When I posted last week about cards I’ve opened recently, one reader asked about my banking relationship with U.S. Bank (I have long had checking and savings accounts with U.S. Bank that I don’t use much, but those are no longer required for the Altitude Reserve card). In a different recent post about a Capital One Checking Account bonus, someone asked if having a Capital One 360 account would make it more likely to get approved for a Venture X card (I don’t know the answer, but my wife had long had a Capital One 360 account and did get approved for the Venture X). Now Dan’s Deals reports that application details on at least one type of credit card from another issuer indicate that having a checking account may increase the odds of approval.

Approval algorithms for credit cards are obviously very complicated and can rarely be boiled down to a single factor. I often remind people of this when they cite being denied for “too many inquiries” (those denial letters cite something, but it is probably almost never the leading reason and sometimes isn’t even a sensical reason).

However, we do know that some issuers seem to value having a larger banking relationship. For instance, Bank of America has been known to require some business credit card applicants to open a CD in order to get approved for a business card (my wife got such an offer a couple of years ago and declined to open the CD).

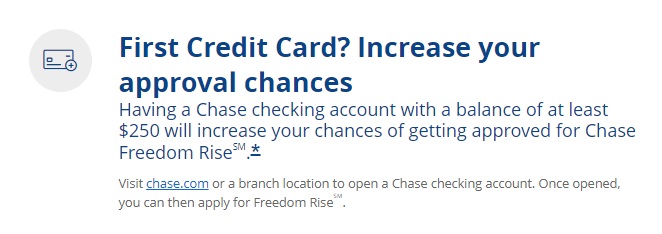

Dan’s Deals catches an interesting section found on the application page for the Chase Freedom Rise card (which looks like a similar card to the Chase Freedom Unlimited card that is probably designed for those who are building credit):

As you can see, the application page directly states that having a Chase checking account with a balance of at least $250 will increase your chances of getting approved for this card. Dan also points to anecdotal data points from readers that were declined and then subsequently approved for credit cards after opening a Chase checking account. That’s interesting as it certainly might open an avenue for those who have had difficulty getting approved. It is obviously impossible for anyone to predict approval, but Chase is explicitly saying that one’s odds are increased for this specific card when you have a checking account with more than $250 in it, so it isn’t unreasonable to think that it may be a factor considered in other applications.

On the flip side, in the past, I heard some data points of account shut downs that seemed to follow the opening of Chase checking accounts (for people who already had Chase cards and probably had a good deal of 5x office supply store spend).

Overall, I consider this interesting because it removes speculation as to whether or not it can increase approval odds. Obviously YMMV in terms of whether or not it helps you get approved, but it might not be a bad idea to consider a Chase checking account if you’re new to Chase and not getting approved for the cards you want.

")

I temporally have a Citigold level account & am trying to figure out how I can leverage that temporary status on the credit card side.

I think for most people a banking account will positively impact credit card approvals with that bank. The exception can be with big MS users as we’ve seen in the past, having a 2nd risk dept (credit and banking) that can have eyes on your account can result in losing both. We’ve seen where those who were getting away with credit cycling (bad idea) get caught out not by the credit card risk dept but by their banking one.

Not for Cap1. Few months ago, I was denied for the Venture, my only credit card denial ever. Though not an active user lately, I’ve had Cap1 360 accounts since it was ING pre-merger.

However, a recent pre-approval screening says I’m allegedly eligible for the Venture. I’ll apply in a few months.

I was denied twice by Cap 1 – once for the Venture and then for Venture X. I then applied for Spark Cash select (about 9 months after latest denial) and was instantly approved. Six months later, I applied for Venture and was instantly approved with $50k limit. All this while not having any checking accounts or any other relationship with Cap1.

OTTH, I was approved for BofA Alaska card a couple of year ago without any relationship with them. I canceled it last year (after 2nd year fee was charged). This year, I applied for Flying Blue card and they denied it. The letter said lack of other relationship with BofA as one of the reasons.

$50k??!!? Good golly… Congrats!

My minimally involved player 2 was approved for the Venture after my denial. P2 was/is on my Cap1 bank accounts, but no other Cap1 accounts. My denial might’ve been due to getting 2 new credit cards within 6 months before applying for the Venture. Now that several months had passed, maybe Cap1 will approve me, and I’ll also have a Venture.

I have been apprehensive about opening new checking accounts to increase my odds of getting credit cards. I have no plans to move my direct deposits or withdrawals from my normal checking account, so the new checking account would not give a lender an accurate picture of my income, spend, or the minimum I keep in the account. I am concerned that a low amount of activity could reduce the chances of approval.

I deposited money with the Wasamatteryou Bank, and they approved my credit line to consolidate debt at 45% daily. (They never sent me a 1099….)