Happy 5/24! Given the holiday, we thought it would be the perfect time to remind everyone to check their Chase 5/24 status.

Chase will not approve a new card application for many of its credit cards if you have opened 5 or more cards with any bank within the past 24 months. This is known as the 5/24 rule. Unfortunately, it’s not obvious how to determine your 5/24 status. That’s where this post will help.

Chase uses your credit report to count your 5/24 status. If 5 or more less-than-24-month-old cards appear on your credit report, Chase will usually deny your application for a new card. This is true even if you have already canceled some or all of those new cards. For information about credit scores, credit reports, and credit inquiries, please see: Complete Guide to Free Credit Scores, Reports, and Monitoring

Two Easy Ways to Count Your Chase 5/24 Status

One complexity in determining your current 5/24 status is the fact that canceled cards must be counted. That is, if you opened a card within the past 24 months, it still counts against you even if you have since canceled it. Yet many tools that show your accounts only show the ones that are currently open (or they show the canceled ones separately).

Fortunately, there are at least easy ways to get your 5/24 status…

Travel Freely

Travel Freely does one simple thing: it guides you through the steps to earn points and miles through credit card bonuses. Travel Freely recommends cards for you based not just on the current best offers, but also based on what cards you’ve signed up for previously. And it’s aware of most of the known multi-card rules. For example, it won’t recommend the Chase Sapphire Preferred or Sapphire Reserve if it has been less than 48 months since you obtained a signup bonus for either one. Once you sign up for a card (and enter it on the website), you’ll get periodic emails reminding you of the due date to meet the minimum spend. Later, Travel Freely will notify you when it’s a good time to sign up for another card. Travel Freely will also notify you when an annual fee is coming up so that you can plan to downgrade, cancel, or seek a retention offer if the card’s benefits don’t outweigh the fee. You can read more about Travel Freely here.

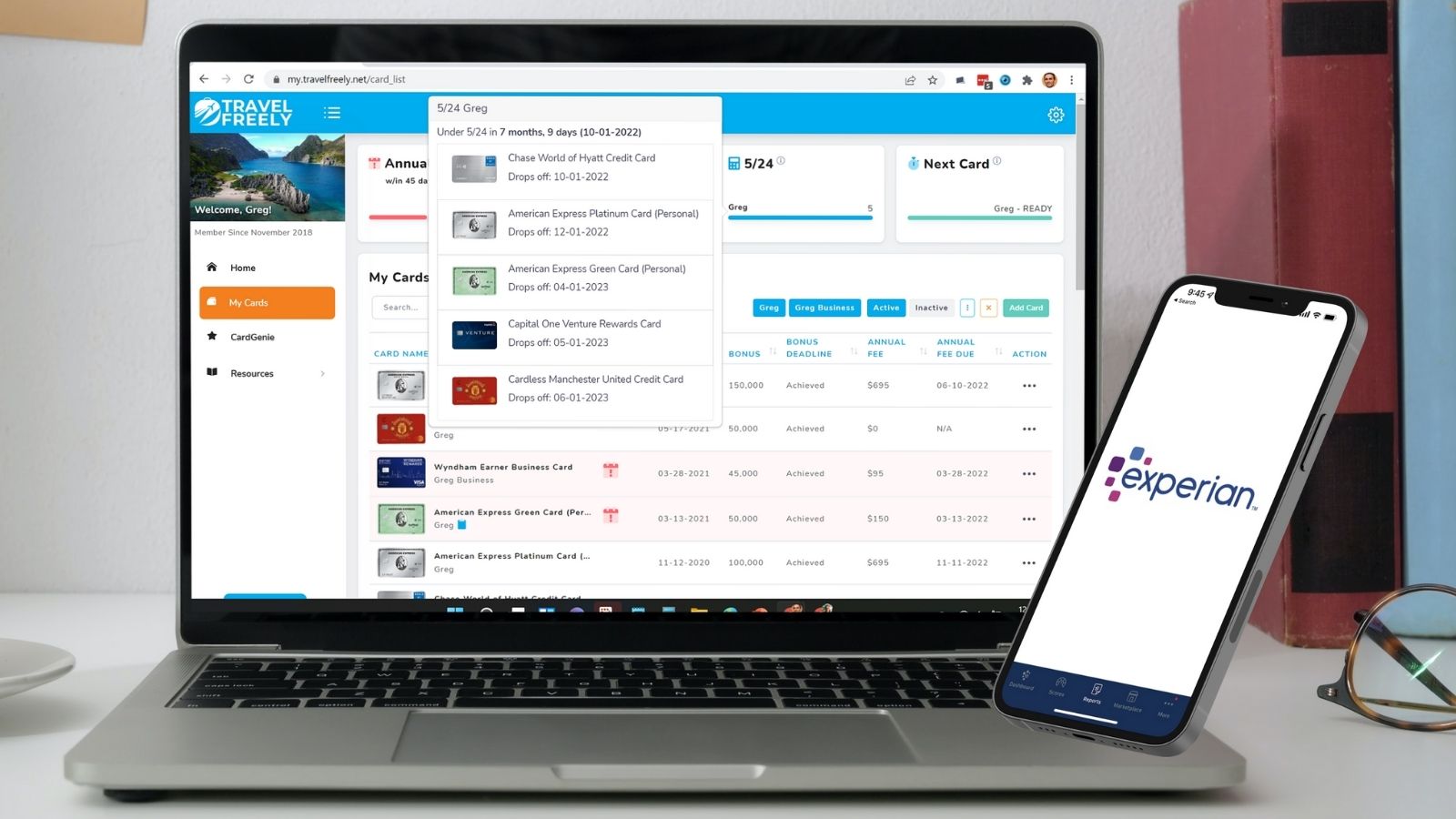

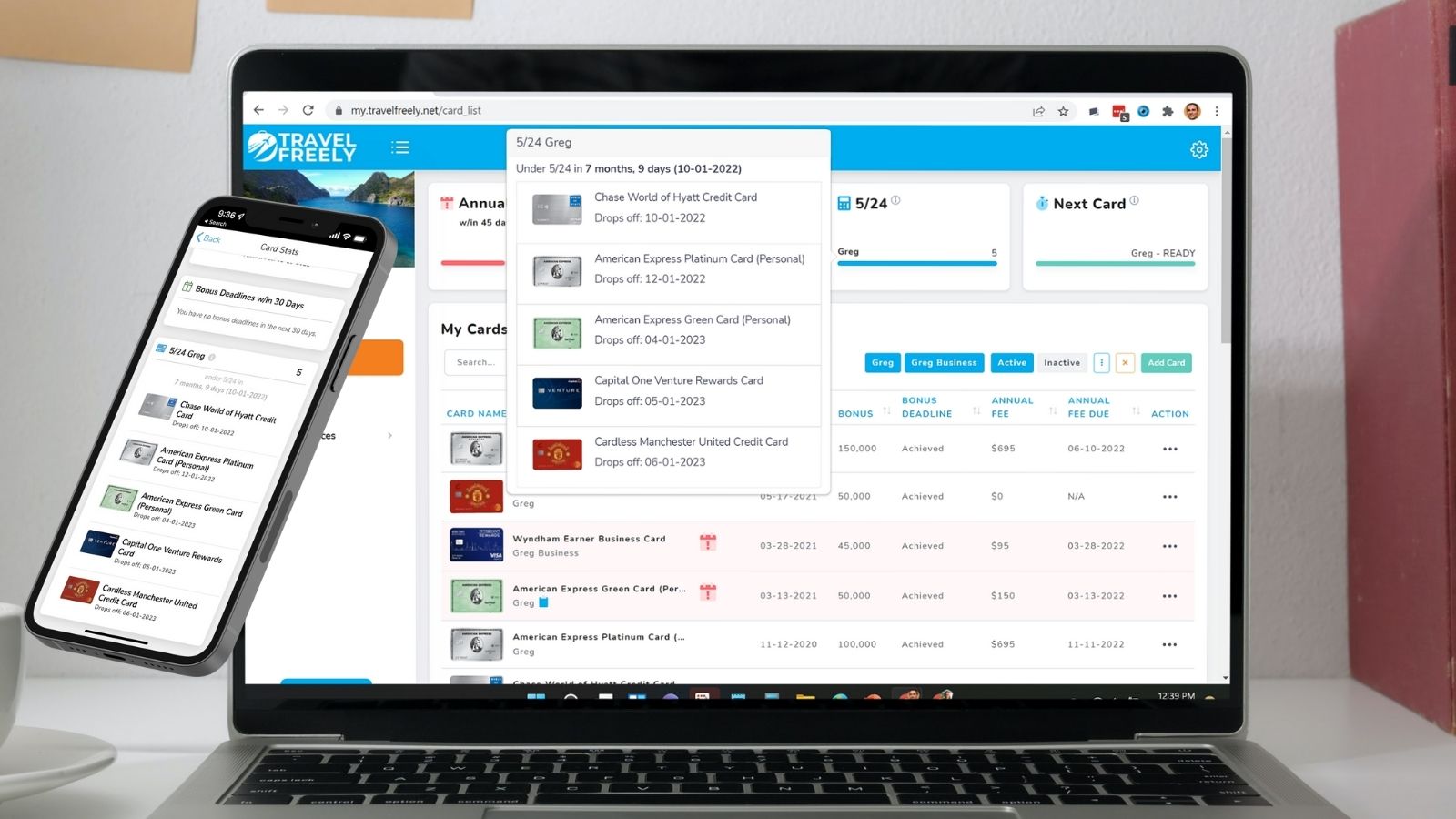

One great feature of Travel Freely is that it constantly shows your 5/24 status at the top of its card dashboard page (see above for an example). Even better, it shows the date at which you’ll be able to sign up for Chase cards again (assuming you don’t sign up for any new cards in the meantime).

To get this information to appear correctly, you need to enter details for all of your credit card signups. I recommend doing so anyway with all-new cards, since the app will provide helpful reminders. If you haven’t used Travel Freely up until now, I’d recommend entering all the cards you’ve signed up for in the past 25 months, if not longer. Yes, it can be a bit of work to get started, but it’s worth it for all of Travel Freely’s features and for the constant 5/24 display.

Sign up here for Travel Freely (it’s free).

Credit Karma

Credit Karma is one of many available free services that estimate your credit score. I particularly like Credit Karma because it gives you free access to your TransUnion and Equifax credit reports, with details about the accounts that appear on them, and, optionally, provides active monitoring of your TransUnion report.

If you haven’t already, click here to sign up for a free Credit Karma account. Disclosure: Frequent Miler will earn a commission if you sign up through this link

To use Credit Karma to get your 5/24 status, first log in, then follow these steps (hat tip Joni):

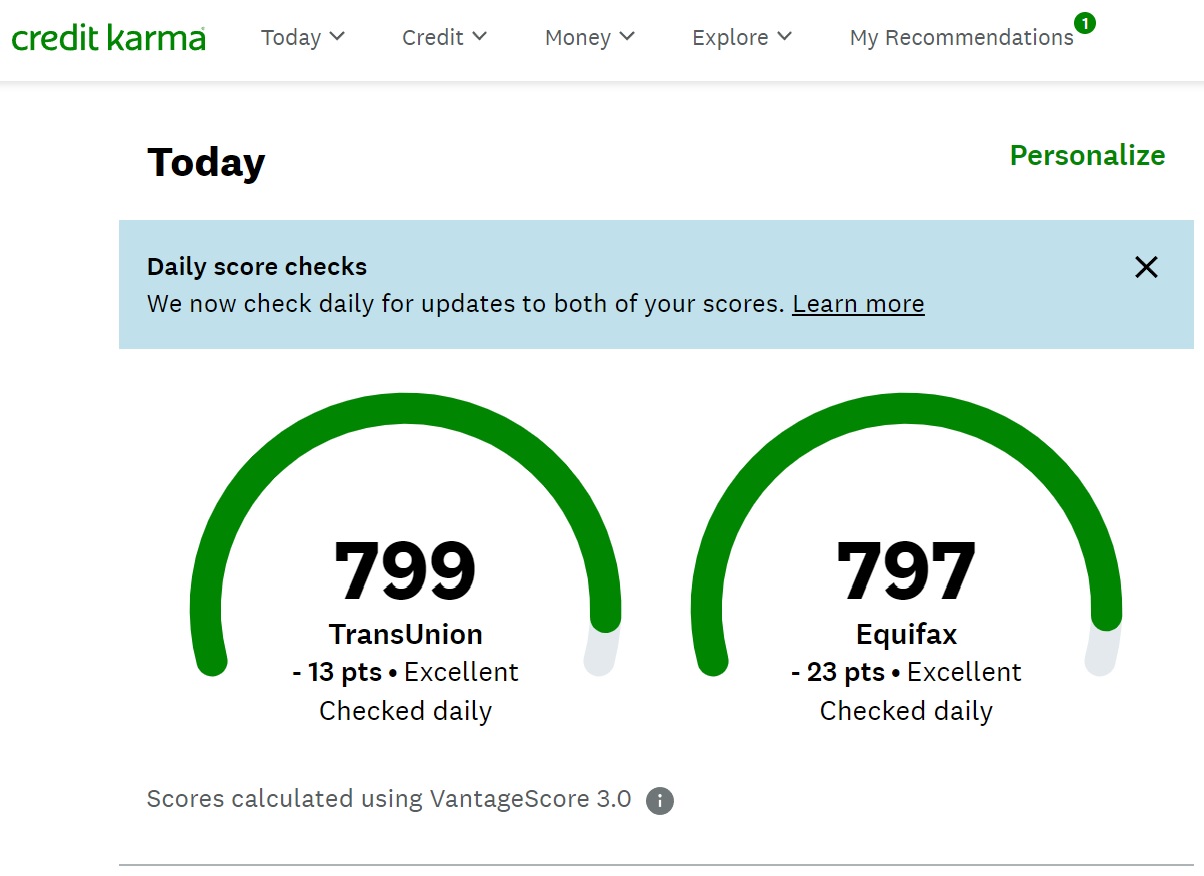

1) Click on the partial-circle graph containing your credit score

You can click on either the TransUnion or Equifax partial-circle, but I’ve found better results with Equifax.

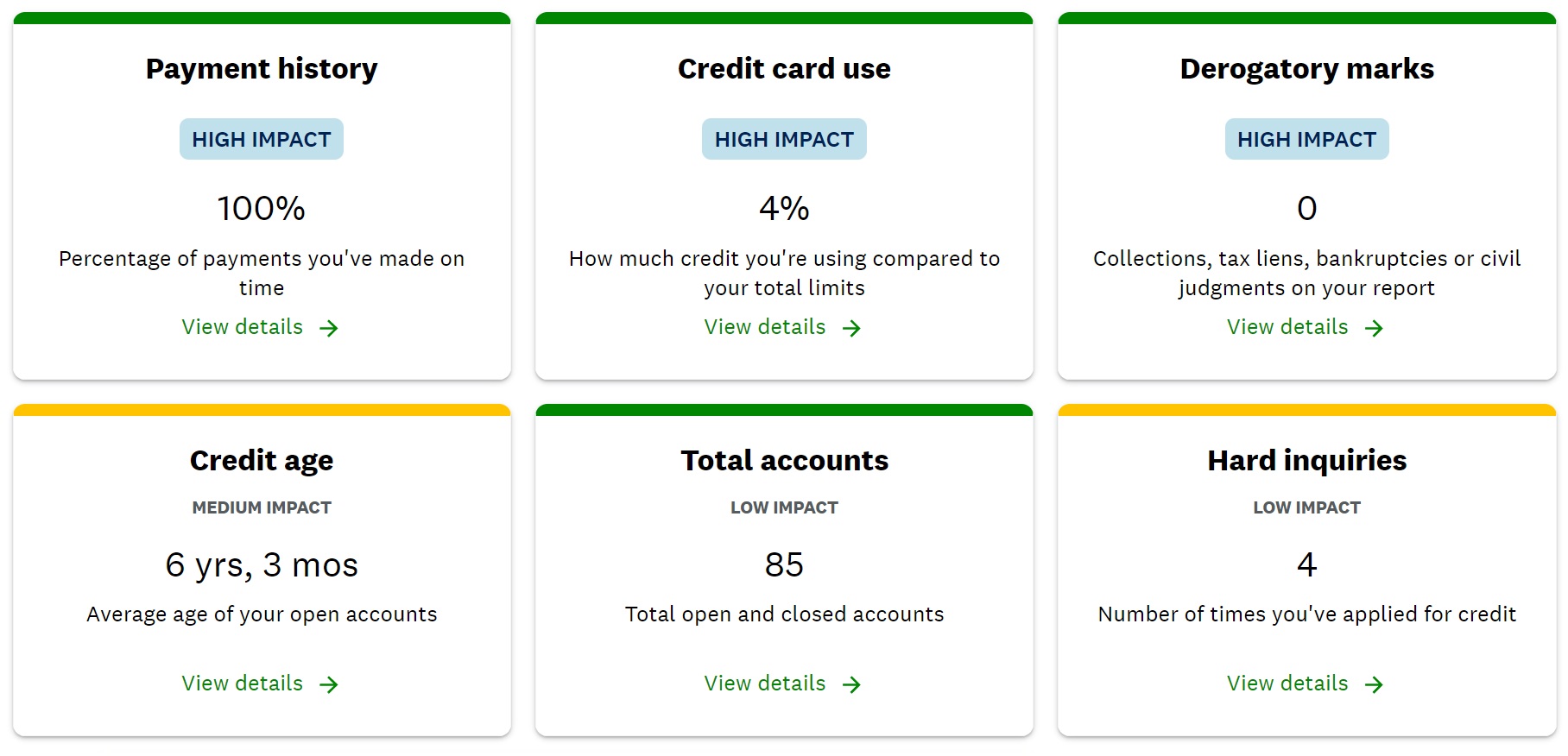

2) Click “Credit Age”

After clicking through from a partial circle on the home page, you may see a title saying “Take a look at your latest changes to see what happened.” Ignore the top section and scroll down until you see a section with boxes like those shown above. Click the box labeled “Credit age” (bottom-left, above).

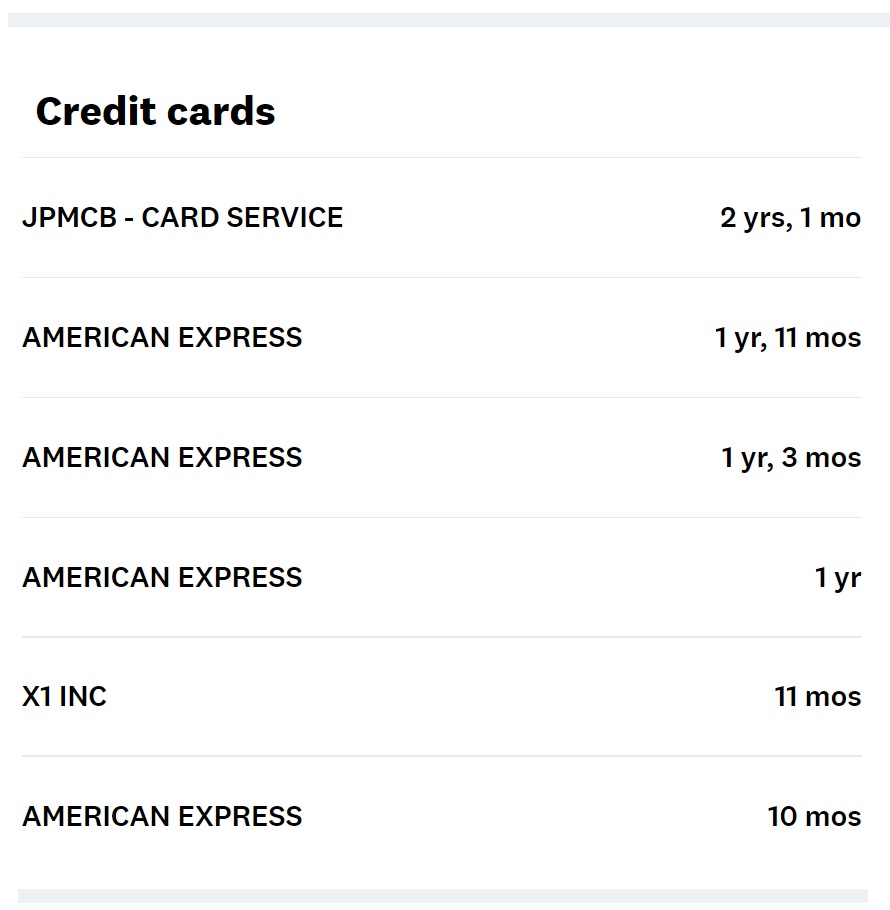

3) Count Cards Less Than 2 Years Old

Scroll down, and you’ll now see the currently open credit cards on your credit report. Count the cards that are less than 2 years old. In the image above, I count 5 cards opened in the past 24 months and 1 card opened more than 24 months ago (I didn’t show the many cards above that one that were opened earlier than that one).

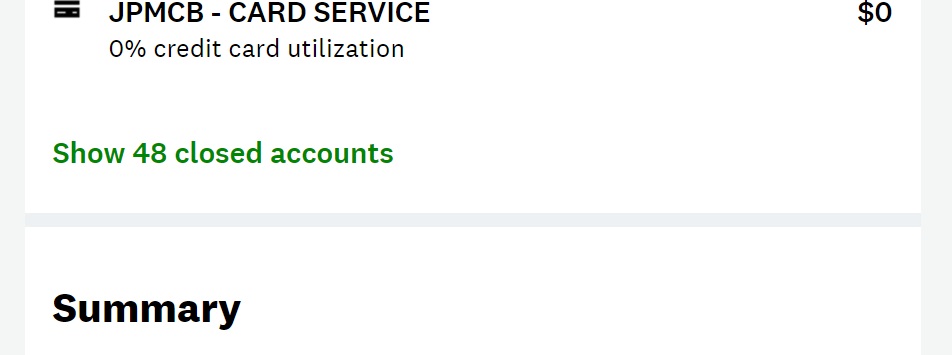

4) Add Canceled Cards

If you’ve closed any cards that were opened in the past 24 months, those add to your 5/24 count as well, but the Credit Karma technique shown here doesn’t include those canceled cards.

One way to find your canceled cards is shown above. Go to Total Accounts -> View All Accounts -> Show Closed Accounts (hat tip Biggie F). An easier option is to click here after logging in: www.creditkarma.com/accounts/closed-accounts/equifax

Unfortunately, the list of canceled cards doesn’t show when each card was opened, nor does it sort in order of closing date, but you can easily scan the list to see if you’ve closed any in the past 24 months. If so, click the card to see when it was opened. If it was opened within the past 24 months, add it to your 5/24 count.

Frequently Asked Questions (FAQ)

Do Authorized User Cards Count?

Cards where you are the authorized user count towards 5/24 when they appear on your credit report. Fortunately, there’s an easy workaround. If you are denied for a new card because you recently opened too many cards, you can call Chase’s reconsideration line and explain that you are not responsible for the bills on any authorized user cards opened in the past 24 months. Chase will then subtract these from the count and reconsider your application.

Do Business Cards Count?

Chase uses your credit report to count your 5/24 status, but business cards are not usually shown as accounts on your credit report. As a result, most business cards won’t add to your 5/24 count. You could theoretically sign up for a new business credit card every month for two years and still have a 0/24 count with Chase because Chase won’t see those new accounts.

Business cards from the following card issuers won’t count toward your 5/24 limit: American Express, Bank of America, Barclays, Chase, Citibank, FNBO, Navy Federal, PNC, US Bank, Wells Fargo.

Some issuers do report business cards to personal credit bureaus: Canadian American Express, Capital One*, Discover, and TD Bank. If you sign up for business cards from these issuers, those cards will add to your 5/24 count.

* Not all Capital One business cards are reported to personal credit bureaus. Two that do not get reported are the Venture X Business Card and the Spark Cash Plus.

Do Chase Business Cards Count?

This is a confusing one. When applying for a Chase Business card, the 5/24 rule is absolutely in effect. This means that if your credit report shows that you’ve opened 5 or more cards in the past 24 months, Chase won’t approve your new business card application. That said, if you do get approved for a Chase business card, it won’t count toward your limit. For example, if your current count is 4/24 and you successfully sign up for a new Chase Ink Business card, your count will remain at 4/24 because Chase won’t report this card to the credit bureaus.

Do Store Cards Count?

Store cards count towards 5/24 only if they can be used elsewhere (e.g., when they are Visa, Mastercard, or Amex cards).

What if Chase Denies Your Application?

If you are denied for a new Chase card and believe you are under 5/24 (or if authorized user cards put you over 5/24), I strongly recommend calling Chase’s reconsideration line at 1-888-270-2127. Ask them to reconsider your application.

If the reason for denial is being over 5/24 due to authorized user cards on your credit report, tell the agent that those are authorized user cards and you are not responsible for paying those bills.

If you are denied for any other reason and have other Chase cards open, tell the agent that you are not seeking additional credit. Ask them if they can move credit from some existing cards to the new card. Note that they can move credit from personal cards to other personal cards, or from business cards to other business cards, but they can’t span the two (e.g., they can’t move credit from your personal cards in order to open a new business card).

Why Does 5/24 Matter?

The easiest way to accumulate huge numbers of points is through credit card welcome bonuses, and Chase has many of the best cards and welcome bonuses in the U.S. market. If you want to take advantage of any of these, you’ll usually have to be under 5/24 to get approved.

For example, Chase has a fantastic lineup of cards that earn Ultimate Rewards points. Through these cards, one can easily amass hundreds of thousands of transferable points through signup bonuses, and then continue to earn huge rewards by picking the right cards for the right type of spend (for example, pay your phone, cable, and internet bills with your no-fee Ink Business Cash card to get 5X rewards for these purchases on up to $25,000 of spend per cardmember year). You can read more here: Chase Ultimate Rewards Deep Dive.

Another key component of Chase’s credit card dominance is its issuance of Southwest Airlines credit cards. This is huge because Southwest has the best deal in travel: if you earn enough qualifying points in a calendar year, you’ll get a companion pass good for an unlimited number of flights booked with points or cash. That companion pass is good for the rest of the year in which it is earned and all of the next year. And, with Chase, it’s often possible to get that companion pass simply by signing up for a personal Southwest card and a business Southwest card and meeting the minimum spend requirements for both. See our Southwest Companion Pass Complete Guide for details.

Chase also has some terrific hotel credit cards. If you want to earn top-tier Hyatt status (which is, by far, in my opinion, the best top-tier hotel status), you can earn that status through spend with the World of Hyatt card. Similarly, you can earn top-tier IHG status with spend on either the IHG Premier Card or IHG Premier Business Card.

")

The new accounts under the capital one transunion report only show new accounts opened in the past 12 months, not 24. I think the post needs to be updated.

Can you update this post? #3 (CreditKarma) no longer matches with what’s posted.

Thanks

I don’t see that my Mesa card shows up on my 5/24 count FYI, via CreditWise/Transunion or Credit Karma

Experian no longer works, no Accounts tab, cannot move further. What is next easiest method? CreditWise?

Experian now requires to “connect” all my accts in order to sort by date.

No way I am giving these clowns all of my banking information/log on’s/etc

Experian app method is gone.

Experian forced me to Upgrade the app and there is no ‘views’ option to sort it by date opened. It defaults to Company name and thats it. Cant change it

No longer works with Experian

Has the Chase Sapphire Reserve popup notice spread to their other cards?

How does the bonus calculation works for 24 months and 48 months. Does it count from card open date or the actual bonus received date?

Can also do this on CapOne via their Creditwise. Takes a few clicks, not entirely intuitive but it’s there

Agree, this remains the best method once you once learn how to navigate the website. The portal literally tells your 5/24 status. It is way easier than the methods mentioned in this article but I understand not everyone may have an account with capital one.

Care to share with the class?

Love it. Try: Home–> “your transunion credit report”–> this brings you to ‘accounts and balances’ and under that on the left side is an icon that looks like a document (under which mine says “8 new”)–>I click on the ‘8 new’ and that takes me to ‘new accounts’. it lists all accounts that are open within the last 2 years, most recent being first. You will have to discern which are your business v personal cards. Clicking on each card name will have various info, most notably ‘age of account’. There is also a payment history which also give you a less specific age, but may be helpful also.

Good stuff. Thanks for sharing.

THANK YOU!

Good call. I added it.

Thanks for that. Currently at 3/24 but will drop to 2/24 after June. I need a chase Marriott card for the 15 nights to keep Platinum. Already have the business card.

Keep us posted!

I no longer see the Views tab on Experian, when I click on Accounts. This used to work.

Experian Slide # 4- there is no longer a Views tab. The only words at the top are the names of the three credit bureaus…..

It’s there when I look at mine. Can you double-check now? Wondering if it was a temporary glitch.

Agree. The “views” link is no longer there

unfortunately, this article was not updated with the last information

You may be able to see a filter icon on the bottom right corner of the phone. The filter allows the sort by date opened.

no, no icon….it only sorts by bank name. This article needs to be updated.

It’s there now.

It’s there now when I look at mine.

It’s there when I look at mine. Can you double-check now? Wondering if it was a temporary glitch.

[…] Tip: Apply for Chase cards early, as 5/24 locks you out even with excellent credit [10]. […]

Excellent article. Thank you!

Admin’s knowledgeable replies to reader questions make Frequent Miler the best points and miles website.