NOTICE: This post references card features that have changed, expired, or are not currently available

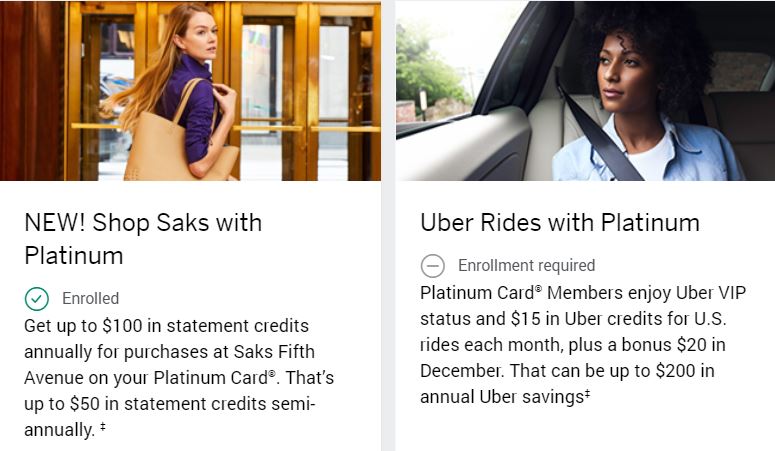

In March 2017, Amex increased the annual fee on consumer Platinum cards from $450 to $550. To some, the net change was positive because Amex also threw in up to $200 per year in Uber credits (See: Amex drives in wrong direction with Uber). Those credits are doled out monthly: $15 per month January through November, and $35 in December. If you don’t use your credits in any given month, the credits do not carry forward.

More recently, Amex added a similar perk to their consumer Platinum cards: Up to $100 per year in Saks Fifth Avenue credit. In this case, the benefit kicks in only if you register for it, and it is doled out in 6 month chunks: $50 January through June + $50 July through December.

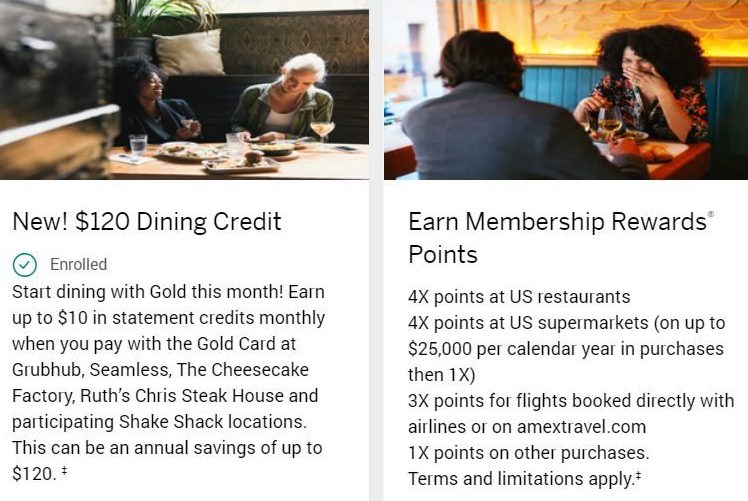

And now we’ve learned that Amex’s Premier Rewards Gold card will soon be rebranded, and will include new and awesome category bonuses for spend, and will include $10 per month “dining” credit towards a specific list of food delivery services and restaurants: Grubhub, Seamless, The Cheesecake Factory, Ruth’s Chris Steak House, and participating Shake Shack locations.

Why this is brilliant

For years, many credit cards have offered annual perks. Credit cards branded by Southwest, JetBlue, Radisson, and others offer bonus points each year when you renew. A number of hotel branded cards offer a free night certificate. Certain United cards offer United Club Lounge passes. Some Delta cards and Alaska cards offer companion tickets. All of these are offered once per year, upon renewal, and are tied specifically to the co-brand. And, in all of these cases, you have a full year to use the benefit before its value is lost.

Non-cobranded cards often offer annual perks that are not tied to any brands. The Chase Sapphire Reserve card, for example, offers $300 in travel reimbursements each year. Similarly, the US Bank Altitude Reserve offers $325 in in travel credits per year. And, Amex Platinum cards offer $200 in airline fee credits per year (but only for the one airline you select as your preferred airline).

Amex’s monthly bonuses are different (I realize that the Saks benefit isn’t really monthly (it’s “half-yearly”), but I’m going to lump it in with the Uber credits and dining credits as if it is monthly to simplify the conversation…). These bonuses are brand-specific, and doled out in dribs and drabs…

Brand specific bonuses…

The Amex cards that offer monthly bonuses aren’t tied to particular brands, but the monthly bonuses are. What that means (my speculation): The brands pay for these benefits. I can’t think of any other rational explanation for why Amex would pick these specific brands (Uber, Saks, The Cheesecake Factory, etc.). It’s possible that the brands directly pay the credits as they happen, but I think it’s more likely that the brands pay set marketing fees to Amex and then Amex pays the credits. Many other payment structures are possible, but the point here is that Amex has found a way to provide perceived valuable benefits at little or no cost to themselves.

Dribs and drabs…

I doubt any of Amex’s customers like the fact that these benefits are doled out in small monthly bits, but for Amex and the brands involved it makes a lot of sense. The brands want repeat customers. The benefit structures encourage that. When choosing between various food delivery services, a customer who gets $10 monthly credit will most likely use GrubHub or Seamless every time, even if they order more than once a month. Similarly, Amex Platinum cardholders will most likely get used to choosing Uber over Lyft, even if they’ve already used up their monthly credit.

The monthly nature of the benefits makes it likely that most Amex customers won’t get full value from each of these benefits. But, they most likely will get some benefit. This is important at credit card renewal time. Psychologically, a cardmember who received some benefit will probably be more inclined to keep the card than one who missed out on a key benefit entirely. In other words, I think this means that Amex will be able to retain a lot of customers based on how they perceive the benefit (e.g. $120 per year!) rather than how much they actually saved in the past.

More to come?

If I’m right that the brands are paying for some or all of the expense of providing these benefits, then it seems extremely likely to me that we’ll see more of these benefits going forward. I expect that Amex requires a multi-year commitment from each brand before they’ll go through the expense of updating a product’s benefit structure. So, I don’t think we’ll see a slew of these benefits appear overnight, but I do think they’re coming.

My guess is that we’ll see something happen with either Amex Business Platinum cards or Amex Business Gold Rewards cards (or both). For example, I wouldn’t be surprised to see monthly credits with AT&T business internet, or maybe with an office supply store like Staples.

So far we’ve only seen these offers on high end cards, but I do think it’s possible that some brands will want to target everyday cards. And, here I literally mean the no-fee Amex Everyday or the Amex Everyday Preferred. Which big brands are most eager to attract Amex’s every day customers? Sams Club, perhaps? Or maybe a gas station chain? Or clothing stores? Time will tell.

What this means to Frequent Miler readers

Just as we’ve learned how to get full value from airline fee credits (see: Amex Airline Fee Reimbursements. What still works?), we will learn how to get maximum value from the new monthly credits. I expect that many readers will earn these credits in non-standard ways. Here are some examples:

- Uber: Order food from Uber Eats once a month if you don’t use Uber directly for rides.

- Saks: When you find yourself near a Saks store, pop in to buy a $50 gift card if you don’t have immediate shopping needs (I recommend doing this in-store because the minimum gift card amount online is $150). If you don’t have any desire to shop at Saks ever, you should be able to resell the gift card for about 80% of its value (e.g. Sell a $50 card for $40).

- Dining credits: Personally I don’t expect to have any problem using the $10 credit every month via GrubHub deliveries or by stopping into Ruths Chris steakhouse for an occasional happy hour. Otherwise, I’d want to pop into one of the supported restaurants once per month to see if I could buy a $10 gift card. It looks like online gift card orders won’t work because they are either handled by Cashstar or they have higher than $10 minimums.

Above are just a few examples. Other methods have been found and will be found to get more value from these benefits. A great place to discuss these ideas is in our Frequent Miler Insiders Facebook Group. If you’re not already a member, consider joining!

When annual fees come due for credit cards you should always evaluate the benefits you get from the card vs. the annual fee. Ideally the benefits are worth significantly more than the annual fee. That’s when you’re getting a good deal. Otherwise, I recommend either cancelling the card or downgrading to a low-fee or no-fee card.

When evaluating benefits like the ones described above, I recommend assessing not their total dollar value, but rather the amount you would be willing to pay for a subscription. For example, if Uber offered you a chance to pay a subscription to get $15 off per month (and $35 off each December), how much would you be willing to pay annually for that subscription? Obviously you wouldn’t pay $200 per year, but maybe if you knew that you would definitely spend at least that much per month anyway then you’d be willing to pay $150 or $175. Those who don’t expect to use the service every month should come up with a much lower number.

Summary

Amex appears to have come up with a great way to offer value to customers at little expense to themselves. This is great for them because it gives them a way to compete more effectively with other card issuers without hurting profits. And, it’s great for cardholders who can benefit from these perks. Not all of these perks will be meaningful to everyone, but when there’s a good fit I think that everyone will be happy: credit card customers, Amex, and the brands who support these offers.

")

")

[…] (yet) offered similar annual or monthly rebates for the Business Gold card. In my post “Amex’s brilliant move toward monthly bonuses. Will it be enough to counter Chase?” I specifically predicted that Amex would bring this type of benefit to the Business Gold […]

Amercian Express Credit are not working on the Uber app. There seems to be a major problem this month with Uber’s software.

Ah yes, AmEx continues to let Chase eat its lunch. What do I care about a credit at Saks? Ridiculous.

If I don’t use UBER but my daughter does, is there a way to get the credits from her usage? I did link her to the “family” feature on UBER, but I know yet if that will work.

Yes, just put your Amex Plat card in on her Uber account. I do this (my card) on my wife’s Uber account.

Thanks, Biggie F. for answering. Just did it, so we will see. If that does work, you helped me immensely.

Thanks again.

I agree that the “monthly” food credits are too much hassle for what’s basically $10 off. If they are going to make their card worthwhile, why not just give me the whole $120 so I can, you know actually GET dinner at Ruth’s Chris or Cheesecake factory?.

Same with the Uber credits on my Plat – why can’t I use it when I want to instead of piecemeal? These are not compelling reasons to spend $195 or $550 a year, and far from “brilliant” ideas.

Because there are people who use the credit, cancel the card and get the annual fee refunded.

Assholes screw it up for everyone, not just themselves. Which is why if you are not an asshole you should snitch on assholes because they are effectively stealing from you.

There’s an easy solution for that: don’t refund the annual fee.

I think there is a law that says you have to refund within one month. I bet people being denied bonuses are the ones who pulled these shenanigans. But who knows.

Because, as pointed out, that makes the perk too expensive for amex. They COUNT on most people only using the credits some months.

The restaurant thing blows chunks. “Personally I don’t expect to have any problem using the $10 credit every month via GrubHub deliveries or by stopping into Ruths Chris steakhouse for an occasional happy hour. Otherwise, I’d want to pop into one of the supported restaurants once per month to see if I could buy a $10 gift card.”

Must be nice to have those services or places where you live. (In caps for emphasis) BECAUSE THOSE THAT DON’T HAVE NO USE FOR THIS DEAL!

This sucks like the Uber thing. I hardly have need of Uber for a ride. But when I do, it’s way more than $15. Amex should let me carry over the credit if they are going to bally-hoo the “$200” Uber credit in advertising. LEMME USE THE FULL $200! I also don’t trust some gooberhead to bring me food and have it be right. I trust the local Chinese or pizza guys to get it right because it is their business. The Uber driver? He doesn’t care if it is hot or anything.

The Saks thing is actually decent. Used it the first day I had it for a Birthday Present. It will supply a Xmas present.

Does the Saks benefit work at Saks Fifth Avenue OFF 5TH locations? Those are the only ones near me.

Not sure about that specifically, but you can order from Saks online. Got some cosmetics for my wife in that manner

The card might be brilliant for Amex, but not for the card user. I’ll take the ease of use of Chase over the restrictive piecemeal “benefits” of this card any day.

In case my post wasn’t clear, that’s exactly what I mean: it’s brilliant for Amex. Whether or not it works well for the cardholder depends upon the cardholder’s spending habits.

The term is “dribs and drabs”, not “drips and drabs”

That’s true. Thanks. Fixed.

The fact that the Uber credits are done on the Uber side and not the Amex side may be an indication that they are paid for, in part or full, by Uber. But for business travelers this is a HUGE detraction as it means we can’t capture the benefit, instead effectively giving it to our employer.

Amex misses a huge point. It’s too much work to get the value. I don’t have time to track all these things every month. I’ll stay with Chase..

From Amex’s POV that’s a feature not a bug since it is a type of breakage.

It might be a feature for them, but I avoid getting their card because of them making everything so difficult. There’s a point of too much effort and they frequently cross that line

Every feature isn’t supposed to be used 100%. If everyone used every single feature all the time there would be no card benefits because it would be unsustainable. Imagine if every customer placed purchase protection claims up to the max amount every year. That benefit would go away. For my family, we always order a pizza at least once a month, and our favorite pizza place is on Seamless and has no delivery fee. This is $10 in my pocket every month for something I’m already doing. If you live in rural South Dakota, this benefits is worthless to you.

In addition, I suspect these new benefits are here for the long haul. I’d rather have decent benefits that get added and stick around than benefits that seem awesome and then get axed relatively quickly (Prestige, CSR).

You cannot escape the simple fact: a benefit someone doesn’t use is a benefit someone doesn’t care about. If a benefit suffers breakage, than the benefit also suffers from a lack of desirability. AmEx is trying anything to differentiate themselves from Chase, but this time they have been to smart for their own good. These are yawners.

That’s definitely a feature not a bug. Lots of work to extract 100% value and only that value is EXACTLY what Amex wants. Amex wants you to GIVE UP, make your card default for Grubhub and put $1000+ spend a year on it. They want you to drop by Saks and occasionally pick up a credit. They want it plugged in as your default Uber card. And they want you wanting to carry it around all the time so that maybe sometimes you pull it out just for a nonbonused spend.

But if I don’t want to do the work, then I don’t see it as a benefit, and I don’t take that into account in evaluating which cards to apply for, hold, use or renew. I can see from their view it may benefit them in terms of some customers, but it just doesn’t have any appeal to others.