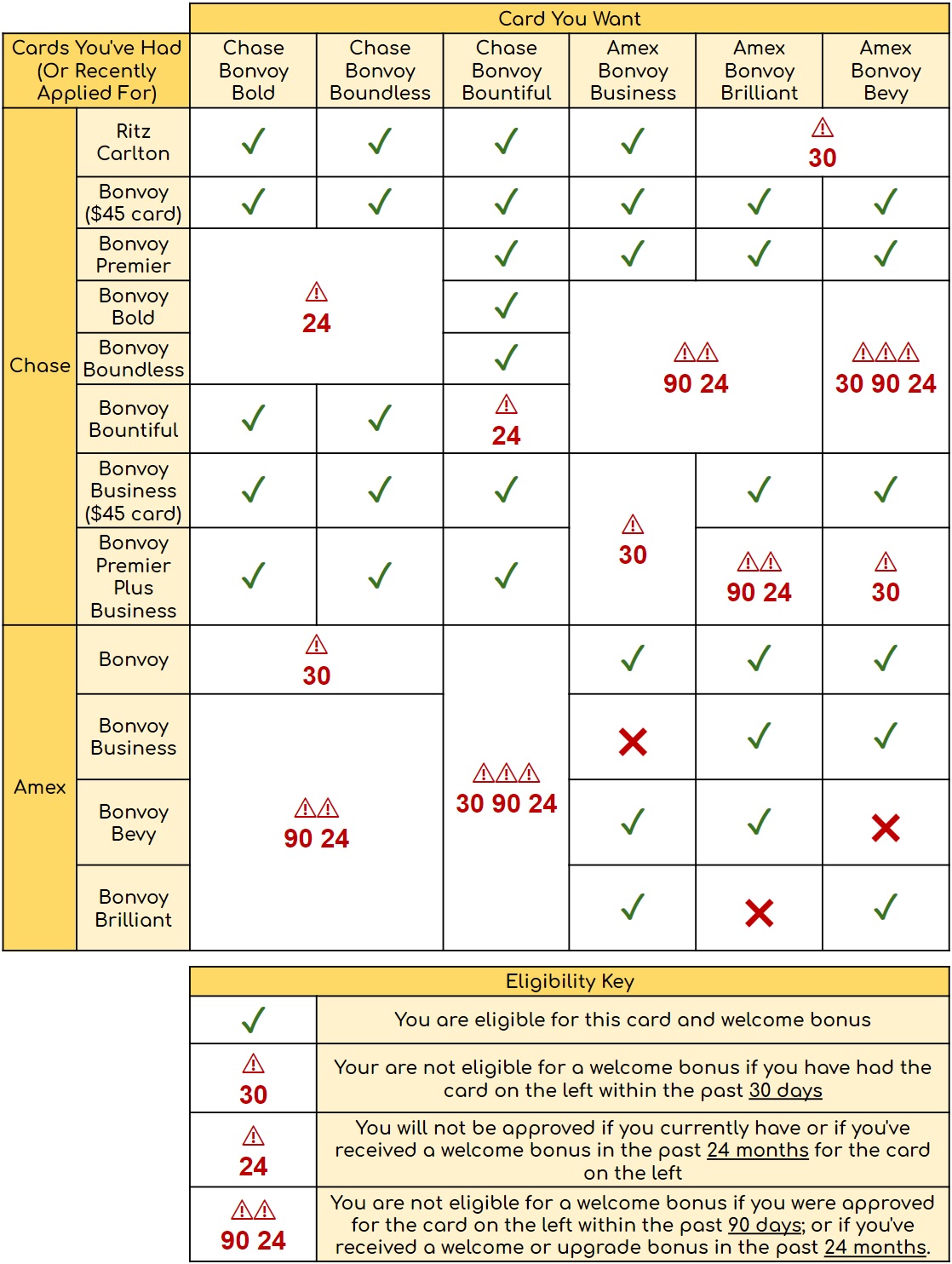

With the new welcome offer, it might be the ideal time to use the Bold as a means to upgrade to the Ritz-Carlton Visa Infinite card down the road. Those who want the Ritz card will need to wait a year from opening one of the Chase Marriott cards to request a product change, but (so far) it’s still possible to do it.

The changes to the card are fairly banal overall. While the 2x categories have been improved, you’re still only getting two Marriott points per dollar. There’s far more rewarding options for each of those categories. The biggest “enhancement” is actually a negative: annual elite night credits have been reduced by 66% from 15 to 5. Although cardholders still get automatic Silver status, those who used the annual 15 elite nights to get to a higher level of status will now find themselves having to make up an additional 10 nights to get there.

Some might argue that awarding 15 elite nights/year on a no-annual fee card was overly-generous to begin with. Regardless of whether or not that was the case, the change still hacks away at the main reason for keeping the card after the first year and it’s hard to see how it offers much in the way of ongoing value.

|

")

")

Hi FM team, View from the Wing is reporting about widespread Marriott devaluation. Would appreciate FM’s take on it (the few properties I check enough to remember aren’t seeing anything significant, but VFTW cites some specific examples as do the comments). If there is actually a major devaluation underway, that would make this card even more interesting for those sitting on Marriott points.

Do you know whether PYB covers hotel taxes too, or just the “rate” part (before taxes and fees)? thanks!

You’ll be reimbursing a charge on your credit card, not at the hotel, so you’ll be able to use PYB on whatever is on the charge from the hotel.

If you product change out of the Boundless to the Ritz card, any guidance on how long you should wait to be clear of the 30 days requirement?

Is this available via Chase referral for P2? I don’t see it via Chase mobile app referral link any way to work around it ?

No, it’s no available via referral yet. Usually it takes a week or so.

In the past, has chase allowed a higher SUB + the referral bonus? Trying to decide if I should wait the week to test it out but also don’t want to miss out on the higher SUB