NOTICE: This post references card features that have changed, expired, or are not currently available

Today World of Hyatt and Chase have announced a brand new World of Hyatt Business Credit Card. I was ready for Chase and Hyatt to serve up a decadent delight of a luxury card that would demand indulgence and so my first reaction was disappointment when I sunk my teeth into what initially tasted like a nothingburger in the announcement of the business card. However, after attending the launch event in New York City yesterday and having some time to digest the changes, I realize this card may be a great fit for big spenders who want a (slightly) easier path to status — and especially for those small business owners who plan to redeem a lot of Hyatt points. This card won’t offer the most points per dollar of spend, but the benefits may make it more valuable for some.

New Card Details & High-Level Summary

| Card Offer and Details |

|---|

ⓘ $1111 1st Yr Value EstimateClick to learn about first year value estimates 80K points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer 80K after $10,000 spend in the first 3 months.$199 Annual Fee This card is subject to Chase's 5/24 rule. Recent better offer: 60K points after $5K in the first 3 months + Category 1-4 Free Night Certificate after $15K total in the first 6 months. (Expired 3/6/25) FM Mini Review: Great for its initial welcome offer and for Hyatt enthusiasts to spend toward status and rebate on award stays. Earning rate: 2X on fitness clubs and gym memberships ✦ 2X in the top 3 spend categories each calendar quarter. Eligible categories include dining; airline tickets purchased directly with the airline; car rental agencies; local transit and commuting; gas stations; internet, cable and phone services; social media and search engine advertising; and shipping ✦ 4X Hyatt and Mr & Mrs Smith Card Info: Visa Signature issued by Chase. This card has no foreign currency conversion fees. Big spend bonus: Get 5 elite qualifying night credits every time you spend $10,000 in purchases on a calendar year basis ✦ After $50K spend in a calendar year, get 10% back on redeemed points for the rest of that calendar year (Up to 20K points back per year) Noteworthy perks: Discoverist elite status ✦ Ability to gift Discoverist to up to 5 employees (they do not need to be cardholders) ✦ Up to $100 each cardmember year in Hyatt statement credits: Spend $50 or more at any Hyatt property and get a $50 statement credit up to two times per year ✦ Hyatt Leverage membership with no minimum stay requirements ✦ Complimentary Instacart+ for 3 months (must activate by 12/31/27) ✦ $10 monthly Instacart credit |

The card comes with a reasonably strong welcome bonus of 75K points. Beyond that bonus, the key benefits of the card are:

- An “adaptive” 2x that rewards you for the three categories in which you spend the most each calendar quarter through 12/31/22 (and then top two categories thereafter).

- 5 elite night credits with each $10K spend

- 10% back on redeemed points after spending $50K in a calendar year (Up to 20K points back per year). Note that the rebate kicks in on stays completed after reaching $50K in purchases.

- Up to $100 in Hyatt credits: Spend $50 or more at any Hyatt property in the world and get a $50 statement credit up to twice per cardmember year.

- Discoverist status for the cardholder and the ability to gift that status to 5 employees (those employees do not have to be employee cardholders)

Many will notice that this card does not come with an annual free night certificate or annual elite night credits. That certainly differentiates it from the consumer card. Note that you can have both the consumer and small business versions of the card if you qualify / are approved by Chase.

| Chase's 5/24 Rule: With most Chase credit cards, Chase will not approve your application if you have opened 5 or more cards with any bank in the past 24 months. To determine your 5/24 status, see: 3 Easy Ways to Count Your 5/24 Status. The easiest option is to track all of your cards for free with Travel Freely. |

Analysis

Update: We are now told that there is a cap of just 20,000 points back per calendar year. That is surprisingly low and changes the analysis significantly. A further update to this post is coming.

At the outset, I was underwhelmed by this card’s bonus categories and disappointed that it lacks a free night certificate or automatic annual elite night credits. It has an innovative-ish adaptive bonus category system where you automatically earn a bonus in the three categories in which you spend the most each quarter for the first year and then only the two categories in which you spend the most thereafter. I call this only innovative-“ish” because Citi stole the thunder on that idea with their Custom Cash card (albeit on the consumer side). I should note that Citi wasn’t the first to offer that type of feature, but the first of the major transferable currencies to do so.

While on the one hand adaptive bonus categories might be useful for a small business owner (Chase presented this as a good option for a new business that might be spending more on advertising one quarter to get the word out about the company and more on shipping the next to get the product out to customers), the problem some will see is that the bonus categories almost entirely overlap with the Chase Ink Business Preferred. Worse yet, while the Chase Ink Business Preferred offers three Chase Ultimate Rewards points per dollar spent (that could be transferred to Hyatt or kept as flexible Ultimate Rewards points that are transferable to a number of programs 1:1), the World of Hyatt Business card will only offer two World of Hyatt points per dollar spent in the categories in which you spend the most (and 1x everywhere else other than at Hyatt).

However, as a Chase executive pointed out when I questioned why someone would choose this card over the Ink Business Preferred, the choice here is a business decision. The Ink Business Preferred will give you more points. The World of Hyatt Business card will give you an accelerated path to elite status and milestone benefits and a 10% rebate on award redemptions after you spend $50K in a calendar year. Which option makes more sense will come down to how much you value elite status, milestone benefits, and that 10% rebate.

For those who redeem a lot of Hyatt points (and who can comfortably meet $50K spend relatively early each year), I could see this card being worth the trade-off.

For example, let’s say that you intend to redeem 500K World of Hyatt points. If you spend $50K in one or two qualifying categories on the World of Hyatt card, you would have 100K points from spend (at 2x). If you complete that spend before completing your stays, you’ll get 50K points back — essentially having earned 150K net Hyatt points on $50K spend.

Update: We have been informed that there is indeed a cap on the number of points back each year. My first question at the press event was whether there was a cap on the 10% rebate and how it worked. We were surprised to find out today that there is a 20,000-point cap on points back. That means that you will only receive the 10% back on the first 200K points redeemed after reaching $50K in purchases. To be clear, you only get 10% back on stays consumed after reaching $50K in purchases — the rebate isn’t retroactive.

This update changes much of my original math. If one spends $50K in a 2x category, they would earn:

- 100K points at 2x

- Up to 20K points back if they redeem 200K points after reaching $50K in purchases but during the same calendar year

That comes out to a sort-of net 120K points on $50K spend assuming you do redeem 200K points in the same calendar year. Given that one could earn 3x in many of the same categories on the Ink Business Preferred (or 3x on dining with other Chase cards), it may alternatively be possible to earn 150K Ultimate Rewards points on the same spend. If you would have transferred those points to Hyatt anyway, you are essentially forgoing 30K points in exchange for picking up 25 elite nights for $50K spend on the Hyatt business card. That could be an acceptable trade in some circumstances.

The 25 elite nights earned from $50K spend on the World of Hyatt Business Credit Card puts you most of the way to Explorist status (which requires 30 nights) and a Category 1-4 free night certificate (a 30-night milestone benefit). It isn’t a slam dunk, but I’m sure that will be worth it for some.

I don’t love the $199 annual fee. That is of course in large part because of the way that annual fee creep has infected the industry; it is becoming very expensive to carry all of the cards you might want. On the other hand, I would guess that most people who would spend enough on this card to make it worthwhile are likely also spending more than $50 twice a year at Hyatt hotels. If you are within the market for whom this card actually makes sense, it’ll likely feel more like a $99 card. Sort of. You can’t really value that $100 in credits as though it were worth $100 since, if given the opportunity to buy an annual subscription to such a thing, you wouldn’t pay $100 for two $50 Hyatt credits that expire in a year. You’d want a discount if you were going to lock up your money in advance. So the effective annual fee is more like $125 in my opinion since I value those credits around $75.

It seemed a bit odd to me that this card comes with neither an annual free night certificate nor the ability to spend toward one. When asked about that decision, a Chase representative basically said that Chase wasn’t looking to create a card that people would get and keep for the free night certificate and never use. They want people to use the card. While I would prefer free night certificates, I understand that perspective. Chase’s trend has clearly been toward bonusing ongoing use of their cards rather than giving you something that just makes you not want to cancel the card (in the form of a free night certificate).

In my opinion, the target market for this card has to be small business owners who spend plenty to hit the $50K mark early enough in the year to maximize the rebate on redemptions and who strongly value 25 elite nights (from that spend).

Folks who would naturally only hit around 35 nights per year and who can spend $50K on the card may also find it worthwhile for the milestone benefits that they will reach thanks to those elite night credits. In fact, from my perspective, the card becomes closer to a slam dunk for someone in that position. If you otherwise wouldn’t reach the 40, 50, and 60-night milestones, think about what you get by dedicating the spend on this card:

- $100 Hyatt credit or 5,000 points at 40 nights

- 2 suite upgrades at 50 nights

- 2 suite upgrades and a Category 1-7 free night certificate at 60 nights

- Globalist status at 60 nights (free breakfast or lounge access, free parking on award stays, waived resort fees, and more)

However, keep in mind that if you have the consumer card, the same $50K spend will still get you 20 elite nights from spend plus 5 annual elite nights from having the card (25 total elite nights) — the same net result and you’ll have a Category 1-4 free night certificate thanks to $15K spend on the card. The trade-off becomes these things:

- Category 1-4 free night certificate with $15K spend on the consumer card vs 10% back on redeemed points with the business card (after spending $50K in a calendar year and only until the end of that same calendar year and only up to 20K points back)

- Annual Category 1-4 free night certificate on the consumer card vs annual $100 credit on the business card (split into two $50 credits)

- $95 annual fee on the consumer card vs $199 on the business card

A direct comparison of the two shows that if it were a choice between the two cards, it would really depend on how much you value the 10% back on redeemed points.

However, for those looking to keep business and personal expenses separate, it isn’t necessarily an either/or situation. Having both cards could work out to be worthwhile for someone heavily invested in the Hyatt ecosystem. Imagine this scenario:

- Spend $15K per year on the consumer card to get a total of 11 elite nights (6 from spend + 5 annually from having the card) plus a Category 1-4 free night certificate from spend (and an anniversary free night certificate in subsequent years).

- Spend $50K on the business card for an additional 25 elite nights (plus the 10% back on redemptions)

- That’s 36 elite nights plus 1 Category 1-4 free night certificate from spend on the consumer card, 1 Category 1-4 free night certificate each anniversary on the consumer card, and 1 Category 1-4 free night certificate as a 30-night milestone benefit

Assuming you use all of the certificates in the same calendar year as earning the elite nights from both cards, that puts you at 39 nights — one shy of a 40-night milestone choice and just 20 more beyond that to Globalist status. If you value Hyatt and its benefits enough that you would consider dedicating $65K spend on Hyatt cards, I imagine you would likely be planning to spend at least that many nights in Hyatt hotels annually to reach the 60-night milestone benefits and Globalist status.

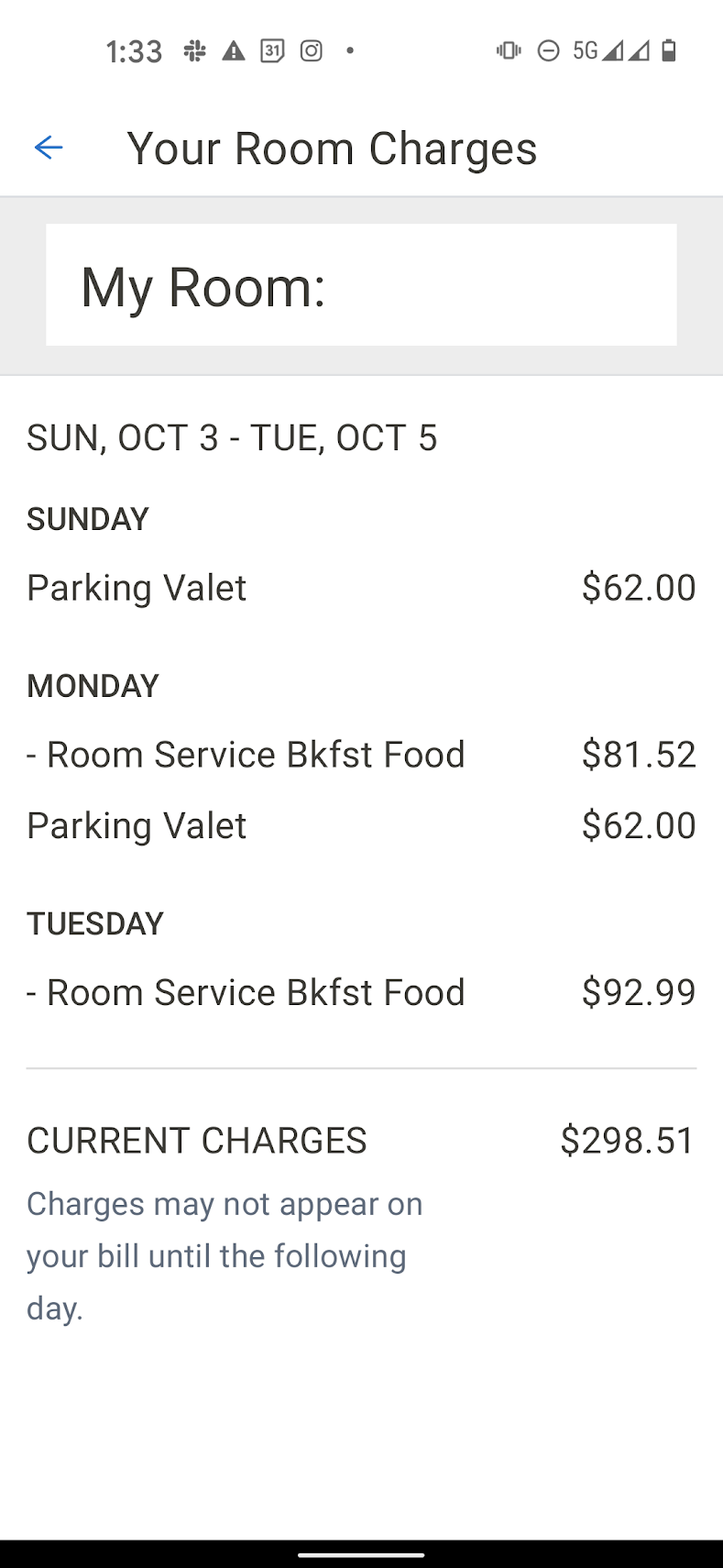

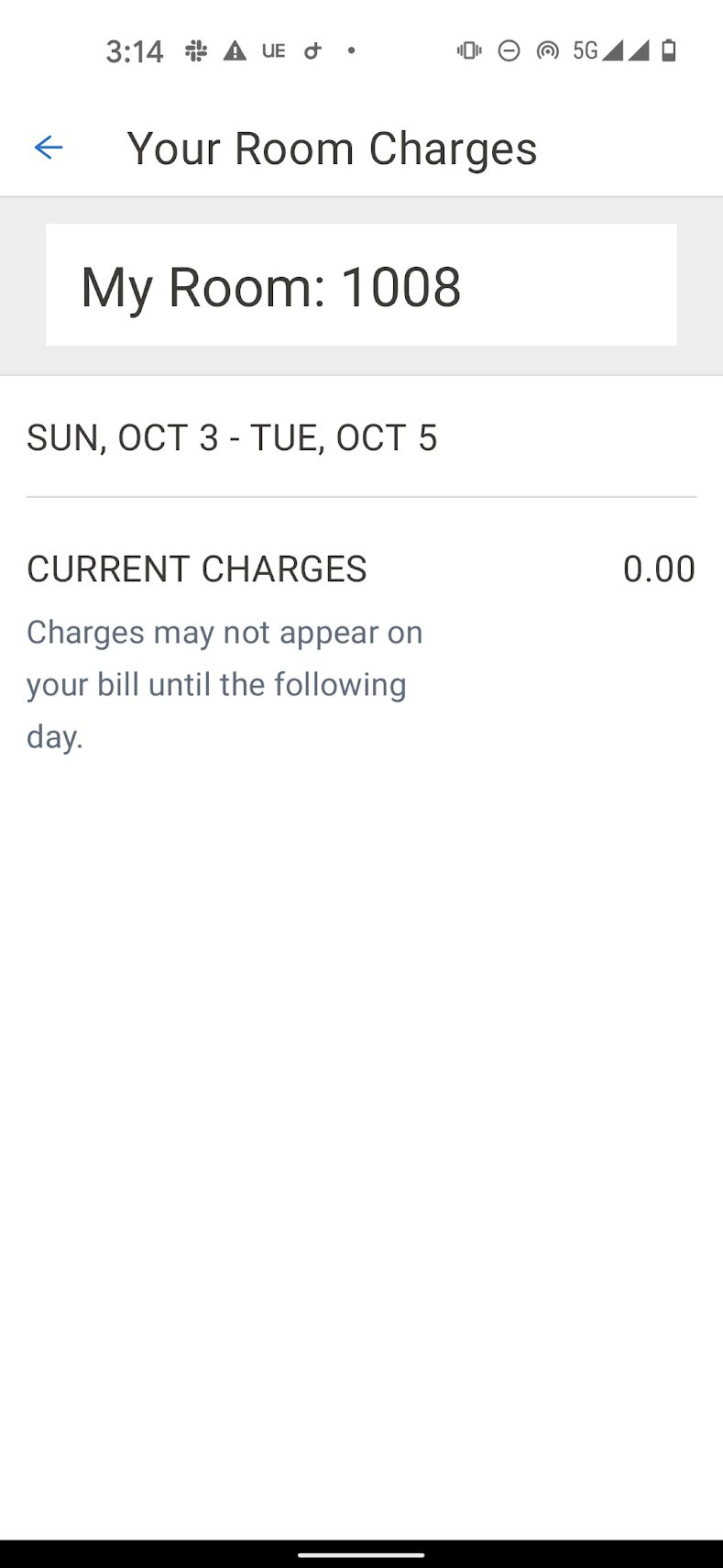

Again, this isn’t going to be for everyone, but I could see it making sense for some who really value Hyatt benefits. For example, I spent a two nights at the Andaz 5th Ave this week (an award stay using 25K points per night) and this is what my folio looked like before checking out for ancillary charges:

This is what it looked like after checkout:

Some will make enough use of benefits like free breakfast and parking on award stays to make the juice worth the squeeze.

Answers to questions

At the media event yesterday, we had the chance to ask some questions and to hear answers to questions posed by others in the room (and then we followed up with additional questions). Some valuable takeaways that are likely to answer common questions:

- Q: When does the 10% back on redemptions kick in?

- A: Immediately after $50K in purchases post to your card, but it can take up to 8 weeks to get the points back.

- Q: Do Guest of Honor stays booked for others get 10% back?

- A: Yes! After you reach $50K in purchases in a calendar year, you get 10% back on redemptions including points you redeem to book a Guest of Honor stay for others (if you have Globalist status).

- Q: Is there a cap on the 10% rebate?

- A:

No, there is no limit on how many points you will get back during your eligibility period.Update: We are now told that there is a cap of just 20,000 points back per calendar year. That is surprisingly low and changes the analysis significantly. - Q: Will stays booked before spending $50K but consumed after spending $50K get 10% back in points?

- A: Yes. You get 10% back on points redeemed for the rest of the year after spending $50K on purchases. Note that the 10% comes back after your stay, so your stay needs to be completed in the same calendar year that you reach $50K in purchases.

- Q: Materials introduce the “World of Hyatt Family” of cards. Will the family expand?

- A: When I asked about whether the family would expand to include additional cards, I was met with the answer that they were there to discuss the business card. Honestly, I didn’t get the sense that an additional card is planned in the near-term, but I’d be glad to be wrong.

- Q: Is the normal 50-night requirement for the Hyatt Leverage program waived for business cardholders?

- A: Yes. The Hyatt Leverage program is a small business discount program that we’ve written about before. It ordinarily requires crediting 50 nights per year in order to stay in the program but that requirement will be waived for World of Hyatt Business Credit Card holders.

Bottom line

The new World of Hyatt Business Credit Card isn’t the wildly compelling ultra-premium consumer card that some have hoped for, but it is a card that can make sense for those with high spend and a strong value for Hyatt elite nights. I’m not enthusiastic about the card’s annual fee or the fact that it leaves out annual perks like a free night certificate or automatic elite nights and I am disappointed in the surprisingly low cap of 20K points on the 10% rebate on redemptions, but I recognize that Chase’s aim here is to get people using the card as a go-to small business card. Those willing to put this card at the top of wallet for its spend benefits might find it to be a nice sweetener to accompany the consumer card in their wallets.

Might want to add *in a calendar year*. I JUST found that out the hard way, was working my way towards SUB planning on finishing it early next year. And then I found out that spending gets reset on January 1st…

That’s not true. The spend doesn’t reset for earning elite nights, but it does reset for earning a free night with $15K spedn.

Ah, thanks for the clarification.

The screenshot of your bill at Andaz 5th Avenue is a great reason to earn Globalist, but it doesn’t have anything to do with reasons to get this card. The only positive thing I can find here is the 70,000 point signup bonus for $199, then cancel after first year. This card is a dud.

I think the quest for Globalist is the main reason to get this card since you’ll earn elite nights a little bit quicker by combining this with the personal card. It’s not an MSers dream by any stretch. But 5 nights for $10K spend makes it a reasonable tool for those who already do $15K on the personal card and who need to continue to supplement elite nights to get to 60.

I obviously understand that someone who MSes two Ink Cash cards and does $50K at 5x has enough points for 50 Cat 1 nights. This card obviously doesn’t beat that, but clearly nobody at Chase is sitting in a room trying to decide how they can offer a better return than what MSers are currently getting. They’re trying to offer a card for the non-MSing small business crowd and I can see how this works for a narrow subset of that market. For the rest of us, it’s just another 75K bonus points. And that’s not a bad thing – for those who can get it, that’s 75K points that they can keep flexible as Ultimate Rewards.

Do I wish they’d have offered six annual Cat 1-7 certs and 10x grocery? Of course. I think from the post it’s obvious that I don’t find it very exciting but rather a tool for the belt for those who have enough spend to comfortably earn the extra elite nights. Again, no slam dunk of a card and I agree with someone above who said that it is disappointing that it requires so much analysis to decide if the card makes sense for you.

When I saw the headline, I was so glad that I did not apply for an Ink card yesterday. Now I wish I had applied for an Ink card. The Hyatt business card is just uninteresting. It is not even worth picking up for the bonus.

I hope they do a much better job designing the new Aeroplan card.

Not even worth picking up for the bonus? I disagree there. It’s another 75K Hyatt points available. Clearly that’s worth more than $199 and it doesn’t stop you from also getting an Ink card. I wouldn’t pick this over an Ink card if you’re not doing big spend for elite nights, but I’m happy about more Hyatt points

I am looking at the universe of Chase Business cards. I need to allocate my Chase Business card applications carefully during the window of time that I am under 5/24.

The no fee Ink cards offer 75k miles for $7.5 spend is a better offer. The United business card (no fee 1st year) is also better than the Hyatt business card. It offers less valuable United miles (75k miles) but you only need to spend 5k instead of the $7.5k spend on the Hyatt card.

The analysis would be different if I did not already hold the Hyatt personal card. The Hyatt business card is really only for those that are going for globalist using BIG spend. I think even at 50k spend you would be better off with the personal card.

Personal card – $50k spend, 20 elite nights (2 nights per $5k spend) + 5 elite nights (holding card) + Anniversary FNC + FNC ($15k spend)

Business card – $50k spend, 25 elite nights, 10% back on redeemed points (20k max)

Yeah unfortunately if we’re being honest, this card completely sucks.

I like how you spend all year trying to get to that 50K spend and then you have to rush to take trips in November and December (the least desirable times) to try and get a rebate on those points. They should have made that an Anniversary year.

Yeah, clearly they aren’t going after someone who takes all year to spend $50K. And they weren’t shy about that – in both the press release and at the event, they noted how, because of this year’s reduced path to elite status, a member could get Globalist status with just $60K spend by the end of the year. While I can appreciate that, it tells me that they aren’t expecting someone who takes 11 months to spend $50K to be the target for this card but rather a small business owner who might be spending more than that every quarter or every month.

You know what I dislike most about this card? The amount of analysis required to determine whether it’s worth it.

The earning is inferior or overlaps with other Chase UR or AmEx MR cards.

I also dislike that this card can’t be easily idled without incurring cost. When also holding the consumer card, it does not have a low “breakeven” threshold. It requires too much commitment in terms of spending. It requires too much commitment to redemptions and receiving elite benefits. It’s like a higher risk investment with modest returns.

While Hyatt generally treats its top-tier Globalists well, the outsized value is derived from room and suite upgrades. These are subject to availability and, potentially, the property owner’s discretion. While I appreciate the option, I generally am not a fan of spending on low earning categories to achieve status.

As a Globalist and holder of the consumer card, there are just too many opportunity costs of putting spend on this card. I understand Chase wants users to put spend on the card, but they’ve made it rewarding under such narrow circumstances.

Setting aside churners chasing the sign up bonus, I feel like the market for this card rather small.

Totally agreed that the market is narrow.

Yeah the opportunity costs kill it. You could be using Visa Gift Cards as your primary card and getting probably at least 200K in points a year conservatively. I’d rather keep my personal Hyatt and struggle to make Globalist every year than lose the point opportunity with the my Ink Plus.

Junk. No elite night credits included with the AF, no free night, no ability to earn FNC’s with spend, weak point earning, minimal hyatt focused benefits, af/benefits ratio is strongly negative, and even the statement credits are drip fed. Overall I think it sucks and that’s putting it kindly.

Any chance there was a nugget to be found on Q4 promo and/or 2022 status or was this strictly a plastic pimping event?

No, this was just a press event to release info about the card. There were Hyatt people there, but they were there with Chase to discuss the card. There was a question asked about whether the 10% back would stack with the typical summertime 25% back for cardholders and it sounded like it probably would, but the answer was a fairly general “we are likely going to continue offering good promotions” type of answer.

Major disappointment for this globalist — especially at that annual fee. I just don’t see how this would be better for me than the personal card and little incentive to have both. Hard pass.

That’s a lot of hoops to jump through. I put around 80K business spend on my personal Hyatt card each year and I’m pretty dubious. They just seem to have a lot of “Gotcha” restrictions.

Whoa…! If you don’t want it, then their already small market niche just got smaller still.

LOL. Thanks, I could use the laugh today.

I think for most of us this isn’t much of a game changer over the consumer card unless people are hoping to spend their way to status and so get a slightly better elite credit earning ability after $50,000 in spend. Or for people who value being able to give out Discoverist. Otherwise, the only redeeming feature that I really see is it not counting toward 5/24.

I don’t really see it as a this-over-that. If you want this card, I think it’s a this-and-that with the personal card. I agree in general it wouldn’t make sense to choose this one over the personal card.

For a certain group, I see that. My hunch is that for the core FM reader the most significant benefits overlap — spending for status nights. But if you have the ability to generate significant spend at gas stations (etc.), this is going to be good news, and you can get an extra 1x and also keep paying your $99 for your additional 5 nights and 1-4 certificate on the other card. And the 20k rebate is a decent little kicker. So, I get it. Then again, I wonder what the venn diagram looks like as between people who have tricks that allow large gas station spending and people who are under 5/24. :0)

Funny enough, the exact example that a Chase exec used with me was someone who owns a landscaping business who spends a lot on gas one quarter and a lot on advertising another quarter. I think they are looking for people who have started new businesses during the pandemic and who like Hyatt – which you don’t need to tell me is a niche within a niche – rather than the “business” crowd.

Just piling on with what seems to be a pretty negative reception.

The only advantage of this card is that you get 5 and not 4 nights per $10K spend. But that’s a downside, also, because failing to hit the exact milestone of increments of $10K is going to cost you the full 5 nights. On the consumer card you only lose 2 nights by missing the next spend milestone.

In all other ways you’d do better earning Chase UR points and transferring.

It’s really just for people who can easily spend $50K and get value out of the 25 elite nights and 10% rebate. Since the rebate is only up to 20K points, it’s definitely a narrow-use-case scenario.

But like in my situation I’m not going to spend 60 nights a year at Hyatt, but I do value Globalist benefits. I could see spending $65K to get myself 60% of the way there and I often do redeem at least 200K Hyatt points. Like I said, it’s a narrow group for whom it makes sense. I don’t disagree with you at all on that point. I think this card is worth it if you know you’re in that group.

One thing I totally left out and in hindsight deserved its own highlight is that the Ink cards and this card aren’t mutually exclusive. If you’re under 5/24, this gives you a shot at another 75K bonus and that isn’t a bad deal.

Again, I had big hopes when rumors started swirling about the luxury card until they gave us the press release and I read the details. Then I felt like I “got it” and their decisions made sense for them from a business perspective. It’s not an unreasonably bad card, it just isn’t at all what we all would have hoped.

Been waiting for Hyatt to come out with a business card, but man this is disappointing…

An annual fee card with no annual free nights, I am not sure what they are trying to do here. Hyatt cashback card?

Chase needs to step it up in terms of creating new products or at least try to get the attention of the customers like Amex is doing with all their huge SUB

Seems like Amex is getting all the press these days.

Great write up and breakdown Nick! Thank you!

This was a letdown IMO. I understand what Chase is attempting, but it falls quite short of enticing me.

That’s the thing. I “get it”, but I’m not excited. I had hoped to be excited.