Gold and Platinum cards from American Express come with statement credit benefits for purchases at Resy restaurants. Thus far, after enrolling your qualifying card in the benefit, the only requirement in order to be able to earn the statement credit on a qualifying card is that you make payment at a restaurant listed on the Resy platform. However, effective August 1st, 2026, the Resy statement credit benefit will only apply at restaurants indicated as eligible for the Resy Credit at the time of purchase. It remains to be seen whether eligible restaurants will be negatively impacted and how often eligibility may change.

Update: An Amex rep indicates that Resy venues have not been removed. On the contrary, we are told to expect more eligible venues later this year, with a specific callout for Tock restaurants. Here is the statement we received:

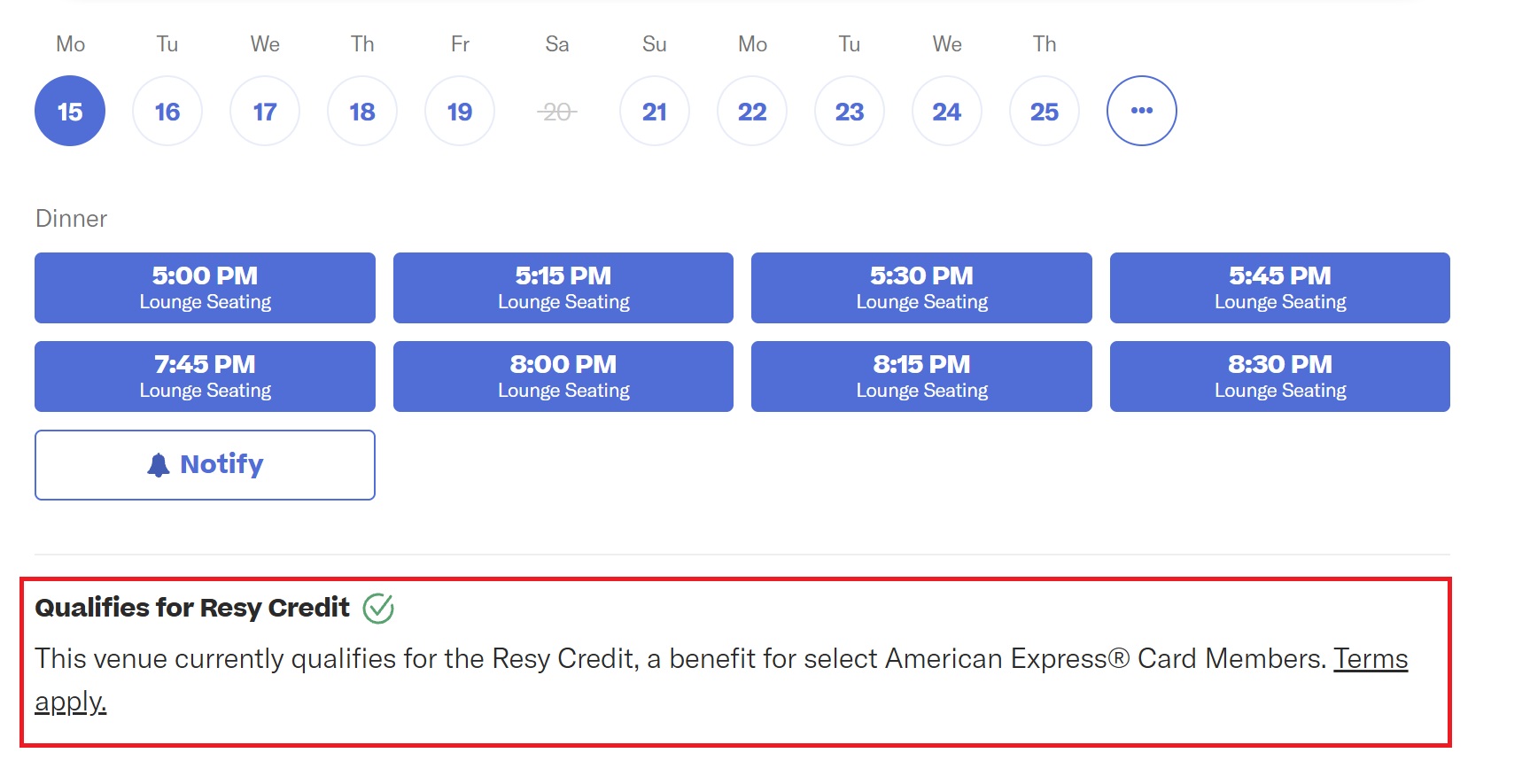

We have added a Resy Credit eligible badge to Resy venues pages to provide additional clarity to diners at the time of booking. We have not removed Resy venues that are eligible today and will be adding more eligible venues later this year when Tock venues become bookable on Resy.

That could be great news if Tock restaurants slowly become eligible for the Resy credit. We’ll see what happens in August, but at this point, we are cautiously optimistic that the changes here affect restaurants being newly added to the Resy platform rather than restaurants becoming ineligible for the credit. The rest of the original post follows.

The following message has appeared on Platinum and Gold card billing statements in recent days:

Effective August 1, 2026, U.S. restaurants and other food and beverage establishments (e.g., wineries, cafes) must be indicated as eligible for the Resy Credit on the Resy website or the Resy app at the time of purchase to qualify for the benefit. Qualifying restaurants and other food and beverage establishments will be indicated as eligible on their booking page on the Resy website or the Resy app and are subject to change at any time.

At the time of writing, all of the restaurants I’ve checked are showing up as eligible for the Resy benefit, which makes sense since this new restriction doesn’t take effect until August 1st, 2026. Beyond that date, it is unclear as to the effect this will have on restaurants eligible for the benefit.

Amex recently announced that it would fold the Tock dining platform into Resy this summer. Tock includes many top-rated restaurants like The French Laundry in Napa Valley and Alinea in Chicago, among many others. It is possible that Amex either does not intend for those former Tock residents to become eligible for the Resy benefit or that technical limitations mean that they may not all be folded into the system to enable the benefit from day one.

On the other hand, it’s certainly possible that Amex is making a change in how this benefit is administered, and restaurants may have the ability to choose whether or not they want to participate in the benefit. We don’t know whether that will be an all-or-nothing proposition or whether restaurants may be able to opt in on certain days of the week and not others. It just isn’t clear at this point.

The frustrating part to me is that it is possible that a cardholder will make a reservation at a restaurant that they see as eligible on the Resy website, but likely would not know if that restaurant had been removed from eligibility for the credit until after they don’t receive a statement credit. We’ve seen exactly that happen with the Chase Sapphire Reserve Tables benefit. As restaurants come and go from that platform from time to time, it really stinks that you have to double-check your restaurant on the day of your reservation to make sure it’s still eligible for the credit card benefit.

Beyond the inconvenience, I find it annoying that a restaurant can potentially take advantage of the ability to market to Gold and Platinum cardholders when they’re making their reservations, but not have to follow through on offering the credit when customers dine. I think that dining credits like these should either have eligibility renewed at predictable intervals, like a list being released every quarter, or that eligibility should be determined by the date the reservation was made rather than the date you dine (in other words, if a restaurant was listed as Resy-eligible when you made your reservation, the benefit should be honored after you dine).

Of course, that could quickly get messy because you don’t actually have to make a reservation through Resy in order to be eligible for the credit. Rather, you just need to use your card to make a purchase at the restaurant in order to earn the credit. I don’t know how they would determine which purchases should be eligible and which shouldn’t if they base it on when you made a reservation. I just don’t like the fact that restaurants can change without notice or notification; I would much rather just see American Express continue to offer the credit for all restaurants listed on the Resy platform. However, it is clear that they don’t intend to do that from August 1st onward.

We will have to keep a close eye on how that develops in August. I’ve personally been using Resy credits pretty quickly, so I will probably use my third-quarter credits between July 1st and August 1st, and thus I probably won’t have to worry about this until the fourth quarter of this year.

")

UPDATE: Amex buying The Fork, which accesses 50k restaurants in 11 European countries. Resy eligible potentially?

(Well, they already had the knife, since they’ve been dissecting these credits… expecting Resy to become a $5/week credit, soon.)

The Resy credit only applies to US restaurants. I don’t see that changing, personally.

The reasons for not keeping all kinds of credit cards keeps growing. Travel has been pretty much ruined, not particularly by these changes but by the masses of people desperate to use their credit card benefits. The entire process is just a slow-moving implosion, like The Idiot in charge.

Fish rots at the head…

Someone commented on another article on another site that Resy’s rapid expansion pulled in eating establishments that are more akin to cafes and the like as opposed to restaurants, Amex likely needs to separate the two for the intended use of the credit. I don’t have any worries about the restaurants my wife and I visit regularly. Everyone should take a deep breath.

I saw this happen with the CSR dining program, too. I’d booked a L.A. restaurant and two weeks later it was off the list. (I’m sure of this fact, as I only learned about the restaurant due to the published list.). Thanks for this update; now I’ll make it a habit to reconfirm. I just used the Amex Plat credit two days ago, and saw the notation that it was “eligible for RESY credit.). I love how quickly the credit is posted!

Oof, the CSR “Exclusive Tables” thing really should be called “elusive” tables. There’s always some fine-print in the terms where these programs basically say they can change anything, anytime they want, and you just have to ‘deal with it,’ or ‘kick rocks’ and ‘pound sand,’ but it doesn’t make me ‘like’ when they do that. Let’s hope Amex doesn’t nerf Resy too badly…

Speaking of Chase, I have it on the best of authorities, one author states that Chase is far too professional an organization to constantly change or flip-flop benefits (like it’s done over the past year with the CSR) . . . or accidentally post benefits on its website prior to being announced (like the recent DoC article notes).

But, if Bilt does any of the above, clearly Bilt is an unprofessional organization.

PS

THIS JUST IN – CHASE SENDS OUT EMAIL TO INK+ CARDHOLDERS EXCLUDING OFFICE SUPPLY STORES FROM 5X.

But, Chase is still a professional organization.

Who has been ignoring Chase’s screw ups? FM blasted them good for the CSR update, including getting Greg’s Bonyoyed of the Year award. Bilt has been blasted for their screw ups too, of which there have been many.

LOL.

Couponification – a growing trend. We all hate it. However, couponification is (somewhat literally) a house of cards.

Benefits of holding certain cards have, in the past, been much easier to understand. Increasing the number of “coupons” makes it harder to realistically understand value and increases the probability of breakage. That’s why the card issuers are doing it, and it seems like couponification is having its hey day.

But the imperfections are starting to show. OpenTables here, Resy there. I’m sure there are plenty of additional examples. As these imperfections begin to accumulate, it’s not unreasonable to expect consumers to figure out that value propositions might not be what they thought they were.

There is a breaking point when a consumer’s frustration exceeds the value they are getting or were expecting to get. When that happens, they’ll cancel their card. After this happens enough times to enough people, the card issuers start to lose consumer confidence. The growth of couponification is not stable for the long term. Will it all come tumbling down? Probably not, but it will likely grow beyond its sustainability then pull back a bit to something different that offers better stability. Whether that comes from shedding a few coupons here and there, or from stabilizing the existing ones that become problematic remains to be seen.

In my city with 11 Resy restaurants, 2 of them do not show the statement that the restaurant qualifies for the credit. Interestingly, one of the restaurants has a same-ownership, same-name “sister” restaurant; one of the two has the credit statement and the other doesn’t. Are these oversights or purposeful? I’m guessing it will be more clear after August 1.

If it doesn’t cost the restaurant anything when the credit is given to the customer, why wouldn’t every restaurant participate?

Do you know if this affects the Delta cards with monthly Resy credits?

Expect it.

I was a bit worried about the Resy expansion because currently most of the Resy restaurants are quite good (not all, but definitely most) and I understand Tock has this reputation as well but if they greatly expand past this it would be a lot less useful as a way to distinguish restaurants. It’s already the case that if a restaurant is not actively listed on Resy at the time of dining you won’t get the credit even if it was when you made the reservation. But if they keep adding restaurants and they’re not as well curated as current ones are, Resy’s value greatly diminishes. I hope they continue to curate the set eligible for the credit in a similar way; if not, it gets a lot less useful.

You want fewer restaurants eligible for the credit?

How exactly does having “worse” restaurants on the platform hurt anything?

It’s because Tock restaurants will show on Resy pretty soon, but rolling the benefit out to them will take a little bit.

Sure sounds like they intend to push the cost onto the restaurants, allowing them to decide whether they want to take a (potential) $100 haircut on the bill — or more than $100 for people who split the check onto two or more eligible cards. The net result will be many fewer restaurants taking the credit, and those will tend to be ones on their way out, not necessarily the places everyone wants to eat.

There’s no way that is how the credit works or will work. The restaurants are likely charged some sort of blanket marketing fee to be part of Resy and the credit must come out of that, directly administered by Amex. I doubt the restaurant has any clue who gets the credit or not – the fee is rebated to us directly from Amex. If it came from the restaurant on a case by case basis NO ONE would participate in the program.

I mean, that’s exactly how this kind of benefit operates for many existing card credits — or, at least, that’s how it’s reported. To the restaurants, Resy is, first and foremost, an off the shelf IT system for handling reservations, and secondly a marketing tool.

There’s no technical reason that the Resy credits couldn’t work the same way as, for instance, the Saks credit worked, implemented by Amex passing through the charged amount less the credit (or some proportion of the credit). When you say there’s no way that the credit will work that way, it sounds like you have some inside knowledge of how Amex interacts with “their” restaurants — is that the case, or are you just guessing?

I am definitely just guessing, but one difference with the Resy credit is that Amex is using it to expand the footprint of a service they own that has been losing market share recently. In addition to adding value to the Platinum and Gold cards to attract users, they also drive more people to Resy and offer an incentive for restaurants to join Resy to get some of the Amex credit traffic. So Amex wins several ways.

Resy is a reservations system that involves tens of thousands of separate businesses. Saks is a *single* corporation that Amex convinced to do this as a marketing campaign via Amex as a delivery mechanism. Saks can amortize the cost of the credits over all of their business, and decided to take a loss on credit card hackers. Individual restaurants are a completely different matter – these credits range from $10 to $100 and this level of variation would make restaurants have to swallow a highly variable and huge clumpy hit to their revenue stream. For example, imagine one person who has a lot of cards and went to their favorite restaurant and used Resy credits for every visit. That would clearly make the business hate that particular customer very quickly 🙂 The multitude of Resy credits only makes sense as an *Amex* marketing campaign which they are taking out of their overall *Resy* revenue stream and spreading out the loss for credits over their entire membership. This is a guess, but I think it’s very unlikely the program works the way the Saks campaign worked for these reasons.

I don’t begin to understand the financial arrangement here, but I had read that some restaurants that had already gone to OpenTable or considering it were taking another look at Resy because of the potential for traffic driven by the Amex credits. So I assume this is a way for Amex to increase the Resy footprint.

I have also seen theories that this is related to restaurants currently on Resy that don’t take Amex. However, I looked up the one restaurant that I know about that is on Resy and doesn’t accept Amex, and oddly it is listed as being eligible for the Amex credit.

There’s clearly an asymmetric power dynamic between the issuer (Amex), merchants, and card members, where, in most cases, we, the card members, come last, usually. *sigh*

I have a restaurant on RESY. Hopefully everything will stay the same. I have not received any info.

Do you mean you own the restaurant, or that you have one convenient to you?

Own. No new info has been given to us at this time.

Well then, you’re the man — a rock of actual information in a sea of us speculators! If you’re comfortable doing so, please feed any information you do get confidentially to the FM team.

James is the man!