NOTICE: This post references card features that have changed, expired, or are not currently available

The American Express® Green Card has been completely revamped. Previously it was a nearly useless $95 per year card. Now, at a $150 per year, it is a serious Chase Sapphire Reserve competitor with 3X rewards for travel and dining. This post has been updated since the Sapphire Reserve card’s annual fee has increased but, in my opinion, the Green card still falls short in a head to head comparison.

Let’s compare the Green from Amex to the Chase Sapphire Reserve side by side:

| Green from Amex | Chase Sapphire Reserve |

|---|---|

| $150 Annual Fee | $550 Annual Fee – $300 Travel Reimbursement = $250 Net |

| No FX fees | No FX fees |

| Earns 3X travel & dining | Earns 3X travel & dining |

| $100 Annual Lounge Buddy Credit | Priority Pass Membership |

| $100 Annual CLEAR Credit | $100 Global Entry Credit every 4 years |

| N/A | Lyft & DoorDash Benefits |

| Minimal Travel Protections | Best In Class Travel Protections (found here) |

Let’s look at each of these in turn:

Annual Fee (Advantage: Amex)

Thanks to the Sapphire Reserve card’s awesome travel protections, I personally put most travel spend on this card. As a result, every year I automatically earn the $300 Travel Reimbursement in the same statement cycle as the annual fee. So, for me, the net annual fee for the Sapphire Reserve really is just $250 ($550 annual fee minus $300 travel credit). There is, though, a tiny loss due to the fact that I don’t earn rewards on the $300 of spend that was rebated.

All that said, the Green card has two big advantages: 1) it’s $100 cheaper; and 2) You don’t have to pay $550 up front. You don’t need to make sure to spend $300 on travel in order to bring the net annual fee down to $250.

Foreign Transactions (Advantage: Chase)

Both cards have no foreign transaction fees, but Visa cards are accepted in far more places worldwide than Amex.

Rewards (Advantage Depends on Circumstances)

Both cards earn 3X for travel and dining and 1X everywhere else. So the real difference in rewards value depends upon how much you value Amex Membership Rewards vs. Chase Ultimate Rewards. If you want to cash out your rewards, then Amex has the edge, but only if you have the Schwab Platinum card which lets you cash out points at 1.25 cents each. If you want to use points to pay for travel, then Chase has a big advantage with points worth 1.5 cents each towards travel booked through Chase. If you want to transfer points to airline partners, then Amex has the edge since they have more transfer partners and frequent transfer bonuses. If you want to transfer points to hotels, then Chase has the edge because they support transfers to Hyatt (which has a generous award chart).

See our guides for more information:

Airport Lounge Access (Advantage: Chase in a vacuum, Amex otherwise)

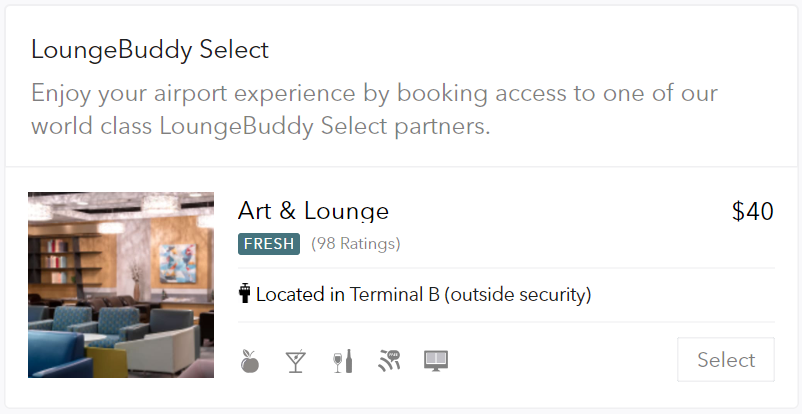

Chase Sapphire Reserve cardholders get full Priority Pass membership. This allows you to freely visit any Priority Pass lounge or restaurant with up to 2 guests. The Green card, meanwhile, gives you only $100 per year of Lounge Buddy credit. Lounge Buddy is a very useful app for finding out about which lounges are available at every airport worldwide. Lounge Buddy also lets you pay for access to some airport lounges. Unfortunately, their selection is even more limited than Priority Pass. Here’s an example…

At Newark airport (EWR), Lounge Buddy offers only one lounge for sale. The Art & Lounge outside of security in Terminal B is available for $40. If you used the Green benefit to get yourself and one guest in to this lounge, you’d use up $80 of your annual $100 benefit with just one visit.

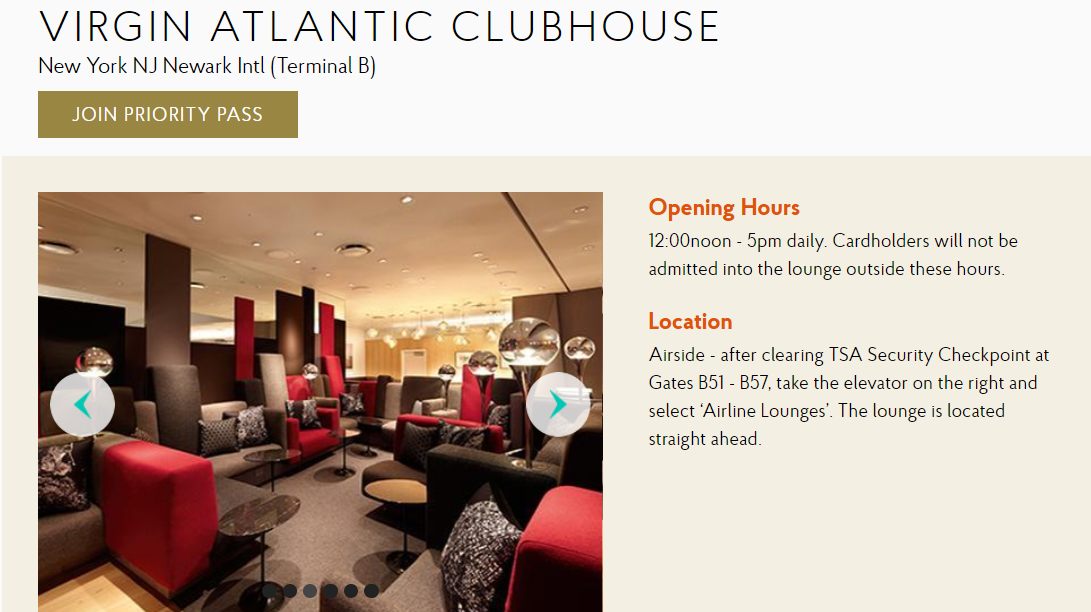

Priority Pass, meanwhile, offers access both to Art & Lounge and the Virgin Atlantic Clubhouse at Newark’s terminal B. It is important to note that access times are limited for Priority Pass cardholders at this lounge, but if the times meet your needs, this is a fantastic option. And, not only could you bring in 2 guests, but you could visit every time you travel without using up this benefit.

There are times where a Priority Pass lounge may turn you away for various reasons. They may have a rule about access being limited to 3 hours before you flight, or they may only allow access during certain hours, or they may turn you away if the lounge is full. The one advantage that I can think of to buying lounge access through Lounge Buddy is that it is a way to secure access to lounges that might otherwise turn you away.

In a vacuum, the Sapphire Reserve’s Priority Pass benefit is arguably much better than the Green card’s Lounge Buddy credit. However, if you already have a good version of Priority Pass from another card, there is more incremental value to the Lounge Buddy credit since there are times (although rare) where it is better than Priority Pass alone.

Airport Security Benefits (Advantage: Amex)

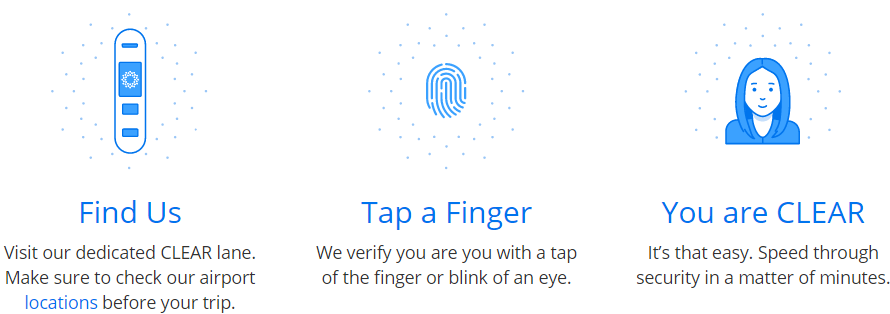

Thanks to my Delta Diamond status, I get CLEAR for free. CLEAR lets me skip the sometimes very long ID check lines at the airport (just before security). Instead, I look into the camera and CLEAR verifies my identity based on my eyes (you can use your fingerprints instead if you don’t mind touching the same germ infected touch pad that everyone else uses).

I also have Global Entry for free thanks to many cards that offer that perk. Global Entry gives you expedited clearance back into the country when traveling internationally. Even more valuable to many, Global Entry gives you TSA PreCheck. This lets you go through special PreCheck security lines at the airport and means that you don’t need to remove your shoes, laptops, or liquids.

The main difference between CLEAR and TSA PreCheck is that CLEAR lets you breeze past the first line at security: the place you line up to show your ID. TSA PreCheck then speeds up the second part where you put your bags through x-ray machines and you go through a metal detector or body scanner. The best is to have both so that you can zoom through both parts of security every time.

Global Entry costs $100 every 5 years. So, at best, the Global Entry fee reimbursement is worth $20 per year. Meanwhile, the Green card’s CLEAR benefit is worth up to $100 per year.

By default, CLEAR costs $179 per year, but there are easy ways to reduce the price. See: 5 ways to get CLEAR for less. If you were going to pay for CLEAR anyway, the CLEAR benefit brings the Green card’s net annual fee down to just $50.

Travel protections (Advantage: Chase)

The Chase Sapphire Reserve card offers awesome travel protections. Check out this post for a comparison with other ultra-premium cards. The Sapphire Reserve covers all of the following:

- Primary car rental collision damage waiver

- Baggage insurance

- Roadside assistance

- Trip cancellation & interruption insurance

- Trip delay insurance

- Travel accident insurance

- Emergency evacuation & transportation

- Emergency medical & dental

Meanwhile, the Green card has minimal protections:

- Secondary car rental collision damage waiver

- Baggage insurance

Summary

| Green from Amex | Chase Sapphire Reserve |

|---|---|

| $150 Annual Fee (Advantage Amex) | $550 Annual Fee – $300 Travel Reimbursement = $250 Net |

| No FX fees | No FX fees (Advantage Chase for worldwide acceptance) |

| Earns 3X travel & dining (Advantage Amex for transfer partners) |

Earns 3X travel & dining (Advantage Chase for purchasing travel at 1.5 cents per point value) |

| $100 Annual Lounge Buddy Credit (Advantage Amex for those with Priority Pass from other cards) |

Priority Pass Membership (Advantage Chase for those without Priority Pass) |

| $100 Annual CLEAR Credit (Advantage Amex) | $100 Global Entry Credit every 4 years |

| N/A | Lyft & DoorDash Benefits (Advantage Chase) |

| Minimal Travel Protections | Best In Class Travel Protections (Advantage Chase) |

Conclusion

In an earlier version of this post, I concluded that the Sapphire Reserve was the hands down winner. Since then, Chase has increased the annual fee from $450 to $550. I’ve also added consideration for the possibility of using the Amex card in conjunction with other cards. Now, I’m led to multiple conclusions:

Chase Sapphire Reserve is the clear winner in a vacuum. If you don’t have another card with no foreign transaction fees that is accepted worldwide, and if you don’t have another card that offers a good version of Priority Pass, and if you don’t have another card that offers great travel protections, then the Chase Sapphire Reserve is a much better option even with its higher annual fee.

Chase Sapphire Reserve is the winner if you want to use points to book paid travel. If you’re only interested in transferring points to travel partners, then Amex or Chase may be preferred depending upon which travel partners you’re most likely to transfer to. However, if you’re interested in booking paid travel with points, the Sapphire Reserve is far superior in that it offers 1.5 cents per point value for travel booked through Chase Travel℠. Amex only offers 1 cent per point value in most situations.

Amex is the winner as an “add on” card, especially if you pay for CLEAR anyway. If you subscribe to CLEAR (or plan to), then the Green card’s net annual fee is only $50. Depending upon what other cards you have, it may be well worth $50 to get 3X travel & dining and $100 Lounge Buddy credit each year.

Comparing to other cards

This post was specifically designed to compare the Amex Green Card to the Chase Sapphire Reserve. If you’re interested in looking more broadly at which cards are worth their annual fees, please see: Which Ultra Premium Cards are Keepers?

Chase Sapphire Reserve® cardholders can get a free year of WHOOP (fitness wearable)")

With respect to Foreign Transaction it should also be noted the VISA exchange rate is also better than that of Amex which relies on OANDA rates, which are always worst than that of VISA, i.e. you buy a shirt in ZARA in Spain in Euros, it will cost you more with AMex than with VISA

Hmm, I suppose the green card works for those with lots of non-airfare travel spend, but I think the gold card makes it irrelevant for most people.

I’m consistently disappointed with Amex’s crazy MR rules. We opened the green amex and were planning on switching from the CSR to Green card. Anyway, my spouse opened the account and added me as an AU at the time the account was opened. Two and a half months into having and heavily using the amex green card, we needed to top off my Hawaiian airlines account with 15k points to book two one-way first class level 1 awards. My spouse has no Hawaiian airline FF or miles with them. Anyway, Amex refused to allow any transfer to my Hawaiian account because I haven’t been an AU on the Green card for 90 days. They refused to make an exception, given that I was on the account at the time of opening, and we both have had Amex cards for the past 15 years…. Typical Amex BS. Needless to say, we ended up having to transfer 40k MR instead of 15k to my spouses new Hawaiian FF account. I’m done with Amex, they can keep their Green card and customer unfriendly MR points.

[…] Miler compares the American Express Green Card head-to-head with Chase’s Sapphire Reserve, which is heady […]

[…] Miler compares the American Express Green Card head-to-head with Chase’s Sapphire Reserve, which is heady […]

Good article. The one thing I want to add is that starting in January the Green card will also provide trip delay insurance up to $300 for trips delayed more than 12 hours.

I’m a little shocked that nowhere in the article or the comments is it mentioned that CSR is 1.5 cpp for travel vs Green being 1 cpp (unless you also have a Biz Plat, which has limited 1.54cpp usability). That makes the CSR the clearly better card to me — the flexibility is outstanding. I’m well aware that airline transfers are how you get outsized value, but there are plenty of situational cases where paying with points is the better play. The ease of family pooling UR points also gives the CSR an edge.

Both cards earn similar earnings rates with the same relative ease, but AMEX points are optimally used towards air travel & URs towards hotels & car rentals. They work hand-in-hand, not mutually exclusive.

Yeah, good point. I forgot to mention how they are different when using points to book paid travel.

Wait, why are some of you paying a 2nd AMEX annual fee for a non-keeper card? I thought you just couldn’t cancel within the first 12 months. So if you get 30 days grace period to cancel and get the annual fee removed, why don’t you just cancel at 12 months + 30 days from application date and not have any reason to fear the RAT?

Wife had a personal Gold from back in Jan of this yr, about 9 months ago & got signup bonus. Will she be eligible for Green signup bonus? I seem to recall only 1 signup among the ‘family’, Plat, Gold, Green.

You remember incorrectly. You can get 1 welcome offer per product — 1 Green, 1 Gold, 1 Amex Platinum (vanilla), 1 Schwab Platinum, 1 Morgan Stanley Platinum, etc. She’s definitely eligible for this if she hasn’t had the Green before.

thanks! glad to be on the wrong side of it

How does the definition of ‘travel’ compare between CSR and Amex? I know that for CSR that definition is quite broad – it even includes things like tolls, etc. I also remember when Amex Gold added 4x on dining, there were a lot of issues with restaurants coding correctly. Any thoughts on this?

Travel on Amex Green only credits if you book it through their portal (amextravel.com). You have to read the terms and conditions to find that little caveat, which I think should be a major strike against the Amex Green.

Not anymore. That changed today – now it’s airfare, hotels, taxis, and rideshares (couldn’t book taxis and rideshares via Amex Travel even if you wanted to).

Important to me (& likely others), AMEX GC still doesn’t award travel points towards timeshares, Chase does.

Regardless, I like this one as well, Nick. Got an instant approval even with 5 AMEX credit cards, so this is def treated like a charge card.

Also when I googled the card, the 45k was offered as long as I applied immediately & didn’t leave the website. No incognito mode necessary.

Pam

U got it so it must be good and I got the same deal..

CHEERs

Lolol, that’s great CD! Easy & attractive points/benies now + a (likely) flexible path to future card options. I just returned from NYC & wanted to use my Barneys acct – the sales rep looked it up & found out it had just been canceled from non-use after 31 months.

A 15-yr old acct history just closed on me! I sign up for cards now I can ALSO envision staying out of the sock drawer/cancelation for non-use. Maintaining a 7 yr avg acct history on my credit report sure helps compensate for all the new accts opened, I’ve found!

Pam

Don’t do this in your Home !!!

I have printed sheets Nailed on the wall with my Cards & Travel data .Like Ath>Mykonos>Naxos>Santorini>Chania>.ATH in Hotel planing stage .

I bet Barney’s will send u $$$ to reopen ur account and I’m surprise the rep was a Fool.

CHEERs

Good tips, thanks CD. Reopening that acct woulda required a hard pull they said & with their (yet again!) tenuous financial position it may have been closed again in the near future anyway.

And, too, I have been waiting since Sept for this new GC to launch. I like to always stay under 5/24 for amazing Chase deals & if I’d caved at Barneys, AMEX woulda put me over for awhile, thx again!

(5x Freedom this qtr at dpt stores mo betta anyways!)

airfare – does that include points purchase directly from airlines? sure hope so

I think it’s important to note also that CSR is one of basically three cards left standing (with Prestige and Altitude) that still offer restaurant access with their Priority Pass membership. Many don’t need this, but for those that do (i.e. me, with a family of three that uses DCA every few weeks) it’s basically an $84 meal benefit every time we board OR get off a flight. And the fact that Amex cards no longer allow restaurant access means that tables have been much easier to find lately 🙂

tim

P-pass thanks for POINTING that (restaurants) out had like 5xsolo so far this year ..Will no one help the poor get a good restaurant meal for FREE ?

CHEERs

To me, the differences boil down to:

1) I may never be able to apply for the CSR due to 5/24

2) The AMEX Green travel protections are a joke

3) I’ll gladly take 45,000 AMEX MR for a $150 fee and $2,000 spend any day!

Gene, go incognito mode and the offer is 45,000 MR’s(after $2k spend), $100 CLEAR AND $100 statement credit. I’m no math wizard but that’s 45,000 points for $50 AT WORST. App dropped, instant approval.

@ geoff — Oh yeah, I forgot that part. Even better! Of course, thanks to RAT, I now always pay the second annual fee, so I guess the cost is something like $200 for 45,000 plus any retention bonus, which I’m betting will be 10,000 points for $1,500 or so spending.

I got approved this afternoon, when prompted I asked for my number now so I can immediately use the card and there was some kind of a technical difficulty and I got a popup that says i’m getting another $60 credit to make up for that inconvenience. So a pretty good little afternoon overall.

I cringe when I read that CSR has a “net $150 AF”. At least you do caveat it, but aside from the risk of your life changing and not being able to use the travel credit, and the opportunity cost of 900UR minimum, there is also the fact that you are prepaying, and thus giving Chase an interest free loan.

It does look like Amex is positioning it as a poor man’s CSR, for those who are put off by high AFs. I do think though for those of us who already have a card with PP and GE, these benefits are very complementary. I like the example of using the LB credit for off hours PP, but I wonder if there are any other uses for those who already have PP. I assume you can’t use it to get into Centurion?

On the other hand, I shrug my shoulders when people say Chase is getting a free loan. Just like Greg, I always spend $300 on travel before that statement cycle closes. Chase doesn’t get a loan — the money ends up being credited during that first statement cycle before I’ve paid the AF. Of course one’s life situation could change — but that statement could apply to literally anything in your life. You probably won’t avoid buying a car because you might get a job within walking distance someday or avoid buying groceries because you may not be hungry for lunch tomorrow. If my situation changes such that I’m no longer spending $300 on travel each year, I’ll certainly be prepared to cancel. And I’m sure that not all readers spend $300 on travel regularly (I’m also sure that many do). But then, if you don’t pretty regularly spend money on travel, I’d wonder why you were considering keeping an ultra-premium rewards card that primarily rewards travel spend in the first place.

I’ll therefore say that I can understand why you wouldn’t personally consider the CSR a “net $150 fee” if you don’t regularly spend much on travel, but then I’d wonder why you were considering keeping it. I’d think (hope?) that most people who consider keeping it know that they spend far more than $300 per year on travel. Keep in mind that you don’t need to spend $300 on your own travel — you need to spend it on anyone’s travel.

All that said, I disagree with Greg. I think this Green card may be a hit, but I’ll save that argument for our weekly chat.

The vast majority of CSR cardholders are not able to burn $300 before the AF posts. You are an outlier. I travel every 2-3 months, but considering it’s almost always using points, there’s no guarantee I would even be able to burn the credit within 6 months, so the need to burn a CSR credit might lead me to pass up a good point option just to use up the credit.

The grocery or car analogy is a miss. You can sell a car, you’re not stuck with it, and you don’t need to prepay for groceries for a year. There is no risk in buying weekly groceries, except spoilage, but that’s entirely controllable.

Bottom line is it’s not net $150 AF. The value of 900 UR, the (generally) need to pay upfront for benefits later, and the risk of not using it, or passing up better options just to use it, are worth something. If I were to offer you an annual $300 travel credit as a standalone benefit, you would be a fool to pay $300 upfront. Maybe you discount it less than me, but personally I would value it at about 90% of face value.

If you struggle to spend $300 on travel in 6 months time, I think you should reconsider why you have a credit card that offers 3x on travel — it clearly doesn’t match your spending patterns and likely isn’t a keeper for you any more than a card that bonuses grocery spend would be a good choice for a vegan who maintains his/her own garden and grows most of their own food. I’d argue that it’s not even worth holding the Sapphire Preferred (nevermind the Reserve) if you spend that little on travel; you should be looking for a card that bonuses the things on which you spend money (or only considering a card like the CSR for the welcome bonus). I definitely won’t argue that you shouldn’t think of it as a net $150 if you spend so little on travel, but I hope that most people who consider keeping the card beyond year 1 spend a lot more than $300 on travel. I think I’m less of an outlier than you think in terms of travel spend as I meet plenty of people who buy cash business class tickets and pay for expensive hotels (things I don’t generally do but many others do), etc (not to mention the great many people who have a job that reimburses their travel).

To be clear, I understand that the CSR doesn’t make sense for everyone. Not every card makes sense for every person. For example, I’m not terribly interested in cards that offer bonus points for gas station spend because my wife and I both work from home and might go days without getting in the car (and none of my local gas stations sell VGCs). I don’t spend all that much on gas, so it’s not a huge motivator for me. Neither are fuel points since my local grocery store doesn’t offer them and I wouldn’t use them every month. I don’t value Global Entry reimbursement since I have so many cards that reimburse it (and I haven’t used it on any of them). I therefore wouldn’t pick up or keep a card where that was a crucial benefit any more than you should keep the CSR if the $300 travel credit isn’t fairly automatic for you.

In regards to your dismissal of my argument regarding the car or groceries, I’d note that just like you can sell the car (for less than you paid for it), you could easily buy airline gift cards or hotel gift cards with your $300 credit (and sell them for less than you paid). I don’t want to make this response about that particular example, but my point is that if the argument is that your life situation could change and maybe someday you won’t spend money on travel, that argument could be applied to any purchase you make. Obviously you have to decide which ones you think make sense for you.

All that is to say that you personally certainly don’t need to consider the CSR to have a “net” $150 fee, but I think there are a lot of people out there who can and do. In fact, if you Google statistics, the average family of 4 spends several thousand dollars on vacation every year. I think that out of the market of people who would consider the CSR, those spending less than $300 every six months on travel would likely be the outliers by a huge huge margin.

I won’t get in to specifics about why I have the CSR, I know what I’m doing, and I’m getting more than I’m paying in value for sure, but I certainly don’t plan to keep it. I’ll downgrade to CF after AF posts.

But it’s really beside the point. Prepaying for something, even if you are certain to eventually use it, comes at a cost. The entire banking industry is built on that premise. Losing 900 UR on that spend is also a cost (about $15 at 1.6 cpp). That right there says the $300 travel credit is really only worth at most $285. I’m not saying you need to discount the value as much as I do, but if you value it at any more than ~$285 then you are being intellectually dishonest. So call it $165 net AF at least.

I agree. With how generously CSR applies the travel credit (and automatically unlike the RItz carlton card) to ALL travel, not just bag fees/lounge/inflight wifi etc – even to Uber rides and parking, the past few years, my next years credit gets consumed before even the year ends (because Chase automatically start crediting it after the last monthly statement of the year closes, so technically for expenses not in the next calendar year). If one doesn’t travel a lot, I’d question why even look at both these cards with a significant AF, like you said, @Nick Reyes Reyes.

Hi Nick, while like Greg, I probably won’t be going for this card myself, here’s a couple more points to add to your argument with Greg on why this could be a hit 🙂

– To my knowledge this is the only mainstream card with CLEAR credit. As someone who has paid for CLEAR in past years (I’m a last-minute, running late kinda guy with several airports and a ballpark near me which accepts CLEAR so totally worth it for me), with several other cards that offer Global Entry / TSA-Pre credit, I can see why this benefit could be attractive.

– CLEAR is getting more coverage in non-airport locations, and recently with Hertz (for Gold Club members). Still have to work out the kinks but as a service, it is getting more useful. For me as a user for many years, its a nice expansion of benefits. (@Greg, they also just added facial recognition instead of “looking into the scanner” with irises, and of course fingerprints). Not trying to be a shill for CLEAR because, yes, you give up a lot of private data and biometrics but that can be a different debate (and also a note of caution to those thinking about this – unlike Global entry, this info goes to a private company, so do your due diligence before you sign up).

– And as Greg himself pointed out – with the CLEAR credit being annual instead of every 4 years for CSR Global Entry, if you are using it, it can be quite valuable.

So while it may not win the CSR v/s Amex Green debate for some people it could be a second card to add on (still a hit). For a paying CLEAR user, if you think of it as you would a hypothetical Amex co-brand card with subsidized CLEAR membership included and with 3x MR points in addition and to many it would make sense to go for this.

I’m not going for it personally, since the United 1K gives me the CLEAR free for now so I am not able to leverage the perk even after touting it above 🙂

Foreign transaction should award to Amex Green since Amex cards won’t get DCC.

One $100 use for CLEAR, one, perhaps two, lounge visit(s) and 45,000 MR’s for $150? Sure.