NOTICE: This post references card features that have changed, expired, or are not currently available

If it seems too good to be true… You know the rest. The funny thing about the credit card signup game, though, is that many deals are as good as they seem. Those 50,000 or even 100,000 point offers really are worth a huge amount of travel. The trick is that you have to get approved and then meet minimum spend requirements in order to get the bonus. Plus, you need to pay your card balance in full each month in order to avoid huge interest rate fees. And you have to learn how to get the most from whatever rewards you’ve earned. So, it takes some work, but for most of us it is a no-brainer — it is definitely worth the trouble.

Now Zerocard has come along and has promised up to 3% cash back on all spend. Not only does that sound too good to be true, but the name itself sounds like a joke. How much cash back will you really get with Zerocard? Zero?

Background

Zerocard is technically a credit card that in some ways acts like a debit card. In order to make a purchase, you must have enough money banked with Zero first. At first glance, Zerocard appears to offer best of both worlds between credit cards and debit cards:

- Like a debit card (without overdraft protection), you won’t be able to accidentally spend more than you have.

- Like a debit card, you can’t end up with interest or late payment fees.

- Like a rewards credit card, you’ll earn valuable rewards for your spend.

- It is possible to earn up to 3% cash back, which would make this the single highest earning cash back card on the market.

Here’s some more info from the Zerocard FAQ:

- Deposited funds will be insured up to $250,000 by an FDIC-member partner bank.

- Cash back will only apply to card purchases. If you don’t use the physical card or card number to purchase something from a merchant, your transaction won’t receive cash back.

- Interest on deposits – In addition to cash back earned on Zerocard spending, you will earn interest on deposits made to Zero at a higher rate than leading savings accounts.

- ATM Use – Zero gives customers the ability to use the card with no ATM fees at more than 50,000 locations via a partnership with a national, non-bank affiliated ATM network.

- Zero will pay rewards at the end of every month.

- Zero will begin accepting applications in early 2017.

- Zerocard is designed for personal and household use. “We use automated techniques to identify and flag patterns inconsistent with personal use and reserve the right to close accounts in such cases.”

Note that you can’t use the card as a debit card (to buy money orders, for example). Even though the card is somewhat like a debit card, it will act like a credit card for making purchases.

When will Zerocard really be available?

I have no idea. Yes the FAQ says that they’ll begin accepting applications in early 2017, but I won’t be surprised if it takes them much longer than expected to roll out the card.

The anti-ms clause

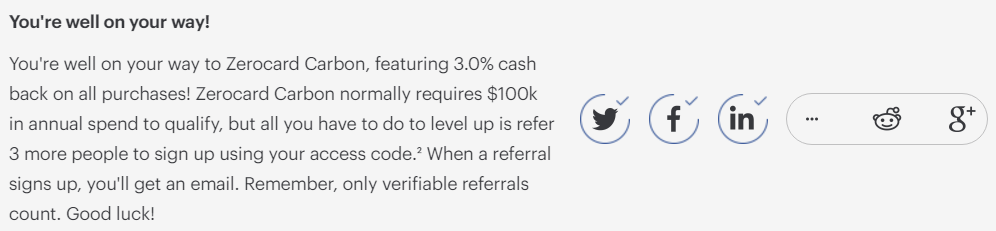

If Zerocard fulfills all of its promises, it will be easy to get 3% cash back in the short term, but long term will be tricky. In the long term, 3% cash back rewards requires $100,000 in annual spend.

Some of my readers may think that $100K spend could be easily met by manufacturing spend. That may be true, but please note this statement found in the Zerocard FAQ:

Zerocard is designed for personal and household use. We use automated techniques to identify and flag patterns inconsistent with personal use and reserve the right to close accounts in such cases.

Even though the above statement was designed to answer the question of whether one could use the card for business purposes or to spend “millions per year”, it seems crystal clear to me. If you MS heavily, you will get shut down.

How to play the 3% game

I’m not saying here that you should get the card, but if you do, here’s a way to get to 3% and potentially stay there long term…

Short term

Short term, simply sign up for the waiting list with someone’s referral link (here’s mine), and then click to share your own referral link on Facebook, Twitter, and LinkedIn. Just by clicking to share on 3 of these networks, you’ll get to the 2% cash back Magnesium level (you don’t even have to actually post to those networks — just click to open the pop-up share box). Then, get 3 friends to sign up for the waiting list with your link and you’ll move up to the 3% cash back Carbon level.

The Zerocard FAQ has this to say about leveling up through referrals:

The Zerocard FAQ has this to say about leveling up through referrals:

Please note that this referral program is being offered for a limited time, and will not be available once we launch the Zero experience and products to the general public (“Official Launch Date”). Registrations must be received at or before 11:59 p.m. PST on the calendar day immediately preceding Zero’s Official Launch Date. People who level up via waiting list referrals unlock the ability to initially receive a higher level card (i.e. Zerocard Carbon) and will maintain it for the remainder of the calendar year in which they become a customer, plus all of the following calendar year.

The key take-aways:

- Do this sooner rather than later (all it takes is your email address, so there’s no real risk)

- When you level up through referrals, you’ll get the higher level rate for the remainder of the calendar year in which you become a customer plus all of the following calendar year.

Long term

Assuming you get to the 3% level through referrals and you get your card in 2017, then you should be good to go at 3% cash back for the rest of 2017 and all of 2018. To keep your 3% cash back rate past 2018, you’ll want to spend $100K or more in 2018. If I understand this correctly, the amount you spend in 2017 shouldn’t matter at all.

The question is, how can you spend $100K without triggering a shutdown? I’m just guessing here, but I think that the following would help:

- Use the card for all of your everyday spend.

- Spread big charges over time, if possible.

- Use a service like Plastiq to pay bills that can’t normally be paid by credit card (rent, mortgage, professional services, etc.). Plastiq charges a 2.5% fee which would be well worth paying if it helps keep your Zerocard cash back at 3%.

- Avoid manufactured spend techniques, such as buying gift cards in large amounts.

Is the Zerocard game worth playing?

If Zero Financial fulfills their promises, then the game seems worth playing in the short term. That is, it’s worth signing up for the waiting list and referring a few friends so that you’ll start at 3% cash back if you get the card. Depending upon when they launch, that may give you close to 2 years of 3% cash back. Not bad. If you put $30,000 per year on the ZeroCard rather than a 2% cash back credit card, you’ll come out ahead by $300 per year. Overall it would be similar to signing up for the Discover It Miles card which effectively offers 3% cash back in your first year of card membership, but ZeroCard may offer close to two years at that rate.

Long term, I think that the Zerocard only makes sense for those who value its debit-card-like features, or for those who spend just a bit over $100,000 per year for personal and household stuff. Those who spend a lot more than $100,000 per year will probably get shutdown.

[…] been here before with a too-good-to-be-true fee-free 3% everywhere startup credit card. Remember Zerocard which was just a few months from release in late 2016? They finally launched the card two years later (November, 2018). Then, in March 2020, they shut […]

[…] In 2016 I wrote about this hybrid debit/credit card named Zerocard from a company named Zero. “Zero” refers to the card’s lack of fees. Zero says that it’s possible to earn up to 3% cash back for all purchases. So, I responded with : How to play the Zerocard game. […]

Use my referral link.

https://zerofinancial.com/ZERO4044

Here’s my link as well – https://zerofinancial.com/EARLY2084

Thanks

Or you could just get a Marukai JCB card: https://www.jcbusa.com/for_consumers/marukai-premium-jcb-card/

It’s 3% after $3,000 in spend and has a $15 annual fee. You can’t get it in every state, but I imagine that’s less of a burden than coming up with 100k in spend.

My referral link here: https://zerofinancial.com/REWARD3945

Please comment if you use it so I can thank you personally!

I expect that this will all end in tears.

Hi Greg, does Zerocard count as a new account toward the Chase 5/24 rule?

Probably. It will depend how they report the card to the credit bureaus

Here’s my referral link (you start at the 1.5% rate): https://zerofinancial.com/REWARD3828

Please use mine. Thank you! https://zerofinancial.com/EARLY22989

For anyone willing,

Please use my referral link:

https://zerofinancial.com/SECURE3787

Here is mine:

https://zerofinancial.com/EARLY5012

Please use my referral link!

https://zerofinancial.com/CASH3711

There seems to be a bug in the system right now.

I just did a test signup and was leveled up to 1.5% after clicking to share on two social networks, but even after clicking to share on all the others, I didn’t get to 2%. However, the screen suggests that I should have moved up to 2%:

“Ready for even more?

Getting Zerocard Magnesium, featuring 2.0% cash back on all purchases, normally requires $50k in annual spend to qualify, but all you have to do to level up is share a special access code on social media.”

Greg, Is it OK to post my referral link here?

Yes. If you put it in the form of a URL it may be caught by the Spam filter though. I’ll try to find those and fix them when that happens, but I can’t guarantee it.