NOTICE: This post references card features that have changed, expired, or are not currently available

Update: While they were valid at the time of writing, some of the offers in this post have since expired. See our Best Offers page for current offer information.

Amex and Delta are offering fantastic welcome bonuses for their ultra-premium Delta Reserve cards. In the past it has frequently been possible to get 10,000 MQMs (Medallion Qualifying Miles) when applying up for the Delta Reserve card. As they did around this time last year, though, the Delta Reserve welcome bonuses currently (through 4/28/21) include 80,000 Skymiles plus 20,000 MQMs. MQMs are the primary currency you need to achieve Delta Medallion elite status. With the welcome bonus offers available at the time of this writing, getting meaningful Delta elite status is easy… if you don’t mind spending some cash.

The idea here is that you can earn near-top tier status without flying so that when you do fly, you’ll be able to enjoy the perks. Here’s what you need to know..

About Delta’s Platinum elite status

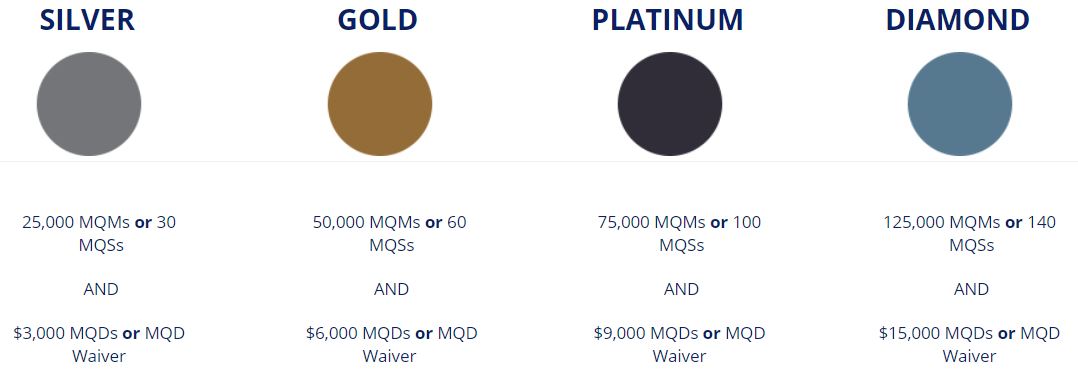

The image above shows the requirements for reaching each level of Delta elite status. Every level of status offers basic perks like free domestic upgrades (when available), premium seat selection, a free checked bag, etc. Higher levels of status make upgrades more and more likely. Also note the following details:

- $25,000 spend on any Delta Platinum or Delta Reserve cards within a calendar year will get you a MQD waiver which means that you don’t need to earn Medallion Qualifying Dollars (spend on Delta flights) to reach elite status up to Platinum status.

- Diamond Status requires $250,000 spend across one or more Delta cards in order to get a MQD Waiver. Due to that very high requirement, the rest of this post focuses on earning Platinum status instead.

Platinum status has several advantages over Gold status, including:

- Better chance of complementary first class upgrades. Free upgrades begin processing 5 days before departure (vs. 3 days prior for Gold members and 1 day for Silver).

- Upgrade to Comfort Plus immediately after booking.

- Choice Benefits: Pick one benefit each year such as 4 regional upgrade certificates (which are now more valuable than ever before) or 20,000 redeemable SkyMiles.

- Free award changes and redeposits. This last benefit is no longer as exciting as it used to be because Delta now allows free award changes and redeposits for all members on itineraries originating in North America. With Platinum status or higher, you continue to get that benefit for flights that originate outside of North America.

- Hertz President’s Circle elite status

Gold and Platinum elites also get waived same day change and standby fees.

Delta Reserve perks and status boosts

Delta Reserve credit cards come with several valuable perks such as Delta Sky Club® and Amex Centurion Lounge access when flying Delta, 2 Delta Sky Club one-time guest passes per year, upgrade priority over those with the same status and fare class, and annual domestic 1st class companion tickets.

Delta Reserve cards also offer Status Boosts: Earn 15,000 MQM bonuses when you complete $30K, $60K, $90K, and $120K spend within a calendar year. With one card, you can earn up to 60,000 MQMs through spend alone. With two cards (consumer and business), you can earn up to 120,000 MQMs through spend alone.

Read our in-depth analysis of the Delta Reserve cards here: Delta Reserve Complete Guide.

Plan Overview

The idea here is that it’s possible to earn near top level Delta elite status with a combination of MQMs from the welcome bonus plus big spend on the Delta Reserve card:

- Apply for Delta Reserve card in order to earn 20,000 MQMs and 80,000 bonus miles

- Spend a huge amount in order to earn additional MQMs through Delta Reserve Status Boosts. Pay federal taxes at 2% in fees. If you overpay, you’ll later receive a refund as a check or direct deposit.

- Earn Platinum elite status for almost 2 years: If you earn Platinum elite status early this year, you’ll have that status for all of the rest of this year (2021), all of 2022, and through January of 2023.

In this post, I’ll cover two versions of this plan. One version, the one-card solution, requires applying for only one Delta Reserve card. The two-card solution requires applying for two Delta Reserve cards: one business card and one consumer card.

Plan Details

Apply up for 1 or 2 Delta Reserve cards

It’s possible to apply for both the consumer version and the business version in order to pickup lots of redeemable SkyMiles and a total of 40,000 MQMs. Here are the current welcome bonus offers:

| Card Offer |

|---|

ⓘ $161 1st Yr Value Estimate$250 Delta Stays credit valued at $125 Click to learn about first year value estimates 80K miles ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Earn 80,000 bonus miles after spending $12,000 in eligible purchases on your new card in your first 6 months of card membership. Terms Apply (Rates & Fees)$650 Annual Fee Recent better offer: Earn 125k bonus miles after spending $15k in eligible purchases on your new card in your first 6 months of card membership. (expired 4/1/26) FM Mini Review: Excellent choice for frequent Delta flyers who can make use of Delta Sky Club® access and companion certificate. Also a good choice for big spenders seeking Delta elite status. |

ⓘ $503 1st Yr Value Estimate$200 Delta Stays credit valued at $100 Click to learn about first year value estimates As high as 100K miles ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer You may be eligible for as high as 100,000 Bonus Miles after you spend $5,000 in eligible purchases on your new card in your first 6 months of Card Membership. Terms apply. Rates & Fees$650 Annual Fee Recent better offer: 125,000 bonus miles after you spend $6,000 in eligible purchases on your new card in your first 6 months of card membership. (Expired 10/29/25) FM Mini Review: Excellent choice for frequent Delta flyers who can make use of Delta Sky Club® access and companion certificate. Also a good choice for big spenders seeking Delta elite status. |

Unfortunately, the $550 annual fee is not waived the first year. After the first year, you can, of course, downgrade to a cheaper Delta card or cancel altogether. The business card version of the offer includes a $200 statement credit (at the time of this writing) and so that’s obviously the better option for the 1-card solution.

More:

You must have a business (but you probably do): In order to apply for a business credit card, you must have a business. That said, it's common for people to have businesses without realizing it. If you sell items at a yard sale or on eBay, for example, then you have a business. Similar examples include: consulting, writing (e.g. blog authorship, planning your first novel, etc.), handyman services, owning rental property, renting on airbnb, driving for Uber or Lyft, etc. In any of these cases, your business is considered a Sole Proprietorship unless you form a corporation of some sort.When you apply for a business credit card as a sole proprietor, you can use your own name as your business name, use your own address and phone as the business' address and phone, and your social security number as the business' Tax ID / EIN. Alternatively, you can get a proper Tax ID / EIN from the IRS for free, in about a minute, through this website.

Is it OK to use business cards for personal expenses? Anecdotally, almost everyone I know uses business cards for personal expenses. That said, the terms in most business card applications state that you should use the card only for business use. Also, some consumer credit card protections do not apply to business cards. My advice: don't use the card for personal expenses if you're not comfortable doing so.

Here’s a summary comparison of the costs and benefits of the welcome offers:

| 1 Card (Business) | 2 Cards | |

|---|---|---|

| Card Annual Fees | $550 | $1100 |

| Statement Credits | $200 | $200 |

| Net Fees | $350 | $900 |

| Bonus Miles Earned | 80,000 | 160,000 |

| MQMs Earned | 20,000 | 40,000 |

Spend Big

In 2021 only, Delta Reserve cards offer 18,750 MQM bonuses (vs 15,000 MQMs in most years) when you complete $30K, $60K, $90K, and $120K spend within a calendar year. That offer expired in 2021.

In order to earn Delta Platinum status, assuming you have no other way of earning MQMs, this plan calls for spending a total of $90,000 in the one-card solution or $60,000 in the two-card solution.

An easy option at this time of year is to use the Delta Reserve card to pay federal income taxes. You can even overpay taxes now and get a refund once you file your annual tax return. The IRS doesn’t mind getting a loan (but I can’t rule out the possibility that this would increase chances of getting audited)

At the time of this writing, each of the 3 primary tax payment processors charge just under 2% in fees for paying taxes. Here are the scenarios, assuming 2% in fees:

| 1 Card | 2 Cards | |

|---|---|---|

| Amount Paid in Taxes | $88,270 | $58,850 ($29,425 per card) |

| Tax Payment Fees (2%) | $1,765 | $1,177 |

| Total Spend | >$90K | >$60K ($30K per card) |

| Miles Earned from Spend | 90,000 | 60,000 |

| MQMs from Status Boosts | 56,250 | 37,500 |

The 1-card solution requires much more spend, but it also earns more miles and MQMs than the 2-card solution.

For more about paying taxes by credit card, see: Complete guide to paying taxes via credit card, debit card, or gift card

Platinum Medallion Elite Status Complete!

Platinum status requires 75,000 MQMs. If you follow the above suggestions you’ll earn slightly more than 75,000 MQMs. And, fortunately, for anyone who earns elite status, Delta rolls over extra MQMs from one year to the next and so those extra MQMs won’t be wasted if you pursue elite status again next year. If you complete either of the above plans early this year, you’ll have Platinum status for all of the rest of this year (2021), all of 2022, and through January of 2023.

Here’s a summary of the two solutions:

| 1 Card | 2 Cards | |

|---|---|---|

| Net Card Fees | $350 | $900 |

| Fees from Spend (2%) | $1,765 | $1,177 |

| Total Fees | $2,115 | $2,077 |

| Miles Earned | 170,000 | 220,000 |

| MQMs Earned | 76,250 | 77,500 |

Costs vs Miles

One way to help justify spending so much money towards elite status is to look at the value of the redeemable miles you’ll earn along the way. It can be hard to justify spending a lot for hard-to-quantify elite benefits, but redeemable miles have tangible value towards flights.

Our Reasonable Redemption Values (RRVs) currently lists Delta SkyMiles at 1.3 cents. That means that we believe that it is reasonable to expect to get 1.3 cents per mile or better value when redeeming miles for award flights. Alternatively, you could more conservatively estimate the miles as being worth 1 cent each since that’s the value you get when using Delta’s “Pay with Miles” feature.

Let’s look at the two plans compared to the two valuations of Delta miles earned:

| 1 Card | 2 Cards | |

|---|---|---|

| Total Fees | $2,115 | $2,077 |

| Miles Earned | 170,000 | 220,000 |

| Mile Value at 1.3 Cents Per Mile | $2,210 | $2,860 |

| “Profit” | $2,210-$2,115 = $95 | $2,860-$2,077 = $783 |

| Mile Value at 1 Cent Per Mile | $1,700 | $2,200 |

| “Profit” | $1,700-$2,115 = -$415 | $2,200-$2,077 = $123 |

As you can see above, if you value miles at 1.3 cents each, then either solution results in a “profit” where the value of miles earned exceeds the costs involved in buying Platinum status. If you value miles at only 1 cent per mile, though, you’ll have a net loss of just over $400 with the 1-card solution. In my opinion, though, $400 is a bargain for nearly 2 years of Platinum elite status plus one year of lounge access (assuming you’ll make good use of both).

One Card or Two? Which Solution is Better?

Here again is a summary comparison of the two solutions:

| 1 Card | 2 Cards | |

|---|---|---|

| Net Card Fees | $350 | $900 |

| Fees from Spend (2%) | $1,765 | $1,177 |

| Total Fees | $2,115 | $2,077 |

| Miles Earned | 170,000 | 220,000 |

| MQMs Earned | 76,250 | 77,500 |

Total costs of the two solutions and MQMs earned are similar, but the 2-card solution offers 50,000 more miles. That makes the two card solution appear to be better, but I think that the one card solution is better for the following reasons:

- If Skymiles are important to you, you’d end up with more total Skymiles by going with the one-card solution and separately applying for the Delta Platinum or Delta Gold card.

- Amex generally doesn’t let you get an intro bonus again for a card you’ve had before. If you get both Delta Reserve cards now, you won’t be able to get the bonuses on these cards again for a very long time. With the one-card solution, though, you could get an MQM bonus again next year, or the year after, that by applying for the other card. Plus, this is a great way to extend the card’s perks (like Sky Club access): You could keep one Delta Reserve card for a year, cancel it and then apply for the other Delta Reserve card. This way you’ll get two years of benefits from the two cards instead of just one year of benefits as would happen with the two-card solution.

Consider cancelling after a year (or two)

If you go with the two card solution, it doesn’t make much sense to keep both cards more than a year unless you plan to manufacture Delta Diamond status (see: Manufacturing Delta elite status in 2020 and beyond). Most of the perks, such as Sky Club access are duplicative. For example, it doesn’t do you any good to have two reasons to have access to the Delta Sky Club.

You could cancel the card you don’t want or downgrade it to one of the cheaper Delta cards. One downside of downgrading is that you then won’t be eligible for a welcome bonus for the card you downgrade to. For example, if you decide you want a Delta Platinum card, you’re better off applying new for that card in order to get the welcome bonus rather than downgrading to it.

Whether or not to keep one Delta Reserve card long term is a tougher question. Yes, this card has great perks, but you can find even more perks, including Delta Sky Club and Centurion Lounge access, on the identically priced Amex Platinum card (not to be confused with the Delta Platinum card). And, unlike the Delta Reserve card, the Platinum card comes with airline fee credits and other credits to help offset the annual fee.

The biggest benefits that the Reserve card has over the Amex Platinum are the annual first class companion certificate, the ability to earn Delta elite status through spend, and the ability to get free upgrades if you don’t have Delta status. In other words, the Delta Reserve card makes the most sense for those who are sure to use the companion certificate towards good value each year and/or who covet Delta elite benefits. Others may do better with an Amex Platinum card or the lower priced Delta Platinum card.

One way to decide is to use our spreadsheet to compare similar cards. See: Which Ultra Premium Cards are Keepers?

Conclusion

As shown above, there’s currently a short term opportunity to buy Platinum status for around $2,100. In exchange, you’ll get Platinum status perks, redeemable Skymiles worth over $1,700, and several valuable Delta Reserve card perks. In my opinion, if you can float the high spend required to get this done AND if you’re a frequent Delta flyer who’s eager to get a taste of Platinum elite status then this deal may be for you. If you don’t check both of those boxes, I don’t recommend this approach.

See also:

- Delta Reserve Complete Guide

- Manufacturing Delta elite status in 2020 and beyond

- Complete guide to paying taxes via credit card, debit card, or gift card

")

My problem with Delta is that I do not see any good use for their miles.

There is no sweet spot with DL miles and I rather using transferable points.

Hello, I was attempting to refer a family member to the AMEX Delta Platinum card but the bonus they would receive is ony 40,000 instead of 90,000 miles. Is there some trick to being able to refer friends and have them qualify for the latest offer? Perhaps to call AMEX?

Thanks

I found that you can refer people to the good business versions of this offer (70K to 90K), but the consumer offers are all terrible via referral.

The MQM and spend elite thresholds now just look insanely high given Covid. Pre-Covid I felt any useful status was only in reach of road warrior business travelers, but now they just seem ridiculous. I’ve got to believe they will have to adjust those thresholds down. Going after the status now seems like a major waste.

Have you confirmed that this plan will work with the Reserve and Reserve Business in light of the fine print under “Status Boost” that states: “Card Members are only eligible to receive one annual bonus per threshold per calendar year for each type of eligible Delta SkyMiles Card (e.g., Platinum or Reserve) that is linked to the same SkyMiles account.” That seems to indicate that you could only get one $30k boost from the Delta Reserve line of cards instead of one each on the personal and business.

Yes, that language has been there for a while and yet it has continued to work. Despite the language, they treat the business and personal cards as separate and each can earn MQM boosts.

[…] A limited time opportunity to buy Delta Platinum elite status […]

I guess I thought that working on status in 2020 was for 2021. So if I currently have gold and meet requirements for platinum during this year, my 2020 status is upgraded?

Yes, you’ve got it right — you’re working on 2021’s status, but you get to enjoy the benefits for the rest of this year once you’ve met that requirement. For people earning the traditional way, that means they’ll probably qualify in November or December and enjoy Platinum benefits for a month or two this year and all of next year. If you leverage the credit card opportunity now, you could end up getting 8 or 9 months of status this year plus all of next year.

Essentially, status benefits are meant to encourage you to fly the airline. Once you’ve met the requirements, it’s not in the program’s interest to make you wait until next year to enjoy them. They want you to keep right on booking with them — so you get access to the benefits once you’ve met the requirement, be that in March or November or whenever it may be.

Greg

Why don’t u do a post on the Coronavirus in respect to seats . FBN just said to the end of April airlines canceled flts. They need to Fly them dead horses to make money or go BK . Hmmm I smell Deals coming up quickly long range aircraft as in EU .

CHEERs

I think your analysis of cost, especially if you’re doing it early in the tax year, should include some accounting for the opportunity cost of not investing the money elsewhere.

If you’re overpaying your taxes in expectation of a refund, you’re loaning the money out at no interest for about a full year — and foregoing perhaps 2% interest on it. That brings your cost on that money from 1.87 to 3.87 percent. The calculation is a little more complex if you’re just pre-paying future quarter estimated tax since you’re then losing 3, 6, or 9 months of interest but the the idea is the same.

If you’re a large-scale MS-er and could be cycling that money monthly I imagine the lost income might be even higher.

Am I missing something in this analysis?

You’re right about that, but my assumption here is that people will do this for their 2019 end of year taxes. So if you time it right, you’ll get back your overpayment quickly.

Larry

Large-scale MS-er’s get Shut Down u Loose it All by being GREEDY .

Cheers

CD: You mean Greg? He seems to be doing okay, right?

Larry

I mean u or anyone doing that or playing fast with the rules look @ the AA deal. Now as far as paying the IRS I’ve been doing that for 8 yrs to get a few needed points .Who cares if it 1.8000% or 3.88888% u folks Love to Split hairs .

Eating BK waiting for the Sun to come up in Hawaii with my well earned points.

LOL

CHEERs

Greg’s method is closely tied to the timing of being early in the yr. if you do this in Apr (1) the loan out is only 2-3 weeks instead of a full yr (2) Status will last about 20 months

I don’t know if u can do it 4/1 for 2019 without fines.? I did it 1/6 should get back like 3/20 just like last year .

Cheers

You can’t hold all your estimated payments until the last quarter or you will pay penalties, just like you said. But if you paid all along, and just make a large overpayment on your fourth quarter 2019 estimate, then you won’t incur penalties, and you should get the money back in a month or so. So, that particular strategy does work and your total cost is close to 2% (the 1.87% plus a little less than 0.2% on the month’s lost interest).