Some of the best ultra-premium credit cards come with trip cancellation insurance coverage. Like any kind of insurance, it is difficult to measure the quality of trip cancelation coverage until you have cause to use it. A couple of months ago, we had to cancel a trip at the last minute because one of our kids got sick. We filed a trip cancellation claim with the Card Benefit Services claim administrator, and I’m glad to report that the process was easy and the claim was approved. This post covers how we made a claim, what was required, and the positive outcome.

Chase Ritz-Carlton Visa Infinite trip cancellation insurance coverage (which matches the coverage on the Chase Sapphire Reserve)

The Chase Sapphire Reserve has what is widely considered to be the best ultra-premium credit card travel protections of any currently available card on the market (you can find more detailed comparisons of ultra-premium credit card travel protections here). The Chase Ritz-Carlton Visa Infinite Card, which is no longer available to new applicants, but which can still be acquired via product change from another consumer Chase Marriott card, has matching travel protections. Either card can be a great choice for travel protections like trip delay coverage, lost or delayed baggage insurance, emergency medical coverage, and trip cancelation coverage.

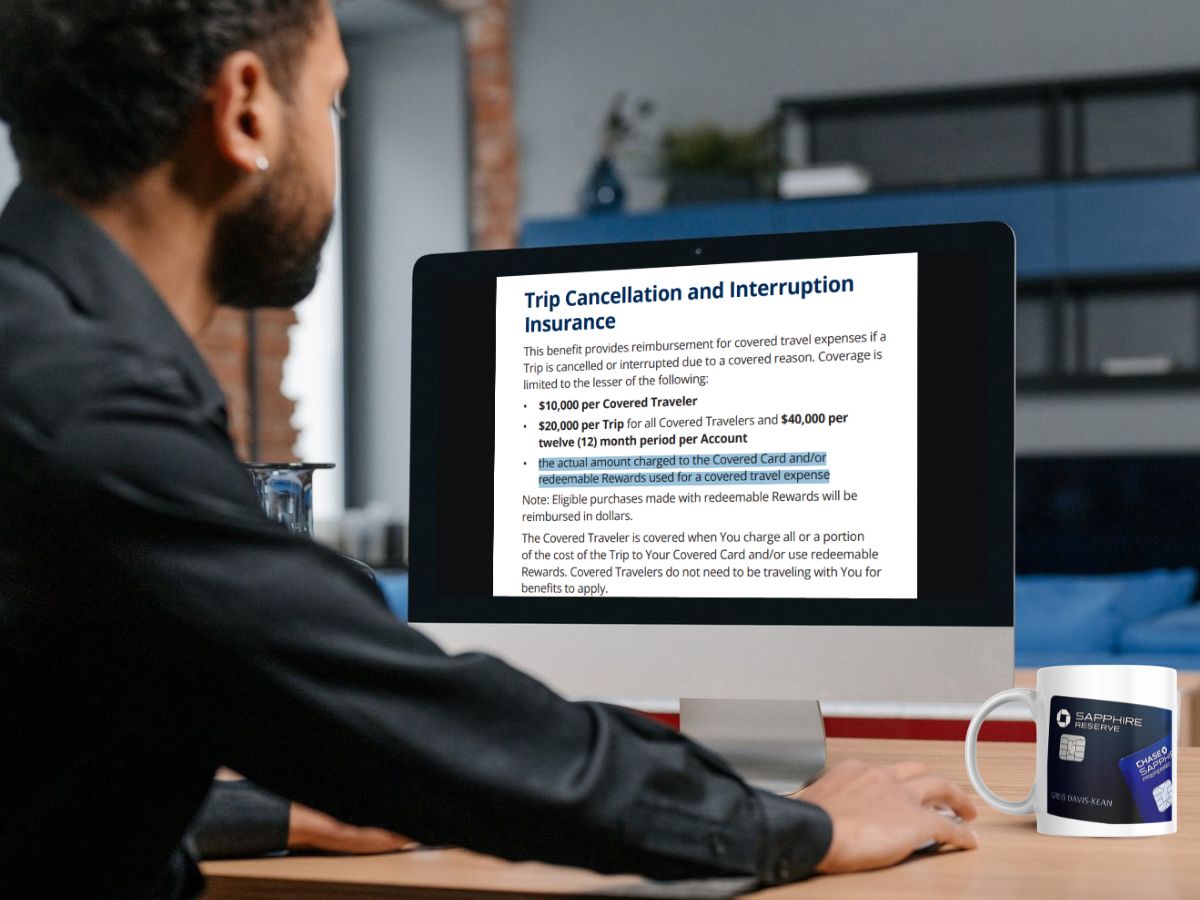

I recently had experience with trip cancellation coverage. This is the summary of the trip cancellation benefit from the Chase Ritz Carlton Visa Infinite Guide to Benefits that outlines the basics of the coverage, including maximum amounts and which parties are covered:

The Trip Cancellation and Trip Interruption benefit provides

reimbursement for Eligible Travel Expenses charged to the

Cardholder’s Account up to ten thousand ($10,000.00) dollars

per Covered Person and up to twenty thousand ($20,000.00)

dollars per Trip, if a loss results in cancellation or interruption of the

travel arrangements.

The Cardholder and Immediate Family Members are covered when

the Cardholder’s name is embossed on an eligible Card issued in

the United States, and the Cardholder charges all or a portion of

a Trip to his or her Credit Card Account and/or Rewards programs

associated with the Account. Immediate Family Member means an

individual with any of the following relationships to the Cardholder:

Spouse, and parents thereof; sons and daughters, including adopted

children and stepchildren; parents, including stepparents; brothers

and sisters; grandparents and grandchildren; aunts or uncles; nieces

or nephews; and Domestic Partner and parents thereof, including

Domestic Partners or Spouses of any individual of this definition.

Immediate Family Member also includes legal guardians or wards.

Immediate Family Members do not need to be traveling with the

Cardholder for benefits to apply.

Eligible travel expenses covered are non-refundable prepaid travel expenses (and can include redeposit fees imposed by a Rewards program). Note that things like event tickets or prepaid fees to theme parks, museums, and other points of interest are excluded unless they are part of a travel package.

The guide to benefits suggests that a broad array of situations is covered. Specific examples included in the guide that were applicable in our circumstances included the following bullet points (bold is mine for emphasis):

• Accidental Bodily Injury, Loss of Life, or Sickness experienced by You

or Your Traveling Companion which prevents You or Your Traveling

Companion from traveling on the Trip

• Accidental Bodily Injury, Loss of Life, or Sickness experienced by an

Immediate Family Member of You or Your Traveling Companion when

the Accidental Bodily Injury or Sickness is considered life threatening,

requires hospitalization, or such Immediate Family Member requires

care by You or Your Traveling Companion

In our case, one of our sons got sick in the days leading up to our departure date. Since a sickness experienced by a traveling companion is covered, as is a sickness by an immediate family member that requires your care, we expected to be covered under trip cancellation insurance.

We had to cancel a trip on Allegiant at the last minute due to illness

A couple of months ago, just a few days before our local school went on a week-long February break, we decided that we were going to spend that break period visiting family in Myrtle Beach, South Carolina. Allegiant Airways has a nonstop route from our local airport of Albany, NY (ALB) to Myrtle Beach, SC (MYR). Ordinarily, we are very hesitant to book with a low-cost carrier like Allegiant because of the relative infrequency of their service. However, since it was by far the most reasonably priced option at the time when we booked, we decided to book the Allegiant flight just a few days before travel. We paid a little over $300 total per passenger for the flight, seat selection, and baggage fees (we had both checked and carry-on luggage).

My wife and I both have Ritz-Carlton credit cards, and the Ritz-Carlton credit card comes with $300 in annual airline incidental credits. Since we were paying for incidentals like seat selection, carry-on, and checked baggage, we split up the booking. I purchased the airfare for myself and one of our sons on my Chase Ritz-Carlton Visa Infinite card. My wife purchased airfare for herself and our other son on her own Ritz card. We anticipated that we would each file separately for incidental credits to cover those ancillary fees.

In the end, we were glad to have used our Ritz cards because of the travel protections they provide.

Unfortunately, just over 24 hours after purchasing airfare, one of our sons woke up in the middle of the night vomiting, and he proceeded to spend the next couple of days under the weather. On the day we were due to take off, we brought him to our local health center for a professional evaluation and advice.

In short, the doctor recommended against travel until he was symptom-free (no surprise to us). We made sure to get that documented from the doctor’s office on official letterhead.

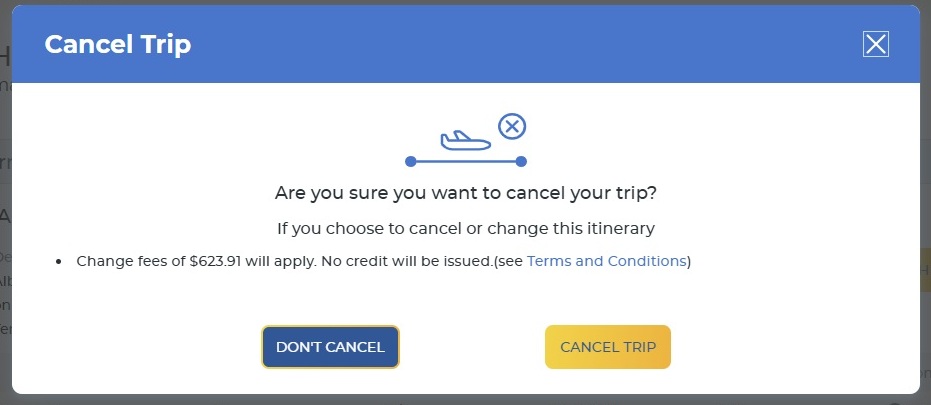

Next, I canceled our flights. During the cancelation process, I made sure to take a screenshot of the Allegiant website showing that the airfare was nonrefundable and that we wouldn’t receive any flight credit for the cancelation.

Note that the guide to benefits suggests that your benefit will be decreased by the value of any merchant credit you receive (such as a future flight credit) until such credit expires:

• In the event that Your Trip Cancellation or Trip Interruption results

in a credit for future travel, accommodations, or other consideration

being issued by the Travel Supplier, no benefits shall be payable

for that portion of the Eligible Travel Expenses which such credit

represents until such credit expires.

I interpret that to mean that if Allegiant had provided a flight credit, we would not have been eligible for a credit from this coverage until after the credit expired (though this does suggest to me that reimbursement may be possible after the credit expires; your mileage may vary).

Filing a Chase trip cancellation insurance claim

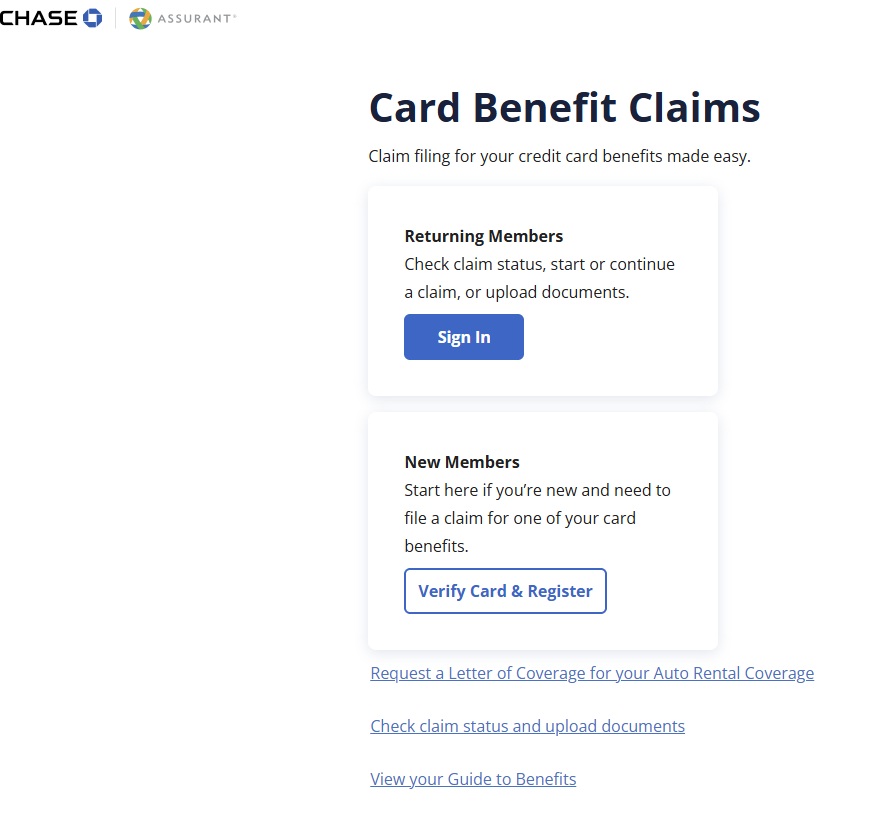

The process of filing the claim was very simple and straightforward. After consulting with benefits in my online account, I went to https://www.chasecardbenefits.com/file-claim to start the process of filing a claim. If you already have an account with the card benefits administrator, you can sign in. Otherwise, you have to verify your card and register for an account (this is separate from your Chase login, as the benefit administrator is a separate company).

It is worth noting that I could have alternatively begun the claims process over the phone, but I was happy to file the claim entirely online since I knew I had all of the necessary screenshots and documentation. Personally, I would rather have everything in writing than handle the process over the phone anyway, lest I mispeak in some way or misunderstand a piece of critical information.

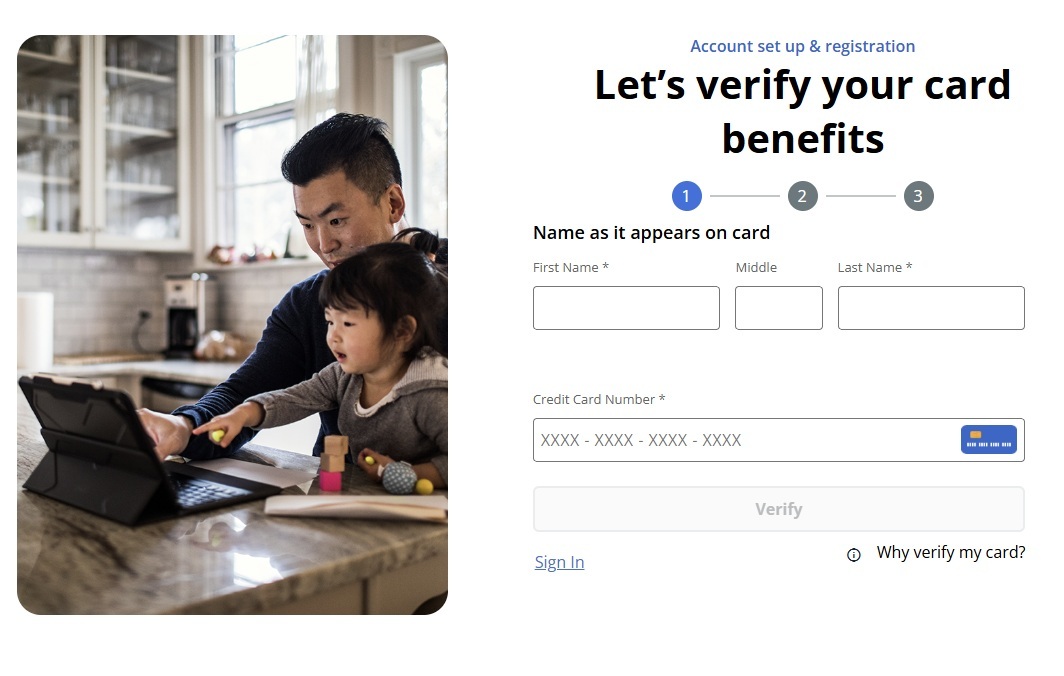

Registering for an account is easy. You just need to enter your name and card information to confirm eligibility.

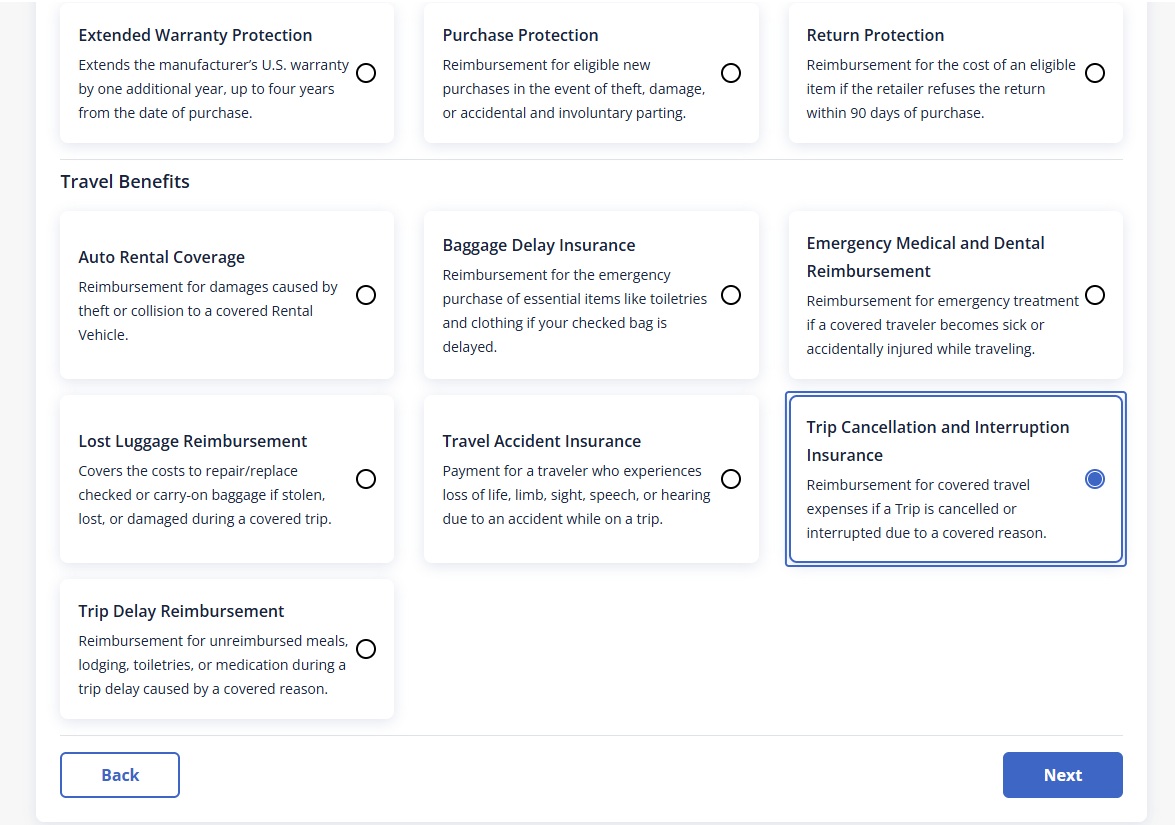

Next, you click a button to file a claim and choose the type of claim.

From there, I had to enter basic information like the date of purchase, cost charged to the card, and date of cancellation. I also had to provide documentation. The system requested all of the following information:

- Confirmation of the reason for the trip’s cancellation or interruption

- Confirmation of Travel Arrangements cancellation

- Covered Travel Expenses

- Travel Itinerary

- Unused vouchers, tickets, or coupons (if any were received)

- Monthly billing statement showing the purchase amount

- Other claims settlement details (like a settlement from other insurance you may have)

In order to meet those requirements, I uploaded the following:

- A photo of the letter from my son’s health center office visit recommending against travel until symptoms subside

- A PDF of the email Allegiant sent confirming cancellation of the itinerary, as well as the screenshot above (at a wider view) showing the fact that no refund or credit would be received

- A PDF of my original email confirmation from the date of booking, which included my travel itinerary and the cost of the trip (along with the last four digits of the card used to pay)

- A PDF of my monthly billing statement showing the purchase

I had also taken a screenshot of the page on Allegiant’s website explaining its cancellation policy, but I ultimately didn’t need that.

Request for follow-up information and trip cancellation insurance approval

Within a day of filing my claim, I received a request for additional information from the Claims Adjuster. Oddly, they requested that I upload a copy of the itinerary for the Trip. I had already done that, so I uploaded the same document again, along with a letter written in a Word document explaining that I had already uploaded this information and was uploading the itinerary once again, explaining where to find the date and time and all of the necessary information in that attachment.

Somewhat frustratingly, I didn’t receive any additional follow-up response after that. Days passed without any additional communication confirming receipt of the requested information or following up with other specific questions.

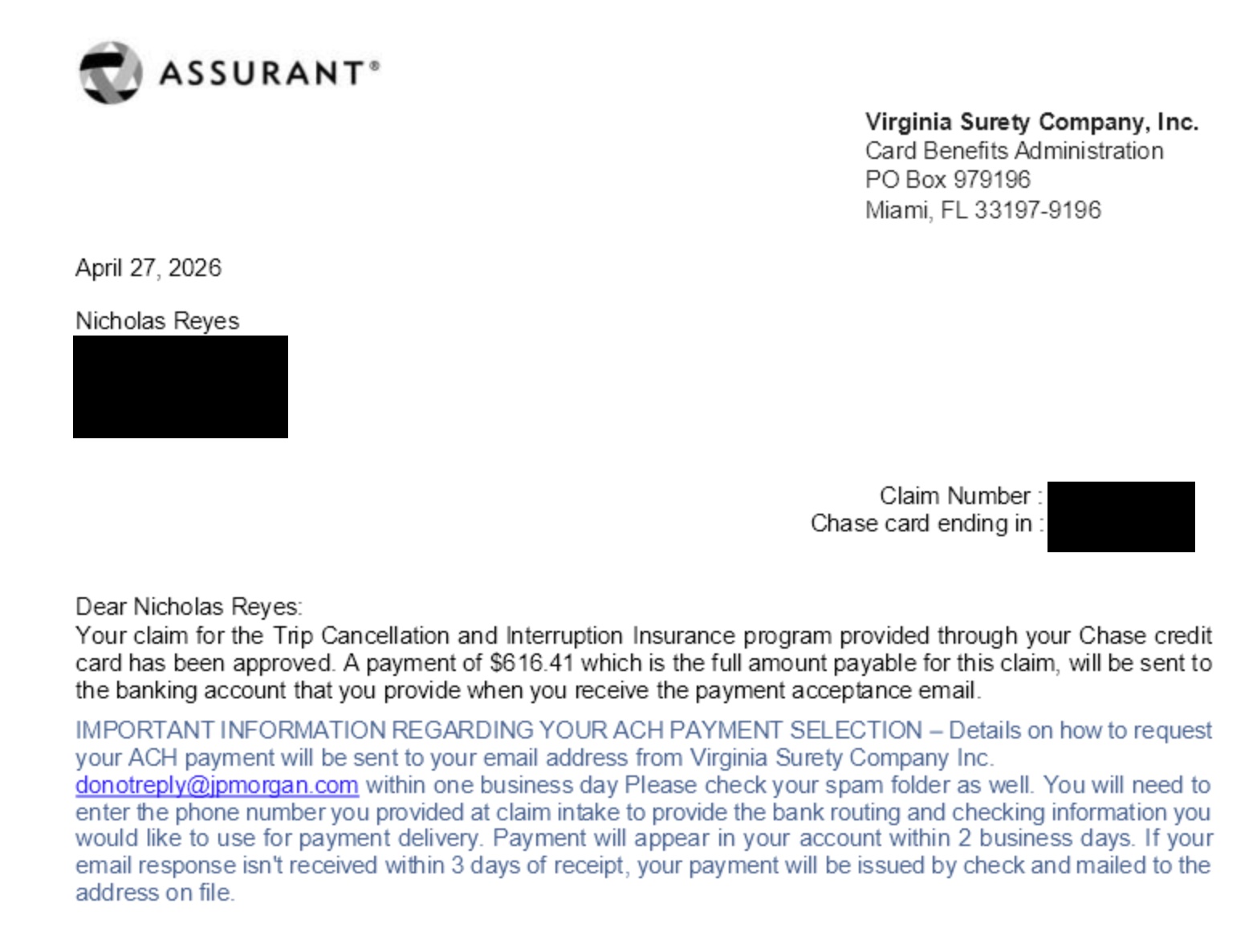

However, almost a week later, I received an email with an attachment indicating that my claim had been approved.

That was great news. Eagle-eyed readers may notice that the payment due here is listed as $616.41 despite the cancellation screenshot above showing a flight cost of $623.91. That’s because I used $7.50 worth of Allegiant Allways Rewards points from a previous trip and only charged $616.41 to my Chase Ritz-Carlton card. The Chase benefit covers the cost charged to the card and the value of rewards redeemed from your eligible Chase account. Since my Allegiant points were not connected to Chase in any way, I did not try to claim reimbursement for those.

I received another email a day later from Virginia Surety Company Inc an Assurant company, that confirmed the payment amount and provided a link to enter my banking information to receive an ACH transfer for the payout.

My wife then proceeded to file a separate claim for cancellation as well. We expect that to be approved with the same timeline. The son who got sick was on my itinterary, but as she needed to help provide care for him, she should also be eligible for the same coverage.

Bottom line

My trip cancellation insurance claim was as smooth and simple as one would hope. The process of filing a claim was intuitive, the processing time was entirely reasonable, and the claim was ultimately approved. While that is the outcome I would have expected based on the coverage provided by my Chase Ritz-Carlton Visa Infinite card, it is nonetheless reassuring to put the benefit into practice and see that it does indeed work as advertised. That makes me far more confident to book with a Chase card in the future, knowing that the claims company stood by the benefit and paid out without undue hassle.

Do you know how this coverage and claims process compares to what’s provided by C1 Venture X?

Feels to me like an insurance scam by nikko beardedhomo