NOTICE: This post references card features that have changed, expired, or are not currently available

In my recent post “The next best credit card perks that will be taken away,” I predicted the demise of the 3X charity category bonus on the US Banks FlexPerk Visa card. Reader Kumar then pointed out that 3X charity was already scheduled drop to 2X at the end of this year. He wrote:

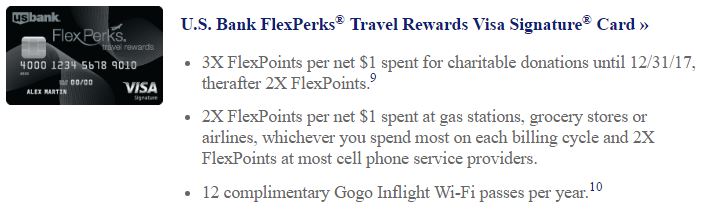

US Bank already announced the reduction in Charity category: 3X FlexPoints per net $1 spent for charitable donations until 12/31/17, therafter 2X FlexPoints

Goto usbank website, choose products and credit card. When you scroll down to Flexperks visa, you’ll see this information

And, he was right.

Specifically, the site says “3X FlexPoints per net $1 spent for charitable donations until 12/31/17, therafter 2X FlexPoints.9”

And footnote #9 says:

FlexPerks Travel Rewards Visa Signature Cardmembers will earn FlexPoints at a rate of three (3) FlexPoints per every $1 in eligible Net Purchases during each billing cycle for any merchant location that classifies itself as a Charitable and Social Service Organization (through 12/31/2017, then two (2) FlexPoints per every $1 thereafter). U.S Bank does not have the ability to control how a merchant chooses to classify their business and therefore reserves the right to determine which purchases qualify for additional FlexPoints. Bonus FlexPoints will be awarded within 60 days of donation.

I found similar text in the terms of for the business version of the card.

Does this effect existing cardholders too? No.. No.. Yes.

It’s obvious from the text on the card signup page that new customers will only get 2X points for charity after this year. What’s not clear is whether existing cardholders will also drop from 3X to 2X. I couldn’t find any documentation online that answered the question, so I called. Twice.

I have both the consumer and business version of the FlexPerks Visa card. I called the consumer customer service number first. The phone agent understood the question and immediately answered that the drop to 2X was for new customers only. I pressed her for additional information to see if existing cardholders would drop to 2X at some time later, but she didn’t have any more information. She said that if they were to change things for existing customers, we would receive an announcement about it.

I then called the business customer service line. Again, I asked if this 3X to 2X change is for all cardholders or just new cardholders. The agent put me on hold to research the question. When she returned, she had the same answer as the first agent. The change to 2X is for new customers only.

Then, last night I was at a US Bank promotional event for their new Altitude Reserve card and I had the chance to talk extensively with John Steward, president of Retail Payment Solutions (the same guy that Randy previously interviewed). I asked him about the FlexPerks change and he admitted that the change is coming to existing cardholders too. He said that we should receive notice within the next couple of months. While he didn’t tell me exactly when this would change for existing cardholders, I got the impression that we are also on an end of year schedule.

John Steward further told me that there was another change. They will (or maybe, already did?) expand the definition of charity so that more things will count (such as religious institutions, for example). Apparently they have had to deal with many support issues where customers thought they should have been getting extra points for spend that they thought of as charity. US Bank is hoping that by expanding the definition, even while reducing the category bonus, they’ll have more satisfied customers. I tried to find evidence of this expansion in the online terms, but all I could find was text that defined the charity bonus category as “any merchant location that classifies itself as a Charitable and Social Service Organization.” I’m not sure whether or not “Social Service Organization” is new.

What this means

It looks like 2017 will be the year for charitable giving! I plan to increase my Kiva loaning until the ball drops at the end of the year. After that, we’ll see. The FlexPerks card still has its uses, but 3X charity was the one thing that previously made it most attractive to me. For many, though, the card’s annual 12 Gogo Wifi passes alone could be enough to justify the card’s $49 annual fee.

Increased US Bank FlexPerks bonus: 26,667 points after meeting spend")

How can I check if my FP Visa still catagorizes Kiva as a charity? I made a ton of Kiva loans last month, but they don’t appear to be included on my latest FP Visa statement as charities. Has anyone else had a similar problem? The transaction descriptions are “Paypal/Kiva.”

Unfortunately US Bank had stopped coding Kiva as a charity over the summer: https://frequentmiler.com/2017/07/29/flexperks-kills-kiva-3x/

Is there any benefit to keeping the Flexperks cards anymore apart from the Gogo benefit?

Not for most of us. Some people like getting 2X for grocery spend (that’s all they use the card for). I plan to product change to the no-fee version.

[…] January 1, 2018, the US Bank FlexPerks Visa will no longer offer 3X for charity. Instead, the card will offer 2X. Since Kiva loans code as charity, this has been a great way […]

[…] Update: This perk is already scheduled to drop to 2X by the end of 2017. […]

[…] Hat tip to Frequent Miler […]

[…] FlexPerks kills 3x charity for 2018 and beyond. […]

[…] US Bank Flexperks is ending triple points on charitable donations […]

Another big change on the horizon: The Trump tax proposal doubles the standard deduction, and eliminates deductions for state and local taxes. De facto this means most of us would no longer get a tax benefit for charitable deductions, which is a far bigger loss than the Flexperks 3x. If this change takes effect at the start of 2018, another big reason to “bunch” charitable deductions in 2017. (At this point there’s no way of knowing what will actually happen, but we should know before the end of the year.)

Very good point. This doesn’t affect those of us who get 3X making kiva loans (since those are not considered charitable contributions by the IRS), but for actual donations it’s an important consideration.

Every decent exploit that you post about is quickly killed by whoever owns it. It’s hardly a coincidence. They read your blog specifically looking for ways to control abuse. This is no secret. Exposure here directly results in killing deals.

Why all the shock?

I suspect that the re-wording means that spending at, for example, Thrift Stores run by charitable organizations (ARC, Goodwill, Churches, etc) will qualify as charitable as they are supposed to be “non-profit” to benefit others.

Very unfortunate. I had Justin streamlined my FlexPerks 3x MS method, guess I’ll only have 6+ months of it.

*just, not Justin, haha.

And here I was about to reach out to Justin for advice 🙂

Noooooooooooo!!!!!!!!!!!!!!!

What card do you think is best for charitable giving after this happens?

I still think that the flexperks Visa is best but no longer by a wide margin compared to best cards for everyday spend:

https://frequentmiler.com/best-rewards-for-everyday-spend/