I’ve talked to many people lately who are struggling to decide whether to keep their Sapphire Reserve® cards when their next annual fee comes due. I’m in the same situation, so I figured it would make sense to walk you through how I’ve been thinking about it and the decision I made.

If you decide to cancel, I recommend using as many of the card’s new coupons as possible before it’s too late. See: Still got the Sapphire Reserve® card? Your new benefits are now live. Here’s what to do next.

Overview

Last year, Chase overhauled the Sapphire Reserve card. The old version was easy to understand and easy to recommend: it offered 3x points for travel & dining, and 1.5 cents per point value for travel booked through Chase Travel℠. Plus, a single easy $300 travel rebate brought the annual fee, after rebate, down to around $250. The new Sapphire Reserve card is more expensive, more complicated, and loaded with coupons. Now, depending on how you book your travel, you’ll earn 1x or 4x for travel (or 8x when booking through Chase Travel), and you can redeem points for up to 2 cents per point through Chase Travel, but you’ll usually get just 1 cent per point unless you got your card before June 23rd 2025, in which case points earned prior to October 26th 2025 are worth 1.5 cents each through Chase Travel, but only until October 26, 2027. Clear?

If you haven’t already been charged the new $795 annual fee, you should expect that fee a year after your last payment of the old $550 fee. I paid $550 on August 1, 2025, so I expect to be charged $795 on August 1, 2026. Until then, I can (and will) take advantage of as many of the card’s features & coupons as possible, regardless of whether I renew.

Is the card worth $795?

The Sapphire Reserve card comes with coupons that can be worth at least $795, but it depends on how and whether you use them. For example, the card offers $250 back, twice per calendar year, for 2-night or longer prepaid bookings through The Edit. Obviously, those coupons are worth nothing if you don’t use them. Less obvious is the fact that The Edit often charges much more than other booking channels for the same hotels. In those cases, you could get negative value from these coupons if you pay more than $250 extra.

One way to decide whether to keep the card is to fill in “Your Value” in the “Which Premium Cards are Keepers” spreadsheet. The idea is to decide, for each benefit, how much you’d be willing to prepay for it if it were available as a stand-alone subscription. Record that amount. If the total across all benefits equals or exceeds the annual fee, then the card is worth keeping. See the post about this spreadsheet for more information.

Bundling

One problem I have with the spreadsheet shown above is that there are many perks and coupons I wouldn’t even consider buying as a subscription, yet they still have value. For example, I would never consider prepaying for StubHub credit, but since it’s there, I happily used it to get free seats at a basketball game. Similarly, with Points Boost and The Edit credits, I wouldn’t prepay for them, but I like having them available in case good opportunities come up to use them.

The solution I came up with was to bundle perks and coupons that have some value but that I wouldn’t be willing to prepay for individually. For example, rather than trying to figure out how much I value each travel perk individually, I bundled a bunch of them together:

- My Travel Benefits Bundle: 4x flights & hotels; 8x travel through Chase; best in class travel protections; Points Boost; $250 The Edit credit

Similarly, I bundled together the miscellaneous other coupons that I like having, but have a hard time valuing individually:

- Misc Coupon Bundle: $150 x 2 Stubhub rebate, $10 x 12 Lyft credit; DoorDash benefits, free Apple Music

When taken as a bundle like this, I have an easier time assigning a “how much would I prepay” estimate. I’d be willing to pay at least $150 per year for those travel benefits, and at least $100 per year for those miscellaneous coupons. Meanwhile, coupons and perks that, individually, are valuable to me stayed separate:

- $300 travel credit: $280

- Free subscription to Apple TV+: $99

- Sapphire Reserve Exclusive Tables $150 per 6 months: $200

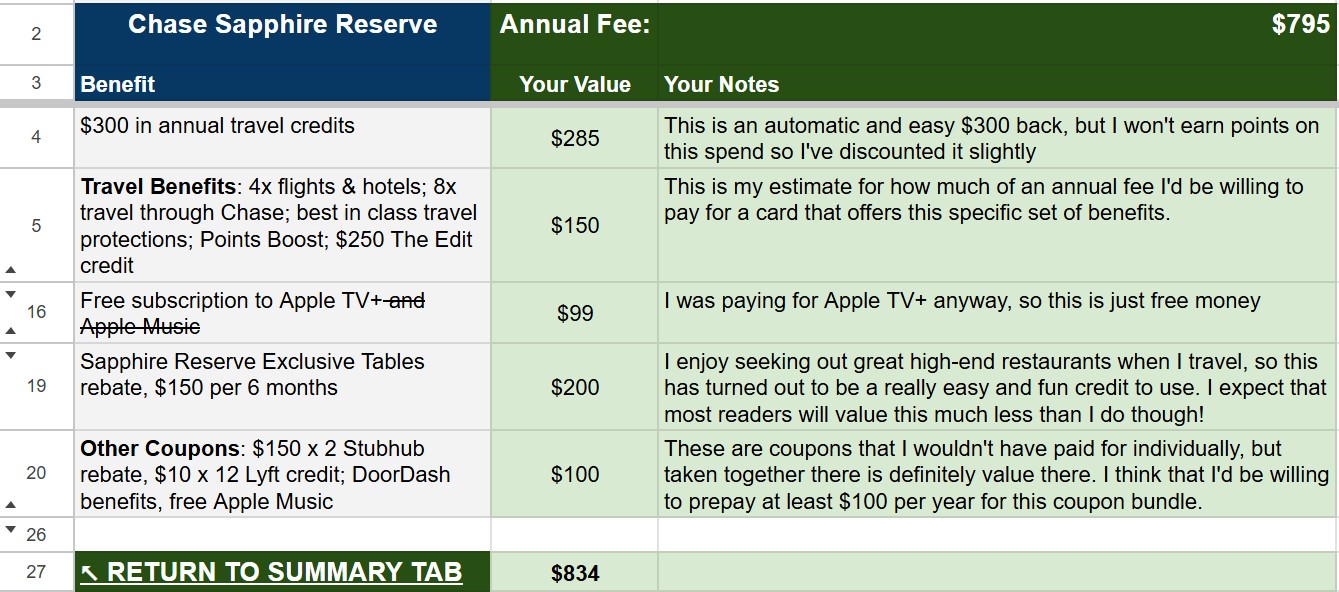

On my personal copy of the spreadsheet, I edited some rows to bundle items and hid rows for perks and coupons I don’t value. The result was this:

| Benefit | How much would you prepay? | Notes |

|---|---|---|

| $300 in annual travel credits | $285 | This is an automatic and easy $300 back, but I won’t earn points on this spend, so I’ve discounted it slightly |

| Travel Benefits: 4x flights & hotels; 8x travel through Chase; best in class travel protections; Points Boost; $250 The Edit credit | $150 | This is my estimate for how much of an annual fee I’d be willing to pay for a card that offers this specific set of benefits. |

| Free subscription to Apple TV+ |

$99 | I was paying for Apple TV+ anyway, so this is just free money |

| Sapphire Reserve Exclusive Tables rebate, $150 per 6 months | $200 | I enjoy seeking out great high-end restaurants when I travel, so this has turned out to be a really easy and fun credit to use. I expect that most readers will value this much less than I do though! |

| Other Coupons: $150 x 2 Stubhub rebate, $10 x 12 Lyft credit; DoorDash benefits, free Apple Music | $100 | These are coupons I wouldn’t have paid for individually, but taken together, they definitely have value. I think that I’d be willing to prepay at least $100 per year for this coupon bundle. |

| Total | $834 |

Your bundles and values may (& should) vary

There are coupons in the list above that you may not value at all, so you should remove them from your analysis. For example, I know people who subscribe to Apple One family plans. For them, the card’s Apple TV+ and Apple Music coupons are worthless. Also, there are many perks and coupons that I hid because I don’t value them at all, but you probably do. For example, the card offers Priority Pass Select & Sapphire Lounge access for you plus 2 guests. I don’t value this because I get the same benefit from my Ritz-Carlton card. If you don’t have the Ritz card, you should include a value for it, or bundle it with other travel perks. Other examples of perks I don’t value but you might include: IHG Platinum Elite status, roadside assistance, $10-per-month Peloton rebate, and perks you get with $75K in annual spend.

Is the card a keeper?

Bundling perks and coupons made it easier for me to come up with concrete amounts that I’d be willing to prepay for those benefits. In my case, the sum total came to $834, which is $39 more than the card’s annual fee, so it’s a keeper… for me.

Please, please, please understand that I am not saying that the Sapphire Reserve’s $795 annual fee is worth it for you. Your situation is different from mine. You should value things differently. I expect that most readers will decide that the card isn’t worth keeping! Regardless, I hope the concept of bundling perks & coupons helps you find your answer, as it did for me.

")

Let’s not forgot the first year offer of $250 towards a two night hotel stay with IHG, Omni, etc,

Greg, you have proven that the CSR value is very individual. I luckily renew in April. I have used quite a few of the new benefits. But I am still on the fence if I will get $795 of value. Considering that we have 2 Amex Platinums in the household, I think this is a downgrade. We get so much value out of our Platinums. I think Chase made a big mistake trying to copy Amex. For us, CSR removing 3x earn on cruises is a big deal. Which Citi Strata Premier earns very easily for $99/year.

I appreciate the honestly of this website and asking us to think for ourselves if a card is worth it

CSP is, CSR is not

Whatever shortcomings the CSR might have, it makes up for it with its incredibly robust set of transfer partners. (Humor intended.)

I’ve had mine since 2015. I just got the Morgan Stanley Amex platinum which is free for me. There are no Tables restaurants near me so that’s not an option. It just doesn’t pay. I’ll downgrade to preferred at next annual fee.

P2 got the Morgan Stanley Amex platinum as well . Had the CSR since it came out but most likely will be cancelling it in the fall when the AF posts. Its been a great card but too much work now.

I totally agree. Too much work. Having said that, I’m willing to work for the perks on the Platinum card because it’s free for me and because they have restaurants on RESY that are near me. CSR does not.

I also value the travel insurance. CSR insurance covered a $60k rental car stolen off the street mid-day in s*hole SF, a small accident in Lisbon, and a missed connection to Venice over the last few years. Similarly I tried to claim on AMEX Platinum insurance on another situation and I got denied.

Further I travel to the craziest places and my CSR card ALWAYS works, where I’ve been declined and need to talk to AMEX customer service when I was in Morocco and Turkey – no thanks.

As someone else said, if you are just breaking even on a card, unless there are other perks (transfer partners, lounge access, whatever) you are actually losing money on it.

In my case it was an easy no for the CSR despite having a ton of points (ton for me) and I lucked out and got a signup bonus for the CSP despite having had it previously.

That allows me to use the various transfer partners to hopefully get 4 or so business class tickets over the next year or two.

Amex is another one where I will keep one platinum (CS) and cancel the other one despite potentially breaking even. The final push was losing one of the restaurants we like from Resy so we are down to one good one we like but not enough to eat there that often.

Obviously anyone who does travel blogs have a completely different set of needs and travel plans.

That’s a big advantage of the approach FM recommends, thinking about how much you would prepay for credits. If you use that approach rigorously and thoughtfully then if you come out ahead the card is likely a keeper even if you are only a few dollars ahead because the other downsides to using coupons and credits are already built in. I see in comments below that a lot of people are erroneously interpreting his +$39 to be barely coming out ahead. But of course that is a heavily discounted value that already factors in the trouble and risks of using the credits.

I recently renewed my wife’s Global Entry membership. We have 3 cards that offer to pay the $120 fee for renewal. EVERY single card came up as invalid card number when I clicked Pay. I tried each card several times with the same result. When I attempted ACH payment, it went through immediately. It seems credit card banks and the government are not on the same page and now I question if this benefit is worth anything. I’ve already decided to cancel the card due to the annual fee. AMEX and Chase can continue their dick-swinging, I’m not playing.

There’s a time value to money too. This isn’t about value of your time to keep track of ‘coupons’. And no travel blogger ever talks about it. It’s about paying the annual fee up front and then accuring benefits after the fact: you’re giving the bank a loan in effect where you would otherwise be eaning at least decent interest if not more were it invested in a more risky investment (eg money market).

when you combine both the ‘time to keep track of coupons’ and ‘time value of money’, for many higher earners, the math comes out to be you need to make roughly double whatever you pay in annual fees on a card to keep the card. Otherwise you’re. Wttwr off just getting a 2% cash back card and ‘set and forget’.

The bloggers ignore this math because far fewer would sign up for the card and/or first year churn would be much higher. and that’s what drives their business.

How long do you have to wait to transfer those accrued points with a transfer bonus to some airline or hotel travel partner to get redeem for those hard-to-find J or F seats or lux suite? So then with considering time value of money did you really get $0.05-0.08 per point value on those end-partner points? Methinks not.

It’s a fair point. But I don’t think it has been completely ignored either.

There are two types of prepayments. The first is the coupon-like credits that you redeem throughout the year. If you follow Greg’s methodology and think about how much you would prepay for a credit then you should be taking this into account when you do your own valuation. I never give any credit full face value even if they are really easy to use for this reason. (And, of course, more complicated credits are devalued by a lot more to account for the complexity.) But for credits that are used during a year the cost of loaning your annual fee to the bank and getting it paid back over the year isn’t all that high because it isn’t a long term loan. But still, it should come out of your “How much would I prepay for this credit?” valuation.

The other type of prepayment is the cost of having assets tied up in points. This gets a lot of attention in the points and miles world, largely because the risk of points devaluations, but also because you could be earning interest on the cash. It is certainly one of the drivers of the “earn and burn” philosophy (although personally I think there a cases when hoarding can make sense). I account for this in my own valuation by using a CPP valuation in my calculations that is very conservative, far below what I usually get in redemptions.

Interestingly, the premium cards probably don’t suffer as much from the cost of loaning your money to the bank because you are getting most of your returns within a year. In Greg’s valuation of the CSR the only benefits that don’t pay out within the year are the values he places on the 4X and 8X earnings, lumped together under the Travel Benefits line.

What you are pointing out could be a big factor in thinking about whether it is worth it to pay a higher annual fee to get a card that earns higher multipliers. The Amex Gold card comes to mind here. I tend to be very hesitant to pay more just to get a card with higher multiplier unless the return is overwhelming. But for the ultra-premium cards this isn’t usually an issue because the value has to be there in the form of credits I would be willing to prepay to get and use within the year. Extra earning multipliers on the card rarely play much of a role in the valuation.

Obviously there are many bloggers out there who ignore these points, accepting coupon credits are face value and generally inflating the value of the cards to drive up referrals. One reason I like FM is that they are much more careful and thoughtful in this respect.

Greg — But is it worth your time to keep track of all of these myriad benefits that only have a net value of $39? I think that question makes most of the very high annual fee cards non-keepers. These cards are great for the SUBs, but downgrading after year one is probably the best move for most people.

It’s not a net value of $39. I expect to get far more value than that or else I wouldn’t be willing to prepay the amounts I listed.

The coupon book part of it is so annoying but esp when they don’t credit the coupon for weeks on end. Just make it easier , please

I enjoy these evaluations, always keeping in mind this applies to the person doing them. With all the coupons that are starting to be attached to cards, I’ve started evaluating differently. If I were going through this for myself and came up with the $39, I would interpret this as I’m only out $39 if I didn’t have this and didn’t have to go through all the gamification of the credits. Essentially -$39 for doing nothing. Then I would look at if I would use this card in everyday spend and regularly take advantage of the points multiplier (4X Amex Gold or 5X dining Prestige). With this card I wouldn’t, so it would be a pass. The older I get, the less work I want to do.

Thanks for sharing Greg even if we use the results to come up with a different conclusion.

I found an easier way to justify my annual fee on Amex platinum, go to 2025 annual statement, what credits received plus AMEX offers credits, in 2025 total is $1392, used lounges 6 times and point balance has increased by 20k. Keeper ! of course will reevaluate when the new increased annual fee his in November.

Did I miss the TSApre/GE reimbursement? I know it’s only every 4 or 5 years but this year mine’s due and it tips the scales on making the card a keeper

Many of us end up with so many TSA/GE credits every year that we don’t know what to do with them. It really shouldn’t tip the scales for anyone who regularly signs up for new cards.

I value cards so much less generously and I definitely don’t think it is a keeper after this year. I think of the annual fee as a “prepayment” – so everything needs to be something I spend anyway. The Edit hotels are too pricey, I don’t normally dine out at fancy restaurants, and I don’t use Lyft, Apple Music / TV, or stubhub. Only thing that makes it worth the annual fee is the sign-up bonus in the first year.

Luckily (for me? for them?) the ability to stack various credits (total of $900: $250 Edit, $250 special credit for 2026, $300 travel credit, and $100 offer for $600) saved it for 2026. I happened to be planning a trip with a two-night stay that qualifies for all these credits (for $620). I value these $900 credits to be $600 as I wouldn’t normally spend $600 for two nights (more like $300, if out of pocket) – so this almost pays for the annual fee + I can get good values from dining credit that lets me get out of the house for a special occasion with my husband.