Ultra-premium credit cards often have great perks like lounge access, elite status accelerators, free nights, companion tickets, etc. The problem is that the annual fees, which can be as high as $895, can be overwhelming. All of these pricey cards are worth getting for their initial welcome bonuses, but they can be very expensive to keep… especially if you have more than one. How can you decide which are worth keeping? We’ve created a spreadsheet that can help!

Since the last publication, the spreadsheet linked within this post has been updated from version 13 to version 14.7. In addition to many minor edits, here’s what’s new:

- New cards added to spreadsheet: Bilt Palladium, Citi AAdvantage Globe, Chase Bonvoy Boundless.

- Updated United cards with 10% award discount, better Polaris saver award availability, and improved earnings on paid flights.

- Updated US Bank Altitude Reserve to account for negative changes as of 12/15/25.

- Updated Amex Gold with the latest $10/month dining options, Hertz elite status, and 5X for prepaid hotels

- Due to popular demand, I restored the Estimated Annual Value column to all tabs. I had previously removed the column in favor of text explaining how to estimate the value yourself, since I can’t possibly come up with values that work for everyone. But people seem to like my made-up values, so they’re back.

The premium card worksheet

To help identify which cards to keep or cancel, I created a Google Doc spreadsheet with tabs for each of the most popular premium (hundreds of dollars per year) rewards cards. I’ve also thrown in some $95-ish cards for comparison. On each tab, you can enter your estimated value for each perk and then return to the summary tab to see which cards are keepers.

–> Click here to open and copy the spreadsheet into your own Google account

The rest of this post goes into detail about how I recommend using this worksheet, but here are quick tips for those who don’t plan to read the rest (I get it: even though there’s some really good stuff below, you’ve got other things to do):

- Don’t double-count overlapping perks! For example, assign a value to the Global Entry credit only to the card that you’re most likely to keep.

- Value perks based on how much you’d be willing to pre-pay if it were available as a subscription. Don’t estimate based on how much you’re likely to save.

- If your total value of perks equals or exceeds a card’s annual fee, then its a keeper.

Background

To make up for big fees, issuers have been adding “sponsored perks” where you can get rebates from spend with specific vendors (Peleton, DoorDash, Dell, Lyft, Saks Fifth Avenue, etc.). On paper, it appears that you can recoup more money than the annual fee for these cards. And you can, if you would actually pay for these products and services anyway. The reality, though, is different. Take the Amex Platinum Saks credits, for example. Each year, January through the end of June and again July through the end of December, you can get up to $50 back from Saks and Saks.com purchases, for a total of up to $100 back. If you regularly spend $50 or more at Saks, both early in the year and late in the year, then the rebate can be considered nearly its face value. But if you find yourself scrambling twice per year to figure out what to buy, the rebate should be worth considerably less to you. In my case, I hardly value these Saks rebates at all. It’s nice to get a free pair of socks and other miscellaneous stuff twice a year, but not nearly face value nice.

When it comes time to pay the annual renewal fee on each of your premium cards, it makes sense to evaluate whether or not the card’s perks and rebates are at least as valuable as the card’s annual fee. If the answer is “no”, then I recommend calling to cancel the card. If the card issuer offers a great retention bonus, great — keep the card for another year. If not, go ahead and cancel or, better yet, product change to a fee-free card if possible (note that Amex Platinum cards do not have a product change path to a free card).

If you decide to cancel rather than downgrade, please review our checklist for canceling credit cards to avoid losing points and other rewards.

How to estimate value

When you pay a credit card’s annual fee, you are essentially pre-paying for a year of perks that this card offers. The best way to determine what these perks are worth to you is to decide for each one how much you’d be willing to pay if it were available independently as an annual subscription. Consider the Amex Gold card’s Uber credits, for example. The Gold Card offers $10 per month in Uber / Uber Eats credits. On the surface, that sounds like an easy $120 for those of us who use Uber or Uber Eats often. But you shouldn’t value it at the full $120. Imagine if Uber sold a benefit like this separately: What would you pay annually to Uber in order to get $10 per month in use-it-or-lose-it credits? You wouldn’t pay $120, would you? It wouldn’t make sense to pay $120 upfront for a total of up to $120 in savings spread out through the year. Instead, you might pay $60 (for example) for $120 in credits.

Other examples:

- Chase Sapphire Reserve $300 Travel Credits: This is a really easy credit to earn since all travel purchases count. But how much would you pay in advance to get $300 back? Keep in mind, too, that the Sapphire Reserve doesn’t give you points for that $300 in spend. I’d argue that you shouldn’t value this perk at more than $285, and it would be reasonable to value it less.

- Amex Platinum up to $600 Prepaid Hotel Credit: Consumer and Business Platinum cards offer up to $600 back per calendar year towards prepaid Fine Hotels + Resorts® or The Hotel Collection bookings ($300 from January to June and $300 from July to December; The Hotel Collection requires a minimum two-night stay). That’s great, but how much would you be willing to pre-pay for this rebate? Keep in mind that unless you habitually book through Fine Hotels + Resorts or The Hotel Collection, you might end up not using this perk at all.

- Marriott Bonvoy Brilliant 85K free night certificate: You might save $500, $700, $900, or more off a hotel night when you use this certificate, but there’s no way you should pay that much in advance. The only reason to pay in advance for a free night certificate (especially one that expires within a year) is if you expect to get way more value than you paid. For example, you might be willing to pre-pay $300 for the chance to save $500 or more.

Overlapping perks

One and done perks

There are many valuable perks that have no incremental value if you have the same perk from multiple cards. For example, getting Hilton Gold status from one credit card is great, but getting it from a second card has no incremental value. Here are some more examples where you might value a perk from one card, but having it on multiple cards doesn’t make it any more valuable:

- Free checked bags

- Elite status with a specific hotel, airline, or car rental service

- Lounge access to a specific type of lounge

Diminishing return perks

Some perks have diminishing value with each extra card that offers the perk. For example, each of the Amex Platinum consumer cards (the regular consumer Platinum card, as well as those from Schwab and Morgan Stanley) offers $300 per year in Digital Entertainment Credits: Up to $25 per month back for select digital entertainment services. In my case, I subscribed to Youtube TV (which costs much more than $25 per month) anyway, and so I value this perk on my generic Platinum card at nearly face value. But I also have the Schwab Platinum card, which I have used to subscribe to Peacock Premium for $16.99 per month. I wouldn’t pay for Peacock Premium without the rebate, though, so here I value the perk at only about $25 total.

How to value overlapping perks

The trick to doing this right is to first figure out which of your cards are the most likely “keepers” and assign perk values to those cards first. Then go to your next most likely to keep cards, and only assign incremental value (if any) to perks that overlap with your keeper cards. And repeat with the next most likely to keep cards, and so on.

If you have a bunch of premium cards, this is not easy! For example, many premium cards offer Priority Pass memberships. If you have more than one, then it’s a good idea to figure out which card is the most likely “keeper”, but keep in mind that the value of Priority Pass varies by card. Many versions of Priority Pass no longer include free meals at Priority Pass restaurants. And details vary about how many guests you can bring in and what it would cost (if anything) to add authorized users with their own Priority Pass membership. One excellent option is the Chase Ritz card, which offers Priority Pass for 2 guests and free authorized users, each of whom can get their own Priority Pass for 2 guests. But the Ritz card isn’t easy to get (you have to start with a Chase Marriott consumer card and upgrade), and its perks aren’t ideal for everyone. Still, if you have the card and highly value its key benefits, such as the $300 incidental travel rebate and an 85K free night certificate, it makes sense for this to be your first-in-line keeper card. Estimate the value of Priority Pass on that card, but not on any others (unless the other card’s Priority Pass is better because it includes restaurants).

Sapphire Reserve & Sapphire Reserve for Business

I used to show my entire spreadsheet here, but my situation has become too complicated to explain in a single post. Many of the cards I have are keepers just because writing and talking about credit cards is my career. So, instead of using the spreadsheet for all of my premium cards, I filled it out just for the Sapphire Reserve and the Sapphire Reserve for Business. You’ll find my valuations below…

Important background: I have (and plan to keep) the Ritz-Carlton card, which offers a better version of Priority Pass than the Sapphire Reserve offers. The Ritz version offers the same access to Sapphire lounges, but at regular Priority Pass lounges, the Sapphire Reserve’s version allows 2 guests, whereas the Ritz version is unlimited. Additionally, Ritz card authorized users are free, and each gets their own Priority Pass.

Sapphire Reserve

| Card Offer and Details |

|---|

ⓘ $1169 1st Yr Value Estimate$300 travel credit valued at $285, $300 StubHub credit ($150 Jan-Jun and again Jul-Dec) valued at $75, $500 Chase The Edit credit (2x per calendar year) valued at $125, $300 Chase Dining credit for dining at Sapphire Reserve Tables restaurants ($150 Jan-Jun and again Jul-Dec) valued at $75 Click to learn about first year value estimates 100K Points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer 100K points after $6K spend in the first 3 months. $795 Annual Fee Recent better offer: Expired 6/15/26: 150K points after $6K on purchases in the first 3 months FM Mini Review: Good all-around card for frequent traveler. Best when paired with no annual fee Chase Freedom Flex, Freedom Unlimited & Chase Ink Cash cards. Click here for our complete card review Earning rate: 8X Chase Travel℠ ✦ 4X flights and hotels booked direct ✦ 3X Dining ✦ 5X Lyft (through September 2027) Base: 1X (1.5%) Flights: 4X (6%) Portal Flights: 8X (12%) Hotels: 4X (6%) Portal Hotels: 8X (12%) Dine: 3X (4.5%) Card Info: Visa Infinite issued by Chase. This card has no foreign currency conversion fees. Big spend bonus: After spending $75,000 each calendar year, get the following benefits: IHG One Rewards Diamond Elite Status ✦ World of Hyatt Explorist Status ✦ Southwest Airlines A-List Status ✦ $500 Southwest Airlines credit when booked through Chase Travel ✦ $250 credit to The Shops at Chase Noteworthy perks: $300 Annual Travel Credit ✦ Transfer points to airline & hotel partners ✦ Up to $500 The Edit credit annually ($250 twice per calendar year) ✦ Up to $300 Dining credit through Sapphire Reserve Exclusive Tables ($150 January to June and again July to December) ✦ Complimentary Apple TV and Apple Music for a minimum of one year when activated by 6/22/27 ✦ Up to $300 in StubHub credits ($150 January to June and again July to December) ✦ Points worth up to 2 cents each towards qualified bookings through Chase Travel ✦ Primary auto rental coverage ✦ Priority Pass Select lounge access ✦ Access Sapphire Lounges for yourself and 2 guests for free ✦ Access select Air Canada Maple Leaf lounges when flying Star Alliance ✦ Up to $120 Global Entry or TSA PreCheck® or NEXUS Application Fee Statement Credit ✦ IHG One Rewards Platinum status through 12/31/27 ✦ Free DoorDash DashPass through 2027 ✦ Two promos of $10 off each month on non-restaurant orders from DoorDash ✦ $5 off restaurant order each month from DoorDash ✦ $10 monthly Lyft credit See also: Chase Ultimate Rewards Complete Guide |

Here are my personal valuations for the Sapphire Reserve card. With one exception (Priority Pass), I only show perks that I gave a value to. All perks not shown were assigned $0 value. Please, please, please understand that your personal valuations should be different than mine. Additionally, there’s a good chance that you value some of the perks that I didn’t include at all below…

| Sapphire Reserve Benefit | My Value | My Notes |

|---|---|---|

| $300 in annual travel credits | $285 | I use this card for flight and hotel charges, so the rebate is automatic every year. |

| Priority Pass Select & Sapphire Lounge access for you plus 2 guests | $0 | I have a better version of Priority Pass thanks to my Ritz-Carlton card. |

| Best in class travel protections | $100 | I highly value this for the peace of mind it offers when paying for travel with this card. I appreciate that when I pay for airfare and hotels, I earn 4x, and get great travel protections. If I were into booking cruises or other types of travel that don’t earn 4x, I’d be less enthusiastic about this. |

| Free subscription to Apple TV+ and Apple Music | $110 | I already pay $10 per month for Apple TV+. This also gives me the opportunity to try out Apple Music to see if I like it as much as Spotify (and could therefore save money by cancelling Spotify) |

| The Edit hotel rebate, $250 twice per year | $100 | It will be interesting to see in practice how often I book 2+ night stays through The Edit. If it’s common, I’ll end up valuing this much more than $100 per year. |

| Sapphire Reserve Exclusive Tables rebate, $150 per 6 months | $100 | The list of eligible restaurants is very small, so I don’t know how often I’ll use this benefit. My guess right now is that I’ll use it at least once per year. |

| Stubhub rebate, $150 per 6 months | $50 | I don’t buy from Stubhub often, but I’d be willing to pay $50 in advance for this semi-annual rebate. |

| Lyft rideshare benefits. $10 ride credit per month plus earn 5X points on Lyft rides through September 2027 | $25 | I’m guessing that I’ll use the $10 Lyft discount at least 3 or 4 times per year, and often more. |

| DoorDash thru 12/31/27: Free DashPass for 12 months after activation. Two $10 discounts per month on non-restaurant orders and one $5 discount per month on restaurant orders. | $25 | Just guessing that I’ll get enough value from this to be worth “paying” $25 per year |

| My Total: | $795 |

This was a weird coincidence! My valuation came to $795, which is the exact new annual fee for this card. Since my estimates were based on what I’d be willing to pay in advance for these features, rather than the amount of value I expect to receive, this means that I should keep the Sapphire Reserve even when my annual fee increases to $795. Of course, by then my valuations of some of these things are likely to change, so I’ll do this exercise again at that time.

Sapphire Reserve for Business

| Card Offer and Details |

|---|

ⓘ $2185 1st Yr Value Estimate$300 travel credit valued at $285, $500 Chase The Edit credit (2x per calendar year) valued at $125, $100 GiftCards.com credit ($50 Jan-Jun and again Jul-Dec for cards purchased from https://reservebusiness.giftcards.com/) valued at $50 Click to learn about first year value estimates 200K points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer 200K points after $30K spend in first 6 months.$795 Annual Fee Recent better offer: None FM Mini Review: Could be very appealing for a business that books a lot of travel, as it earns 8x through Chase Travel℠ or 4x when booking direct through airline and hotels. It has decent perks, best-in-class travel protections, and earns valuable Chase Ultimate Rewards points. Best when paired with no annual fee Chase Freedom Flex, Freedom Unlimited & Chase Ink Cash cards Earning rate: 8X Chase Travel℠ ✦ 4X flights and hotels booked direct ✦ 3X social media and search engine advertising ✦ 5X Lyft (through September 2027) Card Info: Visa Infinite issued by Chase. This card has no foreign currency conversion fees. Big spend bonus: After spending $120,000 each calendar year, get the following benefits: IHG One Rewards Diamond Elite Status ✦ World of Hyatt Explorist Status ✦ Southwest Airlines A-List Status ✦ $500 Southwest Airlines credit when booked through Chase Travel ✦ $500 credit to The Shops at Chase Noteworthy perks: $300 Annual Travel Credit ✦ Up to $500 The Edit credit ($250 twice per calendar year) ✦ Up to $400 ZipRecruiter credit ($200 January to June and again July to December) ✦ $200 Google Workspace credit ✦ $100 Giftcards.com ($50 January to June and again July to December for purchases at giftcards.com/reservebusiness) ✦ Points worth up to 2 cents each towards qualified bookings through Chase Travel(SM) ✦ Transfer points to airline & hotel partners ✦ Primary auto rental coverage ✦ Priority Pass Select lounge access ✦ Access Sapphire Lounges for yourself and 2 guests for free ✦ Access select Air Canada Maple Leaf lounges when flying Star Alliance ✦ Up to $120 Global Entry or TSA PreCheck® or NEXUS Application Fee Statement Credit ✦ IHG One Rewards Platinum status through 12/31/27 ✦ Free DoorDash DashPass through 2027 ✦ Two promos of $10 off each month on non-restaurant orders from DoorDash ✦ $5 off restaurant order each month from DoorDash ✦ $10 monthly Lyft credit See also: Chase Ultimate Rewards Complete Guide |

I was curious whether the Sapphire Reserve for Business might be a better option for me than the Sapphire Reserve. So, I filled out the tab for this card as if I didn’t also have the Sapphire Reserve. Here are the results…

| Sapphire Reserve for Business Benefit | My Value | My Notes |

|---|---|---|

| $300 in annual travel credits | $285 | I use this card for flight and hotel charges, so the rebate is automatic every year. |

| Priority Pass Select & Sapphire Lounge access for you plus 2 guests | $0 | I have a better version of Priority Pass thanks to my Ritz-Carlton card. |

| Best in class travel protections | $100 | I highly value this for the peace of mind it offers when paying for travel with this card. I like too that when paying for airfare and hotels I earn 4x. If I were into booking cruises or other types of travel that don’t earn 4x, I’d be less enthusiastic about this. |

| The Edit hotel rebate, $250 per 6 months | $100 | It will be interesting to see in practice how often I book 2+ night stays through The Edit. If it’s common, I’ll end up valuing this much more than $100 per year. |

| Google Workspace rebate, $200 per year | $190 | I spend more than $200 each year on Google Workspace, so this is an easy win. |

| Gift card credit, $50 per 6 months for purchases at giftcards.com/reservebusiness | $50 | I’d pay $50 to get two $50 gift cards each year. |

| Lyft rideshare benefits. $10 ride credit per month plus earn 5X points on Lyft rides through September 2027 | $25 | I’m guessing that I’ll use the $10 Lyft discount at least 3 or 4 times per year, and often more. |

| DoorDash thru 12/31/27: Free DashPass for 12 months after activation. Two $10 discounts per month on non-restaurant orders and one $5 discount per month on restaurant orders. | $25 | Just guessing that I’ll get enough value from this to be worth “paying” $25 per year |

| My Total: | $775 |

This one ended up just barely shy of its $795 annual fee. So it’s clear that the consumer version of the card is a better fit for me.

A friend’s example (From Feb 2024)

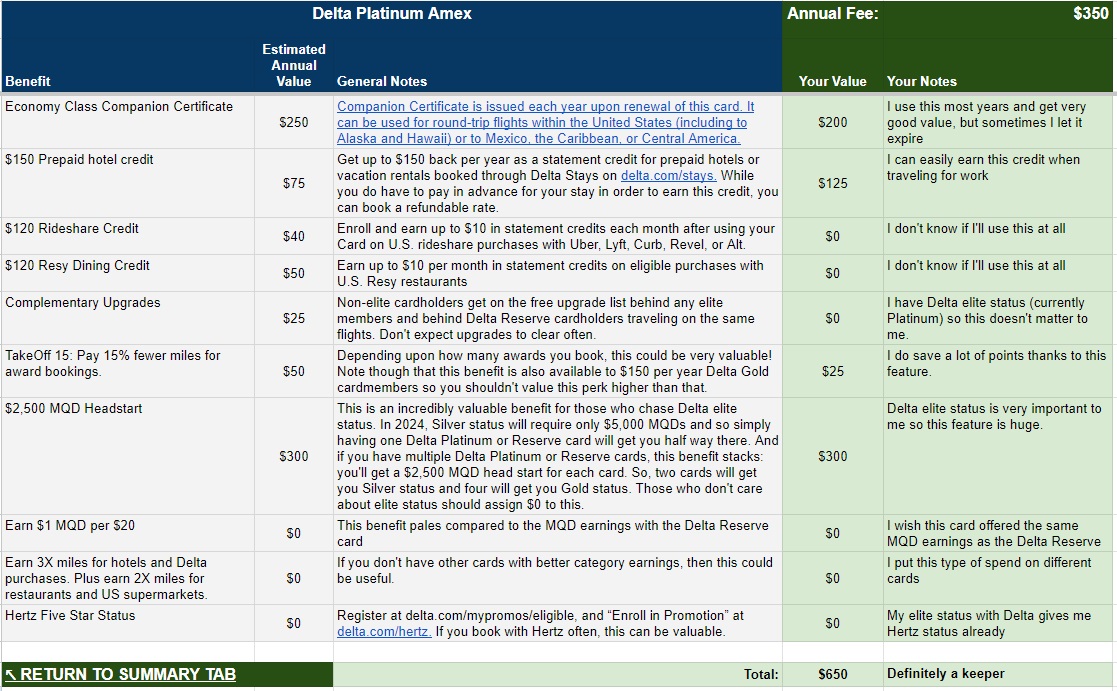

In this example, I created a spreadsheet for a friend. She has the Delta SkyMiles Platinum card. She also currently has Delta Platinum Medallion Elite status and values that highly. She is thinking about upgrading her Delta Platinum card to a Reserve card in order to get Delta Sky Club® access and to get a better way of earning Medallion Qualifying Dollars towards elite status through credit card spend. She has a job where she is reimbursed for travel that she pays for herself and so she believes that it would be very easy for her to use the Delta Stays hotel credits available through Delta cards.

For this exercise, I filled out the spreadsheet on my friend’s behalf as if I were her and imagined her valuations for each card perk…

Delta SkyMiles Platinum Card

| Card Offer and Details |

|---|

ⓘ $758 1st Yr Value Estimate$150 Delta Stays credit valued at $75 Click to learn about first year value estimates Up to 100K miles ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Earn 80K bonus miles after $4K in purchases with your new card, and an additional 20K bonus miles after an additional $2K in purchases on the card, both within your first 6 months. Terms apply. Rates & Fees (Offer Expires 7/15/2026)$350 Annual Fee Alternate Offer: Dummy booking offer of 70K + $400 credit. See this for more details. FM Mini Review: Good choice for frequent Delta flyers who can make use of annual companion certificate Earning rate: 3X Delta ✦ 3X purchases made directly with hotels ✦ 2X eligible restaurants ✦ 2X US Supermarkets ✦ 1X everywhere else Card Info: Amex Credit Card issued by Amex. This card has no foreign currency conversion fees. Big spend bonus: Earn 1 Medallion Qualifying Dollar (MQD) per $20 spent Noteworthy perks: 15% off when using miles to book an award flight (Delta metal only) ✦ Receive $2,500 Medallion(R) Qualification Dollars each Medallion Qualification Year ✦ US, Caribbean, or Central American economy companion certificate (subject to taxes & fees) each year upon card renewal ✦ Earn up to $150 as a statement credit each year after booking prepaid hotels or vacation rentals with your Card through Delta Stays on delta.com/stays ✦ Up to $10 per month in statement credits for US purchases with select rideshare service providers [enrollment required] ✦ Up to $10 per month in statement credits on eligible purchases with U.S. Resy restaurants [enrollment required] ✦ Priority boarding ✦ One checked bag free on Delta flights + an additional free bag on domestic Delta flights ✦ Complimentary upgrades: get added to the complimentary upgrade list after Delta elite members and Reserve cardmembers ✦ Cell phone protection ✦ Terms and Limitations Apply. |

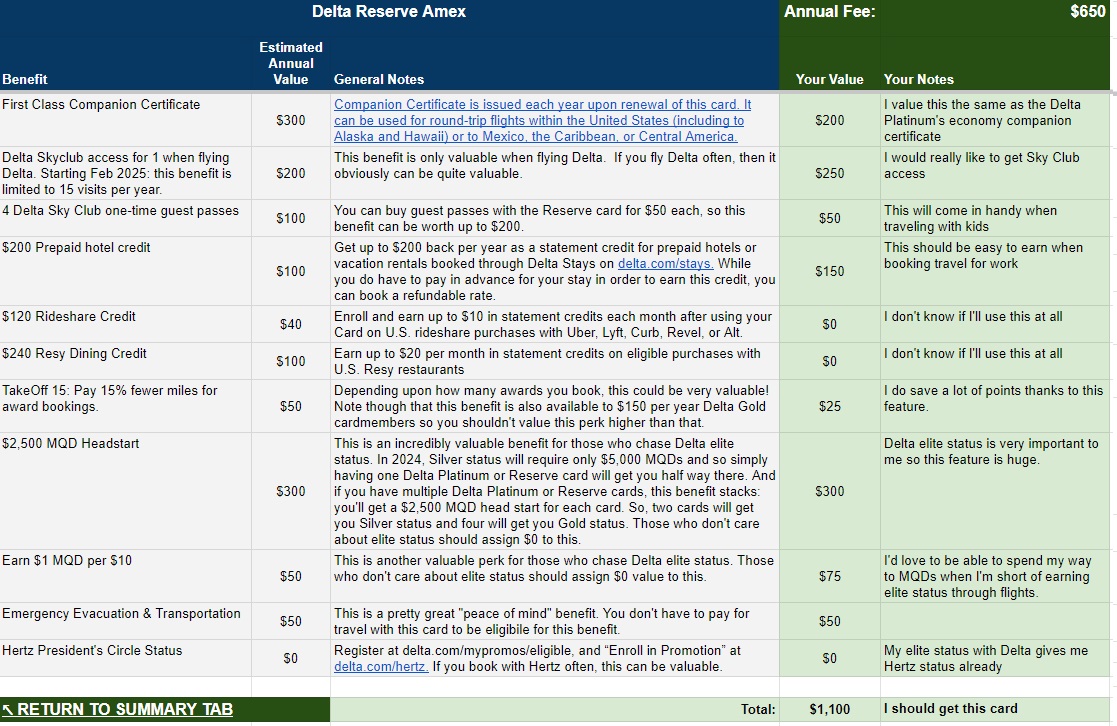

Primarily because my friend highly values Delta Elite status and this card offers a $2,500 MQD Headstart, it’s a clear winner. That said, she may do even better with the Delta Reserve card, so I filled that out on her behalf as well.

Delta Reserve Card

| Card Offer and Details |

|---|

ⓘ $712 1st Yr Value Estimate$200 Delta Stays credit valued at $100 Click to learn about first year value estimates Up to 125K miles ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Limited Time Offer: Earn 100K miles after $6K or more in purchases within the first 6 months and an additional 25K miles after an additional $3K in purchases within your first 6 months. Terms apply. Rates & Fees (Offer Expires 7/15/2026)$650 Annual Fee Recent better offer: 125,000 bonus miles after you spend $6,000 in eligible purchases on your new card in your first 6 months of card membership. (Expired 10/29/25) FM Mini Review: Excellent choice for frequent Delta flyers who can make use of Delta Sky Club® access and companion certificate. Also a good choice for big spenders seeking Delta elite status. Earning rate: 3X Delta ✦ 1X everywhere else Card Info: Amex Credit Card issued by Amex. This card has no foreign currency conversion fees. Big spend bonus: Earn 1 Medallion Qualifying Dollar (MQD) per $10 spent Noteworthy perks: 15% off when using miles to book an award flight (Delta metal only) ✦ Receive $2,500 Medallion(R) Qualification Dollars each Medallion Qualification Year ✦ Companion Certificate on a Delta First, Delta Comfort, or Delta Main round-trip flight to select destinations each year after renewal of your Card. (subject to taxes & fees) ✦ Delta Sky Club® access when flying an eligible Delta flight: 15 visits per year to be used from February 1 until January 31 of the next calendar year (after 15 visits have been used, additional visits can be purchased for $50 each) or to earn an unlimited number of visits, spend $75K or more on eligible purchases each calendar year. ✦ 4 Delta SkyClub one-time guest passes ✦ Centurion Lounge access when flying Delta same day (flight must be booked with your Reserve card) ✦ Earn up to $200 as a statement credit each year after booking prepaid hotels or vacation rentals with your Card through Delta Stays on delta.com/stays ✦ Up to $20 per month in statement credits on eligible purchases with U.S. Resy restaurants [enrollment required] ✦ Up to $10 per month in statement credits for US purchases with select rideshare service providers [enrollment required] ✦ Complimentary upgrades: get added to the complimentary upgrade list after Delta elite members ✦ Up to $120 Global Entry fee or up to $85 for TSA Precheck credit every 4 years ✦ Priority boarding ✦ One checked bag free on Delta flights + an additional free bag on domestic Delta flights ✦ Hertz President's Circle Status [Enrollment required] ✦ Terms and limitations apply. |

The Delta Reserve card has even more upside in this example than the Delta Platinum card. My friend would get Sky Club access and the ability to earn a reasonable number of MQDs through spend. She should apply for a Reserve card (that’s better than upgrading because she’d be able to earn a welcome bonus) and then either keep or cancel her Delta Platinum card. An advantage to keeping it is that the MQD Headstarts are additive, so she could get even more of a boost towards elite status. If she thinks that she can make good use of two companion tickets each year, then this would be a good strategy.

An even better strategy for my friend would be to consider obtaining Delta business cards. They have the same annual fees and perks as their consumer counterparts, but come with even more hotel credits. To keep things simple for this exercise, though, I made the assumption that she is not comfortable applying for business cards.

Thank you for this very valuable resource!! I think that the AA Globe card is missing the 4 Admiral’s Club annual passes. That is listed as a $100 benefit on the Citi Strata Elite.

Thank you! Fixed!

add this line at the end to total all of the annual fees

=SUMIF(B5:B50,TRUE,D5:D50)

I also added in other cards at the bottom that I have with annual fees…

This is seriously incomplete because it omits the single most valuable card WHEN MEASURED BY YOUR OWN METHODOLOGY. The Bilt Palladium Card has a value of $3149 according to the FM First Year Value. See “Using Frequent Miler’s Valuation Method, The Bilt Palladium Card Is The Most Valuable Card They Have Ever Seen, Even With Zero Housing Spend” (use Google — this site censures comments with URLs).

Note that this analysis assumes zero housing benefit, so it is a lower bound on Bilt value. Your value is likely much higher.

Note that FM’s posted value of $600 for Bilt is a nonsense, just the result of their laziness keeping the value up to date. Bilt’s revolutionary invention of an internal currency has rendered their current values meaningless. I seriously doubt that FM actually understands the iconic nature of Bilt. They think it is just another card.

…Palladium is second on the list in the spreadsheet?

Explain FM’s first year valuation? Is it right?

I have 3 Premium cards, CSR, Aspire and Atmos Summit. I used your spreadsheet for all 3. I’m ahead on CSR and Aspire and about break even on Summit.

I’m mostly an Alaska flyer out of SAN and Gold. The 10,000 EQM on the card is the equivalent of two R/T to Hawaii. Keeps the mileage runs to a minimum.

Thank you! Amazing spreadsheet! Can you please add the AAdvantage Platinum Select World Elite MC even though its a low cost card? The title on Venture X Business may be missing “Business.”

Thanks! Fixed the Venture X Business label. Will add the AA card in a future release.

We have a ton of cards on our cull list (will PC to no AF versions or low AF cards).

We cracked 13K in AF last year mainly because of PC to CSR pre-refresh and took upgrade offers for two gold to Amex Plt – also pre-refresh, also we also added Atmos Summit 105K SUB and Amex DBP and UA Quest and PCd two Surpass to additional Aspires.

We have gotten outsized value out of the Refreshed cards used EDITs with 2X~2.5X Points Boost and used both bonus $250 Hotel credits. AF $550.

That said CSR not a keeper- with Ritz card and a Brilliant.

USB AR is still a keeper – with 8x $28 – at PDX we still a Capers market with grab n’ go that makes a great brunch following day.

Cap1 VenX so far still a keeper

Amex Personal Plats – still a keeper with CL/DL SkyClub access – the FHR/THC still amazing value – the Hotel Collection now includes free brekkie and the $100 credit as well – some amazing deals still available with THC. The 4PM late check-out is amazing.

Should point out the Ritz-Carlton card has the same Priority Pass benefits as CSR now with the recent downgrade from unlimited guests to 2. Still good enough for my needs (I’m going to request a retention offer on my CSR, or downgrade it to CSP).

Thanks. I had previously updated it in the spreadsheet, but forgot to update its mention in this post. Fixed.

I’m still on the plus side with CSR but it has definitely become more complicated to use. It is still on my keep list for now.

I hadn’t seen this spreadsheet before, and it’s really helpful. Thanks! One of my goals this year is to maximize the perks on our premium cards (me and P2). When I did a deep dive, I found there were perks we would use or had forgotten about that really made the annual fee worthwhile. As for the Sapphire Reserve, I value that card above all others. Last year P2 had to have emergency surgery and we had to cancel a cruise and accompanying flight and hotel reservations the day before sailing. We had put the charges on the Reserve card and the travel insurance covered everything! We received all cruise and airline charges back with the insurance coverage on the card. That peace of mind is priceless to me.

Thanks for updating this. I’d value this spreadsheet at $100 at least! What a perk.

It is fascinating of course to see what you might value versus what I would. On the Amex Plat, I value 5x direct points highly – definitely getting a couple hundred bucks more points versus a 2x card (or former 3x with CSR travel category) and value booking direct. Whereas I value Clear at pretty much $0 and you have $100. But even with plugging in different values I’m circling the same square and getting to $2100 of value where you’re at more like $1800.

And Amex Plat still an amazing deal especially versus CSR. I feel like you stretch to get to ~$1100 in value. My personal math adds up to ~$1300 but this card is far from the slam dunk it once was. Best value is now access to Chase Lounges, and frankly, C1VX may be much cheaper / easier for some (in NY for instance Chase/C1 lounges are in the same LGA and JFK terminals)

To each their own! And I think that’s the point of this and why it’s helpful to have a straw man – to challenge your own assumptions.

100%.

Amex Plat. CSR. (Personally, still working towards C1VX, gotta get to like 0/24 first, sheesh). But, no love for Citi Strata Elite? C’mon… 6x Citi Nights… bah!

On CLEAR, since you fly AA, you probably haven’t used it much at either LGA B or JFK 8, because they don’t have it. (Don’t worry, they’ll make up for it with more MCE… someday… one would hope.)

I mean, I don’t only fly AA (but yes AA is not a Clear investor unlike DL/UA). I find the Clear kiosks / employees annoying compared to just going through the regular TSA Pre line. And now with Touchless ID from TSA Pre we’re flying through even faster. So I struggle to see the point of Clear, although occasionally it does have the shortest line.

If we are talking about “non-premium value” then Citi has to be in the conversation, because for $95 a year (or $0 if you use the $100 hotel credit) it’s a Citi Strata Premier, Citi Strata and a DoubleCash. That has to be the most well rounded points earning structure within an ecosystem for under $100 in fees. But do enjoy those Citi Nights while you are enjoying all of that amazing year 1 CSE value!

We flew out of SMF Sunday night (even had a long line for the Bus back to Terminal from car rental).

Touchless ID line was closed (no TSA agents) probably a 15± min line at Pre-Check – but Clear did get us straight to front of TSA line to the Agent who told us Touchless was closed (should have had a barrier belt pole closing the line).

That said in the 7+ years we have had Clear (free trials and Amex cards) it honestly has only been a real time saver 2-3 times – I would never pay for it out of pocket – I value it maybe $5 year – PDX (home hub) since remodel with new x-ray machines (they also added Clear lines with the extra space) – waits have really been negligible – we also tend to avoid peak travel dates and times. We have it on many Amex cards so we have family and MIL covered.

Agreed. If it weren’t for the Platinum reimbursement, I would not have CLEAR.

Big fan of the no-fee Strata… that 3x back on barbershops, hair salons, spas, nail places, etc. really helps me and P2 out. Much rather earn 3x than 2x on that stuff.

Double Cash is awesome no-fee catch-all, especially when combined TY points across all cards. But also, the 5x up to $500 on the Custom Cash is great for first category (especially for gas, if you drive, or even just when renting car refueling).

Citi as its merits. Glad their brought back the AA transfers. That was huge.

Thanks! And, yes, that’s exactly the point of this. Everyone has different circumstances, so the idea is to help you figure out which cards are best for you long-term.

Should the Southwest Priority and Performance Business cards get added now that they have cracked $200+ annual fee status?

Yes, great suggestion. I should add the JetBlue Premier card too

For the personal Sapphire Reserve, isn’t there a Peloton credit that you use? I thought I remembered you saying that you used that during one of the podcasts (not 100% sure tho). I don’t see it listed as one of the potential credits. That would add up to $120 to the annual value of the card. I appreciate you guys being a proponent of the “pre-paid credit” method for evaluation – it’s super helpful.

It’s line 22 of the CSR tab, at least for me.

The Peloton credit is there in the spreadsheet, but no, I don’t use it.

I’ve been following this for a while, and TBH, I have a few too many cards with overlapping benefits (Resy, Hotel Credits, etc.), which are “regular” benefits, and I’m wondering if there’s a way to have a “checkbox” or similar to serve as a reminder of what’s available?

Also, how can I configure to only show spreadsheets from cards I own? I think it used to work with the check box on the Summary, but that’s not happening any more.

It’s pretty mind blowing Bilt Palladium isn’t in the list of cards you can track on the spreadsheet.

I’ll add that card soon!

The UA business card earns 5000 anniversary miles if you also hold the Gateway or other personal card. I think it’s missing from your table. Since Pay Yourself Back usually allows 1.5c/m that’s a floor value of $75 off the annual fee.

Good catch! I’ll update that soon.