NOTICE: This post references card features that have changed, expired, or are not currently available

Yesterday we reported that the Merrill+ Visa Signature Card 50K offer had resurfaced. I don’t know how long it will be available, but my guess is not very long at all. Should you hurry and sign up?

Signup for the signup bonus alone? Sure.

The card offers 50,000 points after $3K spend. That signup bonus can be used to get $500 in statement credits or up to two $500 flights. Either way it’s a good deal.

Use long term? Maybe not.

The Merrill+ card has no annual fee and earns only one point per dollar. For most uses, points are worth just 1 cent each. That makes this card a seemingly poor choice for everyone. But there are a couple of details that make the card interesting…

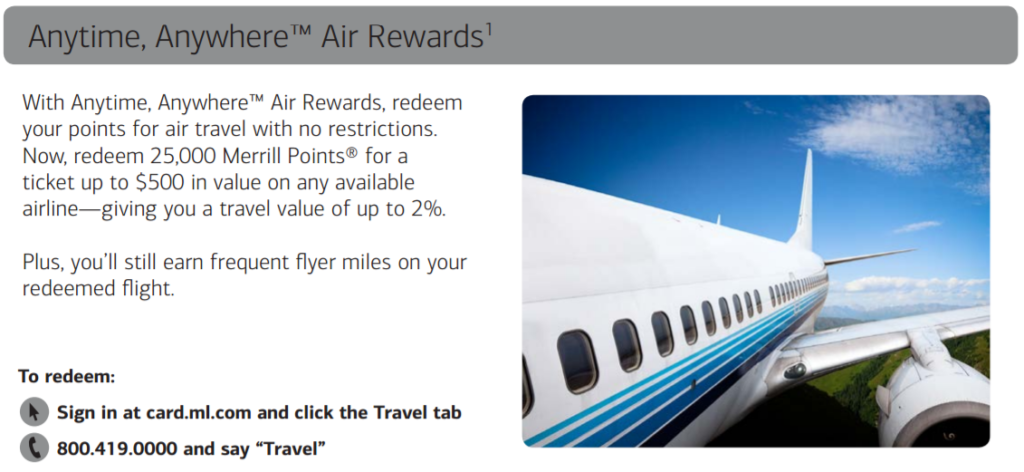

Up to 2 cents per point value towards flights

When redeeming points for flights, Merrill+ charges 25,000 points for any flight worth up to $500. If you purchase two tickets, they’ll charge 50,000 points. According to Doctor of Credit, If your ticket price is more than $500, Merrill+ will charge you 1 additional point for each penny above $500. That means that you can theoretically get 2 cents per point value by buying tickets worth exactly $500, but if you veer far from $500 in either direction, your point value will plummet.

When redeeming points for flights, Merrill+ charges 25,000 points for any flight worth up to $500. If you purchase two tickets, they’ll charge 50,000 points. According to Doctor of Credit, If your ticket price is more than $500, Merrill+ will charge you 1 additional point for each penny above $500. That means that you can theoretically get 2 cents per point value by buying tickets worth exactly $500, but if you veer far from $500 in either direction, your point value will plummet.

If you often buy $500 tickets, you can think of the card as earning 2% for all spend. That obviously sounds a lot better than 1%, but it’s still not even in the same league as a straight-up 2% cash back card. After all, unlike 2% cash back cards, with this one you would have to redeem points in 25K increments, and only for $500 flights, to get that value. And even if you do think it’s as good as a 2% cash back card, you can do much better with other cards (see Best Rewards for Everyday Spend, for examples).

So, obviously, the 50K offer is great, but once you’ve met the minimum spend requirements, there’s not much point in using the card anymore. Right? Well, consider one more thing…

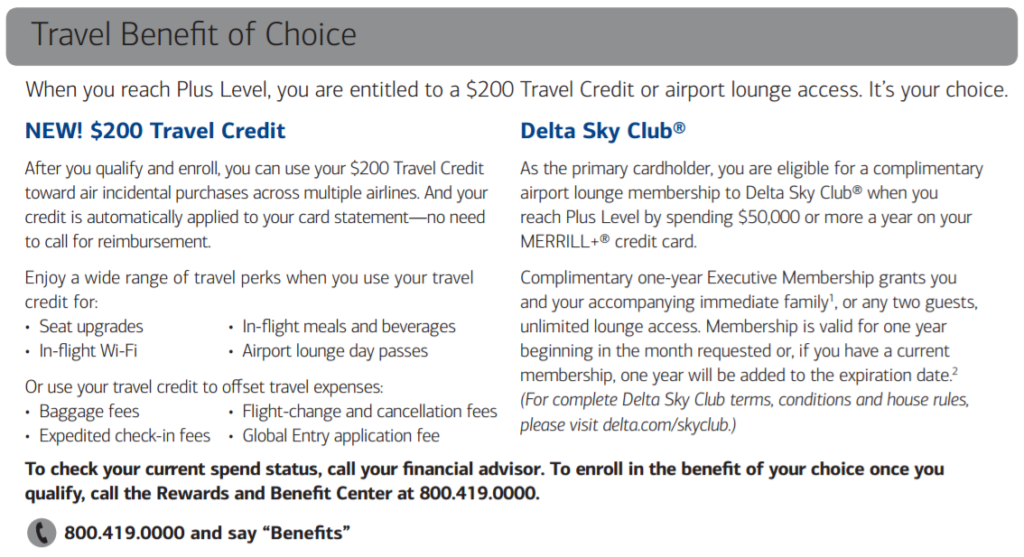

Plus Level Benefits after $50K Spend

After spending $50,000 within one calendar year, you can request one of two Plus Level benefits: $200 in travel credits or Delta Sky Club® Executive Membership.

$200 Travel Credits

I’ll just say it. It’s not worth spending $50K on this card just to get $200 in travel credits. Why not? Let’s assume that you spend exactly $50K and you optimize rewards by always redeeming points for $500 flights. In that case, $50,000 spend gets you two $500 flights plus $200 in travel credits. That’s a $1200 return. $1200 / $50K = 2.4%. That sounds good until you realize that there are several cards that earn more than 2.4% on all spend. Consider, for example, the Alliant Cashback Visa Signature Card. The Alliant card offers 2.5% cash back on all spend. If you spend $50,000 on the Alliant card, you’ll earn $1250 cash back. Subtract the $59 annual fee and you end up with $1191. That’s just $9 less than the rewards earned with the Merrill+ card and with no hoops involved at all.

Delta Sky Club® Executive Membership

Delta sells their Sky Club Executive Membership for $745 per year. The membership has a couple of significant advantages over Sky Club access granted by a credit card, such as the Amex Platinum card or the Delta Reserve card:

- Free Guests: With credit card access, guests are charged extra. With an Executive Membership, you can bring in immediate family or up to two guests for no additional charge.

- Access without flying Delta: With credit card access, you have to show proof that you are flying Delta on the same day. With club membership, you can enter anytime. This can be valuable for those who frequent airports with good Sky Clubs and often fly other carriers.

Is Executive membership really worth $745 per year? Probably not, but let’s do the math as if it was…

Let’s assume that you spend exactly $50K and you optimize rewards by always redeeming points for $500 flights. In that case, $50,000 spend gets you two $500 flights plus $745 worth of Sky Club membership. Let’s call that a $1,745 return. $1,745 / $50K = 3.49%. That’s excellent! If you truly value Sky Club membership at full price and you can be sure to redeem points for $500 flights, then this may be the card for you.

A better alternative

But… wait a minute. What if you have the Amex Everyday Preferred Card? This card offers 3x points at US supermarkets on up to $6,000 per year in purchases; 2x points at US gas stations; and a 50% bonus when you use the card 30 times or more per billing cycle. Let’s say that you make sure to use the card 30 times per month. In that case, you would earn at least 1.5 points per dollar for your spend, but often more. $50K spend would mean at least 75,000 points. And if $6K of that spend was at US supermarkets, you would be up to 93,000 points. And if $4K was at US gas stations, you’d be up to 99,000 points. Now let’s sprinkle in the Amex Business Platinum Card. This card gives you Delta Sky Club access when flying Delta. Plus, it gives you the ability to redeem points on your selected airline or in a premium cabin with any airline at a value of 2 cents per point. As a result, with the Business Platinum card, those 99,000 points are worth up to $1980 in flights. And, you get $200 per year in airline incidental fee reimbursements (which can be used for many things including paying for guests to enter the Sky Club). And you get Centurion Lounge and Priority Pass access for yourself and two guests without the need to be flying a particular airline.

The annual fees for the two cards are steep: $545 combined. But you can get significantly more travel value than with the Merrill+ card. Spending $50K on the Merrill+ card gets you up to $1000 in flights plus a Delta Sky Club membership. But the Amex duo gets you up to $1980 in flights, plus Centurion Lounge access, plus Priority Pass membership, plus Delta Sky Club access when flying Delta, plus $200 in reimbursements that can be used, among other things, to guest people into the Sky Club, plus rental car elite status, plus SPG and Marriott Gold elite status, plus Hilton Gold elite status, plus 10 Gogo internet passes per year, plus… You get the picture.

I’m sure the math would work out similarly for the Sapphire Reserve plus Freedom Unlimited duo, but I’ve already dragged this post on too long. See Super Credit Card Duos for more.

Summary

The Merrill+ Visa Signature Card’s 50K signup offer is excellent. It’s well worth getting if you can handle the $3K spend requirement. After that, though, I recommend sticking the card in a drawer. There are many better options for ongoing spend.

Southwest promo: Save up to 40% off base fares (& award flight) with promo code BUZZER")

Alaska Airlines sale: Save 30% with promo code SPRING30 (Book by 3/10)")

[…] As I reported before, this card is great for it’s signup bonus. The card also offers some perks with big spend, but I argued that you can do better with big spend on other cards. See: $1000 worth of airfare? Sure. $50K spend? Maybe not. […]

[…] applications at once, I decided to apply for three cards: Amtrak Guest Rewards World Mastercard, Merrill+ Rewards Visa Signature, and Alaska Airlines Visa Signature. I already had three Bank of America cards open at the time […]

Yesterday I called (866) 224-7803 immediately after applying online and got approved. I also moved credit line from couple of BoA credit cards

Does anyone have a phone number to speak with a person when checking an application status? It seems every number I call is automated and every person outside of the automation transfers me back to the automation…… Are all BOA cards this way?

I try to keep up-to-date numbers on our Best Offers page: https://frequentmiler.com/best-credit-card-sign-up-offers/#BOA

Currently it lists the same number that Kumar used: 866-224-7803

Does one get Delta Lounge access with any other AMEX Platinum card when flying Delta besides the Business Platinum?

Yes all Amex Platinum cards (except the Delta Platinum card) offer lounge access

In this world of credit card churn, a no fee card that gives a benefit is good to just get, use the benefit and stick in the drawer. It should help the age of your overall credit card profile, thus helping credit score. The only concern for me is the impact on me being able to get more Chase cards. I am way over 5/24, so this concern is small for me, but could be big for others.

A very useful analysis. Thanks