Hotel credits have become rather ubiquitous on travel rewards credit cards. I would say that I’m swimming in hotel credits, but the truth is that it feels more like I’m drowning in hotel credits. Complexifying things is the fact that I’m a serial stacker, always looking for the best deal. That combination of factors recently led to analysis paralysis, where I had a lot of difficulty deciding just how to book a two-night hotel stay where elite status and benefits don’t particularly matter. This post is my attempt to help myself figure out how to book a two-night hotel stay, whether by using one of my various credits or stacking the best possible deal.

The situation

The situation at hand is that I need a two-night stay at a Caesars property on Lake Tahoe. I’m heading to Lake Tahoe for a Caesars tier credit multiplier in order to run the numbers on earning the rest of the way to Caesars Diamond Plus status in a single day.

I intended to stay at Caesars Republic Lake Tahoe since that property has been newly renovated. Reviews I’ve read suggest that Harrah’s Lake Tahoe, its sister property, which is connected by an underground walkway, is a bit more dated.

Unfortunately, I dragged my feet until availability completely disappeared at Caesars Republic for one of my nights. It was still possible to book a run-of-house room if I booked directly through Caesars. I didn’t particularly like the idea of a run-of-the-house room because I could get stuck with a smoking room. I don’t smoke, and I hate the smell of cigarette smoke. While I accept that going to a casino means being exposed to smoke, I don’t really want to retreat to a room that also smells like smoke. I decided to go with Harrah’s.

I don’t really care whether I end up with a room that has two queen beds or a room with one king. I’d slightly prefer the king, but not enough to pay (much) for it.

I’m only staying for two nights. Since it’s a casino property, elite status isn’t particularly important. I’m therefore relatively ambivalent about how I book the property, but I have quite a few different options that have my head spinning . . .

Various hotel booking platforms/credit options

To kick things off, here is a brief rundown of hotel credits I currently have available:

- $300 Amex Fine Hotels + Resorts or The Hotel Collection (I have several of these). Current credits expire 6/30/26. Spoiler alert: Harrah’s isn’t on those.

- $300 Citi Strata Elite hotel credit for a stay of 2 nights or longer booked via Citi Travel. Current credit is valid through the end of 2026, though we may not renew this card when it comes up for renewal this fall, so it may effectively expire sooner.

- $200 Bilt Palladium hotel credit for a booking of 2 nights or more booked via Bilt. This credit expires 6/30/26.

- $250 The Edit by Chase Travel℠ credit. We have 4 of these credits between my P1 and P2 that expire 12/31/26. Spoiler alert: there are no The Edit properties that fit for this.

- $250 hotel credit through Chase Travel for select brands. Again, this doesn’t apply to this stay.

- $100 Splurge credit on Citi AA Globe card that can be used for hotel booking through AA Hotels. My wife and I both have this credit, and it is valid until the end of the year, though we may not renew my wife’s card when it comes up for renewal in October (we’ll keep mine for sure)

- Plenty of Capital One Shopping money to redeem for Hotels.com gift cards to cover this stay

- Plenty of Caesars Rewards credits to cover the stay if booked direct

While a few of those wouldn’t fit here, many of them could, so I had to weigh my options.

I should add that there is a current Amex Offer good for $40 back when you spend $200 or more at select Caesars Rewards properties (Lake Tahoe is included). Many of the options below require paying a ~$68 resort fee at the hotel. If I also charged meals to the hotel during my stay, I would likely be able to trigger that offer and save an effective ~20% on the resort fee + food, sort of inadvertently reducing the cost of some of the options.

But it isn’t yet clear to me which option is best, so here they are . . .

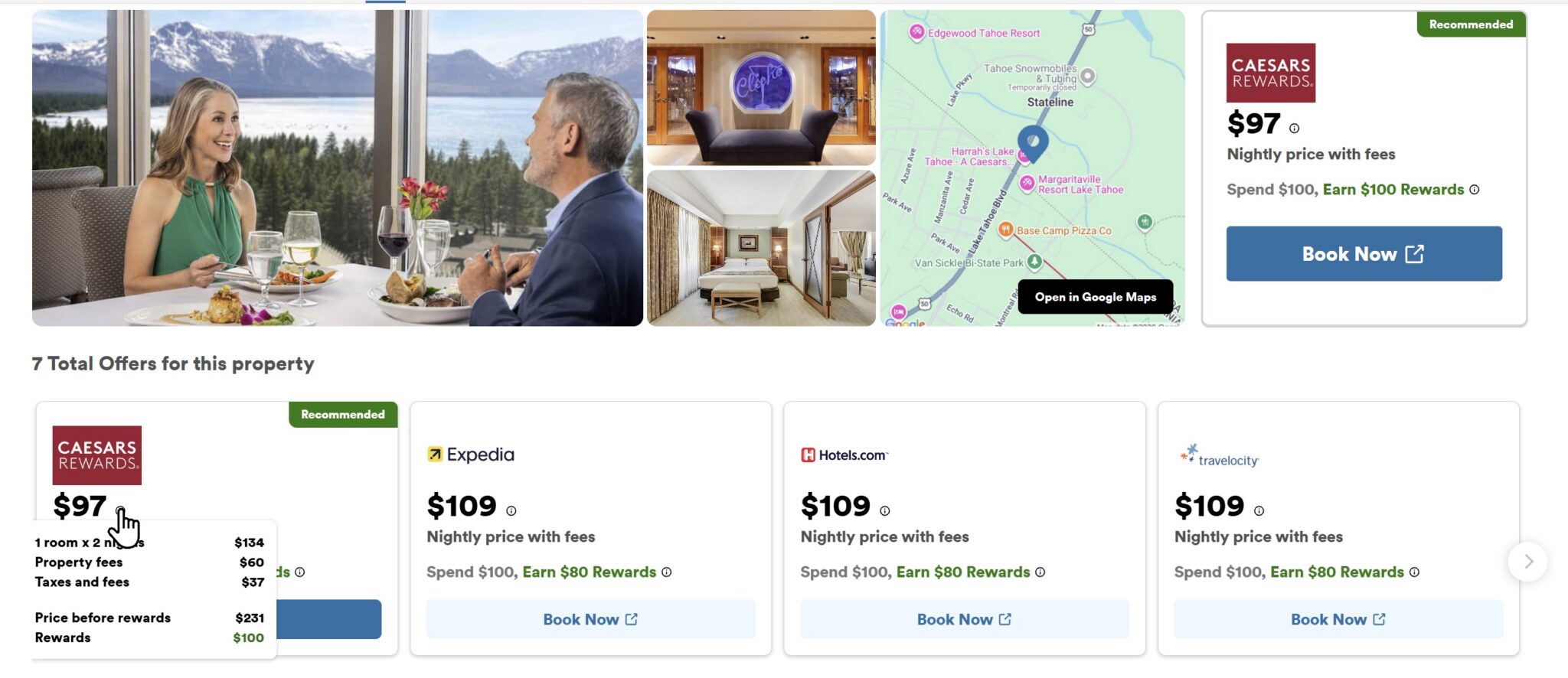

Book direct with Caesars and stack with portal cash, possible Amex Offer, or use Rewards Credits

A clear advantage of a direct booking would be the ability to use Caesars Rewards credits to pay for my room. There are a couple of ways I could stack to make the deal a little bit better:

- Click through from Rove Miles to Caesars to earn 6.5 miles per dollar on the base rate based on the current rate at the time of writing (1,176.5 Rove miles, worth $16.47 based on our Reasonable Redemption Values)

- Use an Amex card enrolled in an Amex Offer that’s good for $40 back on $200 or more. Note that enrollment is required, and this offer expires 5/24/26.

That would make the net cost approximately $225.75 after the Amex statement credit and Rove Miles.

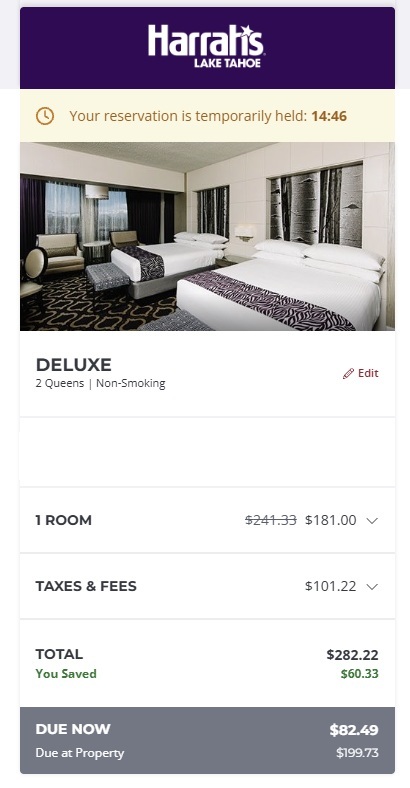

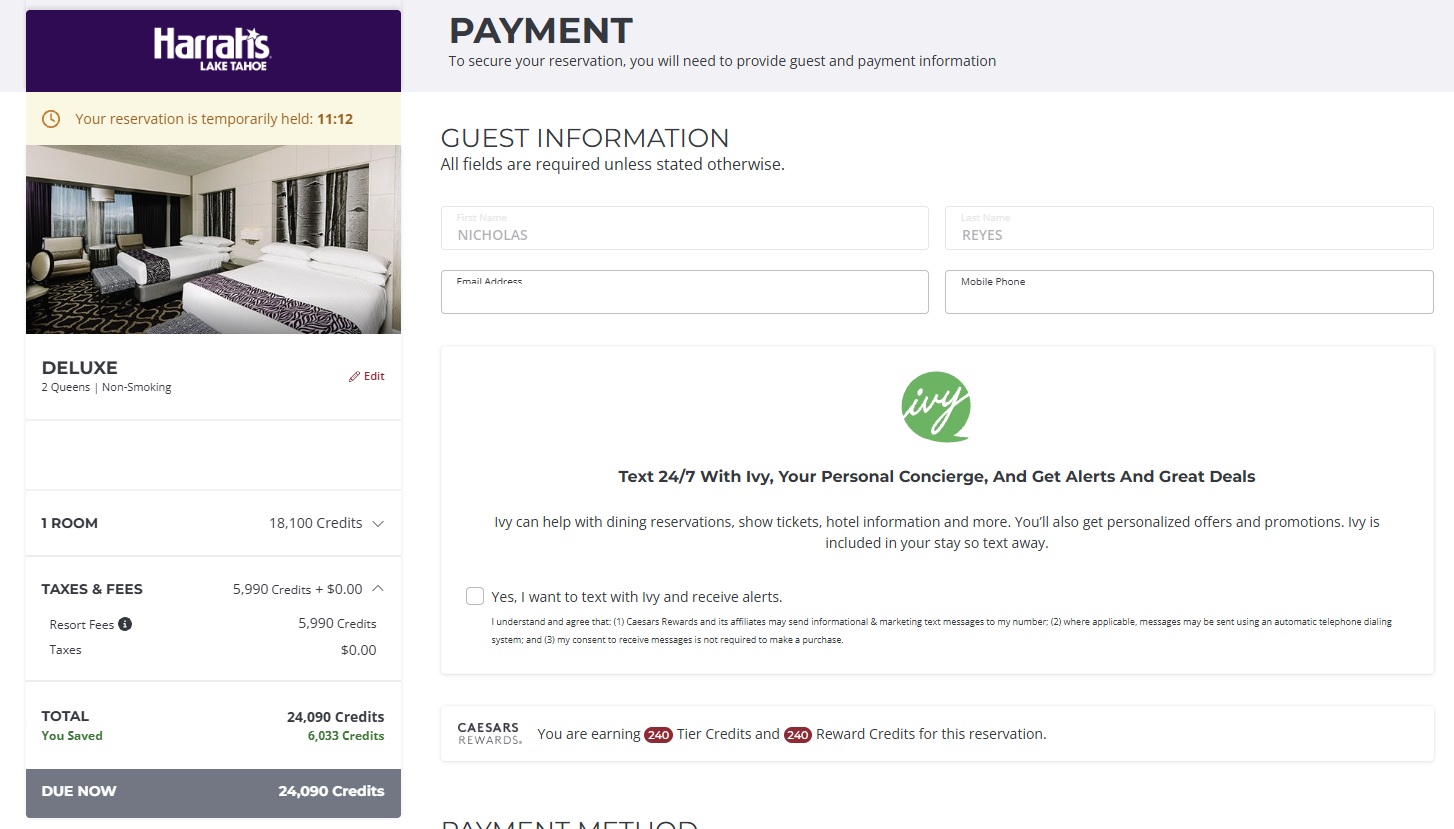

Book direct with Caesars and use Rewards Credits

Since I recently opened the Caesars Prestige credit card and I have also moved some Wyndham points to Caesars in the past, I could use Caesars Rewards credits to cover the room and resort fee. Caesars would charge me 24,090 reward credits total to cover the room and resort fee. There would be no tax, which makes reward credits worth a little bit more than I realized. I knew that they could be used at a value of one cent each toward room and some types of charges while on property, but I hadn’t realized that they could be used to cover the resort fee and eliminate taxes on the room. That actually makes them worth a bit more than 1c per point when used toward rooms.

Interestingly, it still shows that I would earn Tier credits and reward credits on the reservation even when using reward credits to pay, so maybe I would still earn the Rove miles also.

However, there are quite a few other ways to consider booking this room.

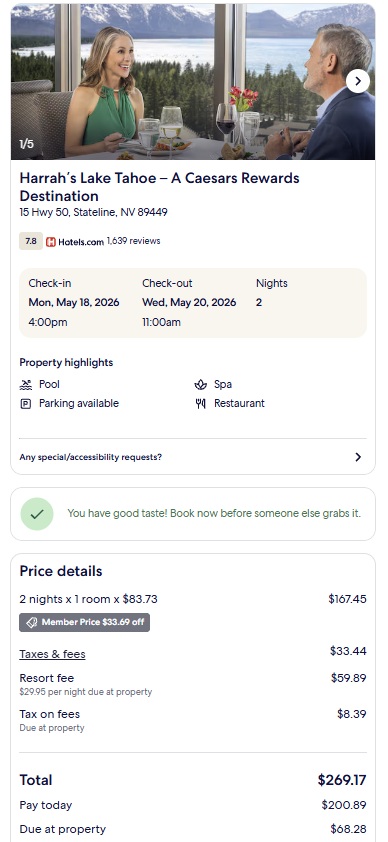

Redeem Capital One Shopping rewards and book through Hotels.com + Retailmenot

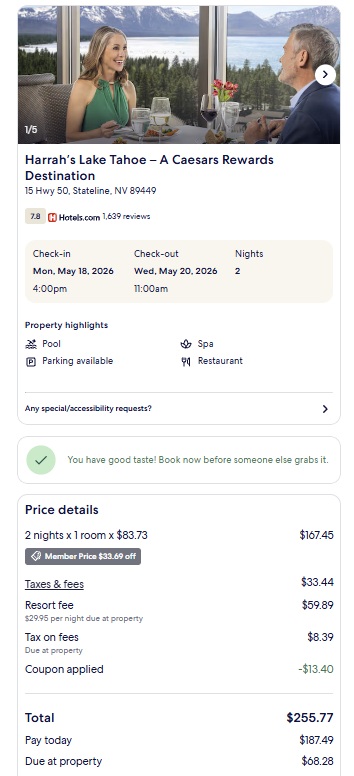

I currently have OneKey (the Expedia/Hotels.com/vrbo loyalty program) Silver status thanks to having made a few Hotels.com bookings last year (using gift cards from Capital One Shopping to pay for my stays). As a result, I qualify for some special member pricing, which in this case got me a discount shown as $33.69 off. Interestingly, and this is new to me, Hotels.com is offering me the choice to either save now with that discount or bank that money for later as OneKey cash. As you can see, the price through Hotels.com is actually a little bit better than directly via Caesars, with the total coming to $269.17. I have plenty of Capital One Shopping gift card money to cover that.

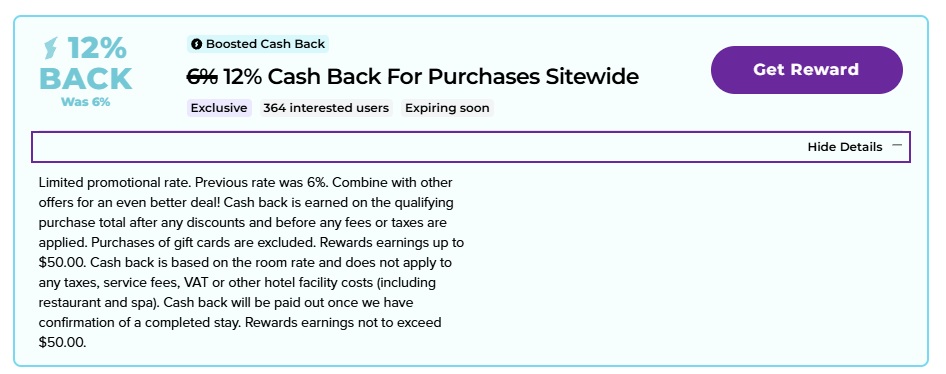

But this option actually gets a little bit better. I could click through the shopping portal to go to Hotels.com and make this booking. At the time that I’m writing this, RetailMeNot is offering 12% back on Hotels.com bookings, up to $50 back.

I would only expect to earn that 12% back on the room rate portion of the bill, which means I would expect to earn 12% of $181. That’s $21.72 back from RetailMeNot. But it gets a little bit better yet because RetailMeNot currently has a couple of coupon codes listed on their site, and at least one of them works. They list a coupon for 10% back in the Hotels.com app or 8% back on the website. Since I was doing this comparison on my computer, I tried the code for 8% back on the website, and sure enough, it worked to drop the total price of the hotel by just a little bit.

That would drop the RetailMeNot cash back to just over $20. The resort fee portion of this is due at the property, so I would need to pay $187.49 to Hotels.com, which I could cover entirely with Hotels.com gift cards from Capital One Shopping. I’d end up with $20 in real cash back from RetailMeNot, using a net $48.19 out of pocket, along with the $187.49 in Capital One Shopping money to cover this stay. You could call the net cost ~$235, but most readers probably wouldn’t value Capital One Shopping cash at full face value, so I think it is more accurate to think of the net cost as $48.19 in real money + $187.49 in Capital One Shopping rewards.

Targeted Capital One Shopping offer for $100 back on $100

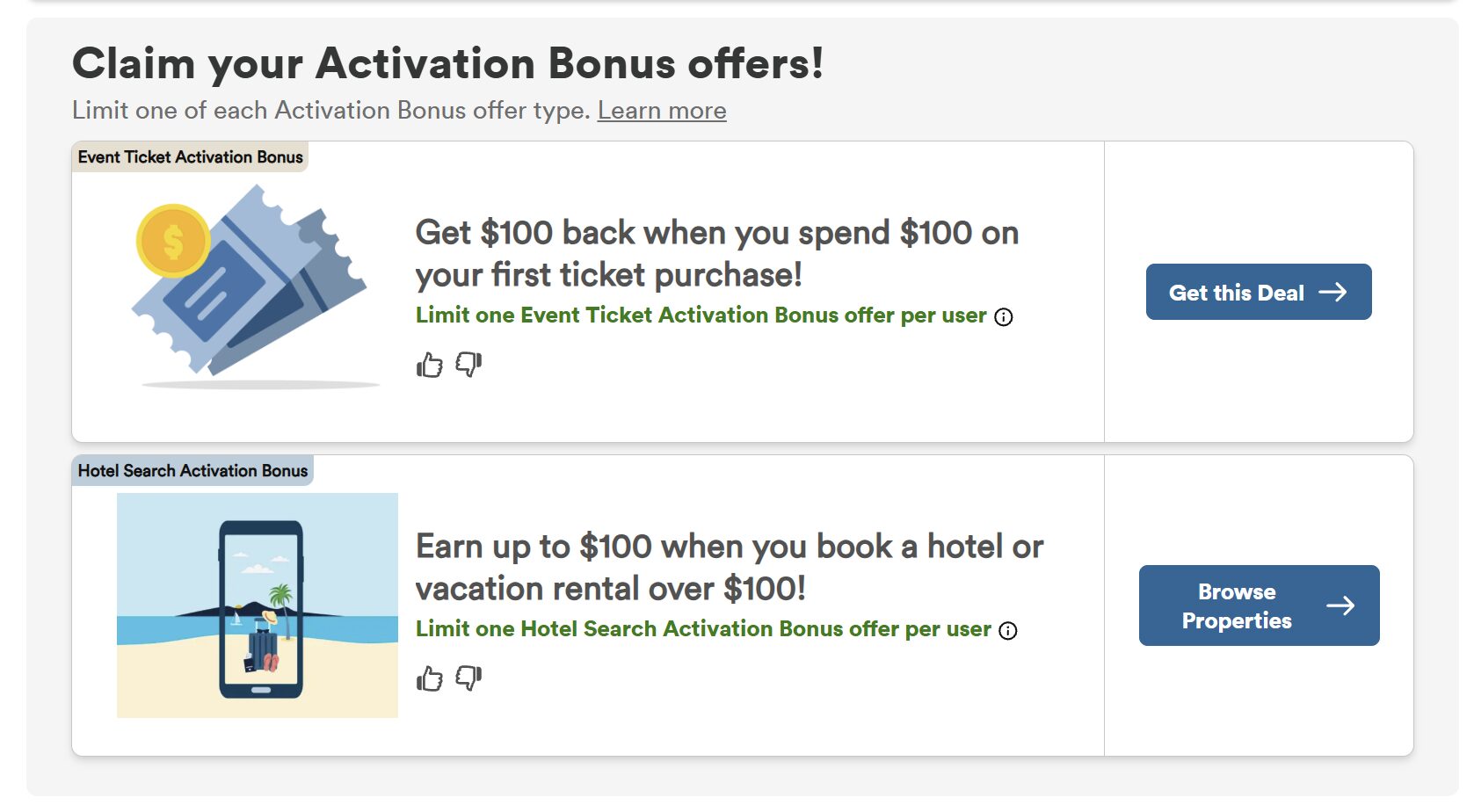

I might be able to do a little bit better yet through Hotels.com, depending on your perspective. Yesterday, I got targeted through Capital One Shopping for a special homepage offer to either get $100 back on an event ticket purchase of $100 or more or $100 back on a hotel booking of $100 or more. Again, these are targeted offers that only some members see.

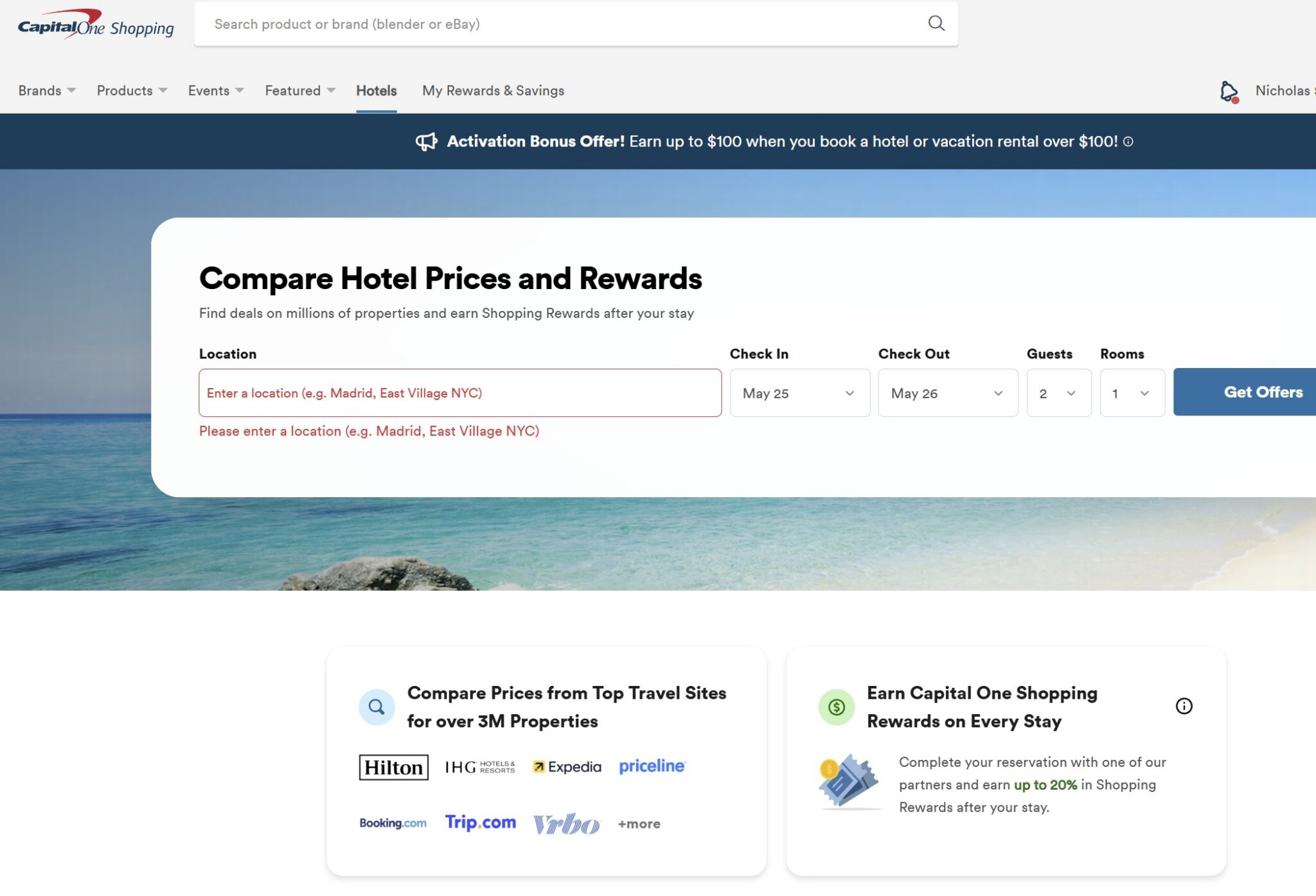

The offer is a little more complicated to use than I expected. You need to use the Capital One Shopping Price Comparison tool to compare prices across sites like Priceline, Expedia, Trip.com, Agoda, Booking.com, Hotels.com, and more.

Interestingly, the “$100 back on $100” varies depending on the booking channel you choose. As you can see here, I could get $100 back if I clicked through to book directly with Caesars:

However, as you’ll probably notice above, the rate via Hotels.com was listed as being a little higher, and it would only be eligible for $80 in rewards if booked through Hotels.com. The total price was listed as $248, though I think it was likely off as it would have probably come to the same ~$269 as above.

Assuming that is true, and I wanted to book through Hotels.com rather than booking direct, I would be on the hook for the ~$269 price shown further above from Hotels.com. Today, I would pay ~$200 via Hotels.com gift cards (redeemed from Capital One Shopping). Later, I would have to pay the resort fee at the hotel, which would be $68.28 out of pocket.

To kind of break that down, I would redeem Capital One Shopping rewards for a Hotels.com gift card for ~$200 in order to avoid paying anything out of pocket right now. I would later spend $68.28 out of pocket at the hotel, eventually getting $80 back in Capital One Shopping Cash.

Spending $200 in Capital One Shopping cash now and later getting $80 in Capital One Shopping cash back means that the net result here is that it would cost me $120 worth of Capital One Shopping Cash and $68.28 cents in actual cash.

Maybe it would have been possible to click through to Caesars and pay with Caesars Rewards credits (24,090 Rewards credits) and still earn the $100 back from Capital One Shopping. I don’t know whether that would have worked, but I didn’t try that.

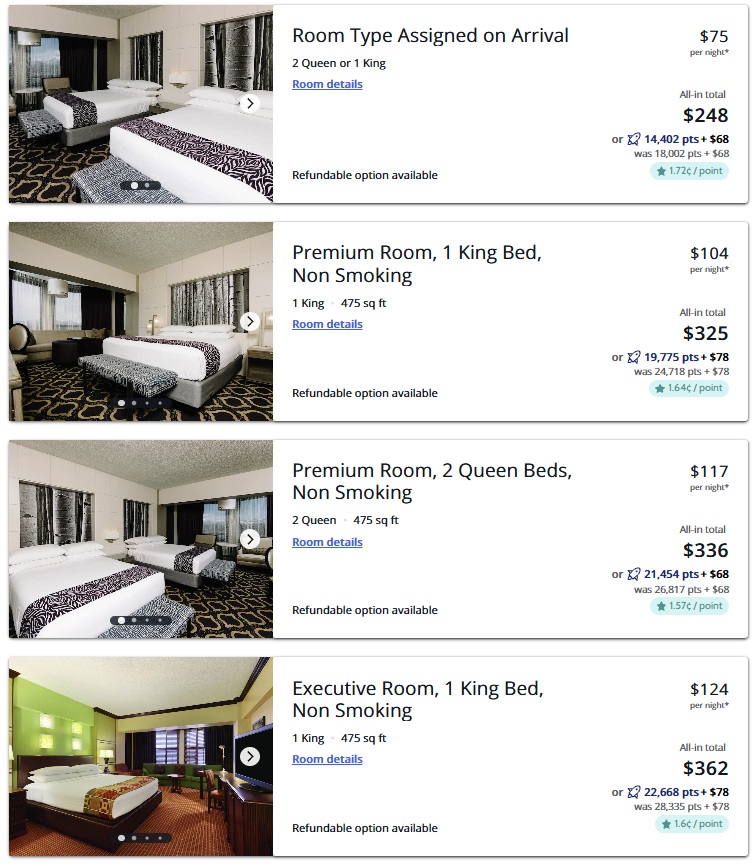

Book via Chase Points Boost

Via Chase Travel, the prices are inflated. Oddly, the 1 King premium room is less expensive than the 2 Queens premium room (despite the room with 2 Queens being cheaper when booking directly or via Hotels.com).

You might notice that the cents per point (cpp) redemption rate listed by Points Path is variable depending on the room type. However, that appears to be an error with how Points Path is calculating the rate as it’s not accounting for the resort fee which is paid for at the hotel. When accounting for that, the Points Boost rate is 1.25cpp for each room type.

Interestingly, the resort fee is less on some room types at $68 than it is on other room types at $78. I don’t really understand why, but either way, you have to pay that cost out-of-pocket.

I’m not actually going to book the room this way, but I wanted to include it for completeness here. The 1 King room that I would book would cost me more than 19,775 points plus $78. That’s clearly inferior to the other options so far, so I didn’t spend any more time thinking about this one.

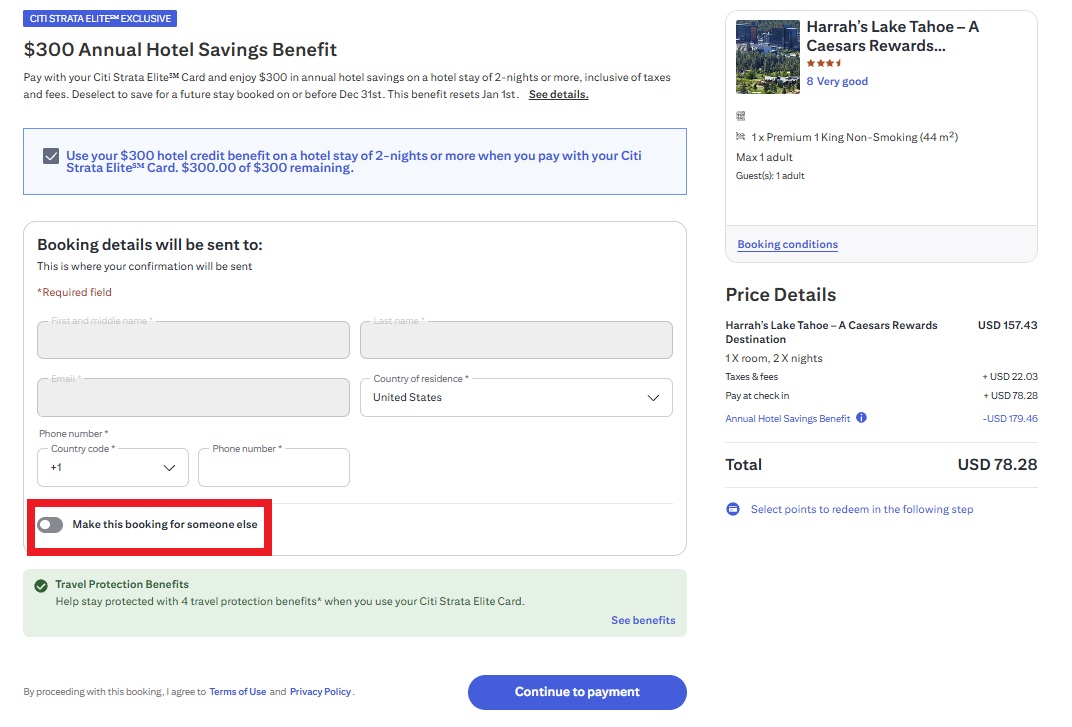

Citi Travel to use Strata Elite $300 prepaid hotel credit

My wife has the Citi Strata Elite card. One of the benefits of that card is a $300 credit for a prepaid hotel booking of two nights or more. We haven’t yet used that for this year, and we don’t have any clear plans to put it to use. I hadn’t been very interested in booking through Citi Travel because of its past reputation for higher prices and the fact that you won’t typically earn hotel points and elite credits. With this stay, those hotel points and elite credits aren’t meaningful.

After my recent surprises with the terrific pricing I found on rental cars through Citi Travel, I became significantly more interested in checking it out for this hotel stay.

And Citi once again surprised me with better pricing than I expected. Initially, the system showed an even better price than what is shown above, but when I got to the checkout page and toggled the switch to make the booking for someone else, it popped up a message saying that the price was no longer available. I don’t know whether it had anything to do with me toggling that switch.

The best price available through Citi Travel was for a room with one king bed. I was happy to see the total price here of $179.46 plus the resort fee of $78.28. The Strata Elite hotel credit would cover the $179.46 of the room rate, taxes, and fees, while I would have to pay the $78.28 out of pocket at the hotel. That would be a pretty good deal. It would somewhat awkwardly leave me with about $120 of the Strata Elite Card’s annual hotel credit. Since that $120 left over would need to be used on a stay of two nights or more, I fear that the credit would become even harder to use in full. That made me less excited about using the Strata Elite.

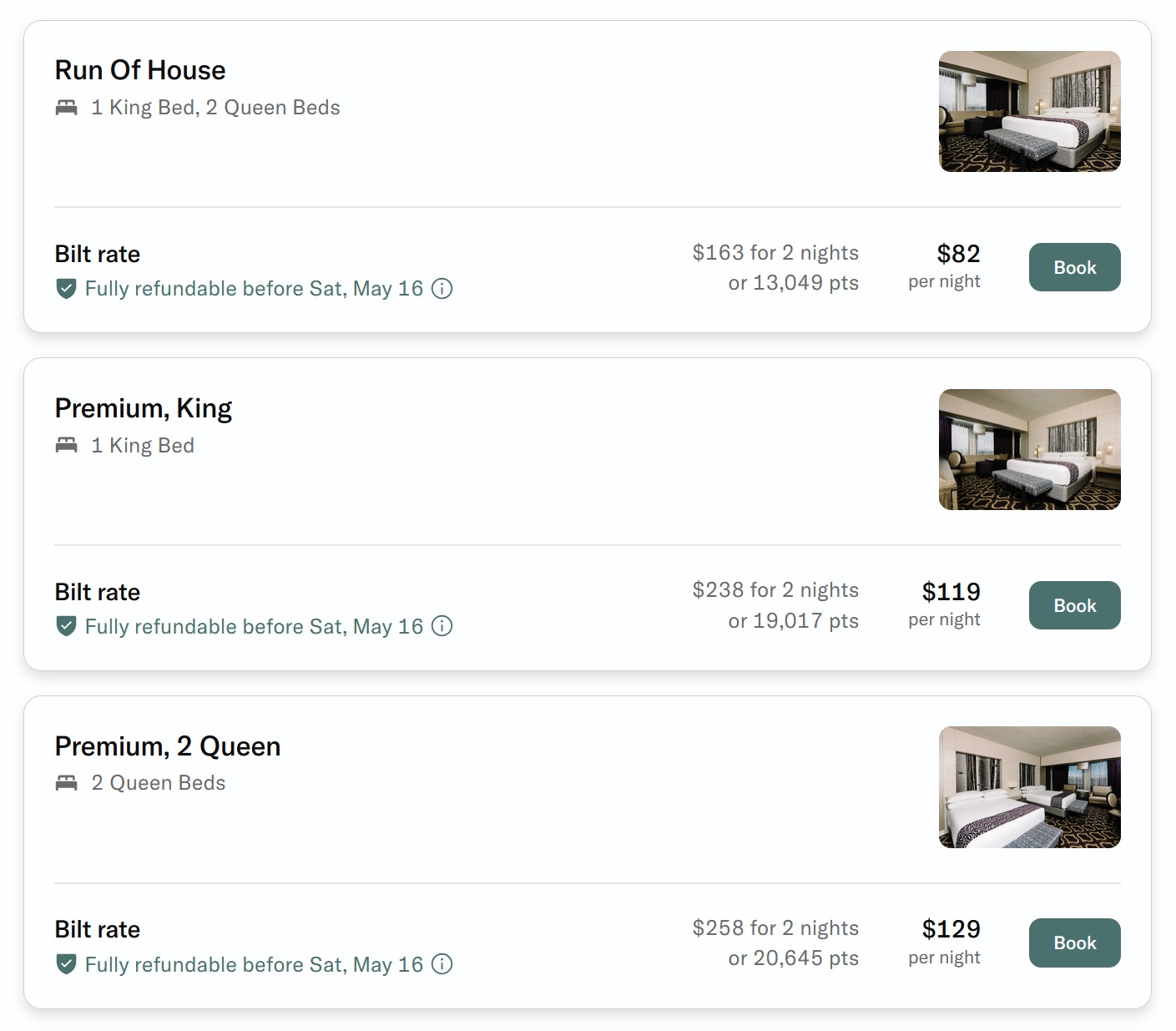

Bilt Palladium $200 hotel credit

While the Citi Strata Elite 300 credit might be overkill, my next thought was to see if I could make use of the Bilt Palladium card’s twice-a-year $200 credit for a hotel booking through Bilt. That credit has to be used once between January and June and once between July and December. Further, it can be topped off with an additional $100 hotel credit by using Bilt cash. My wife hasn’t yet used either credit on her Bilt Palladium card for the first half of this year, and we haven’t had a clear use in mind as to how we would use it. That would make this stay a potentially perfect use of Bilt cash.

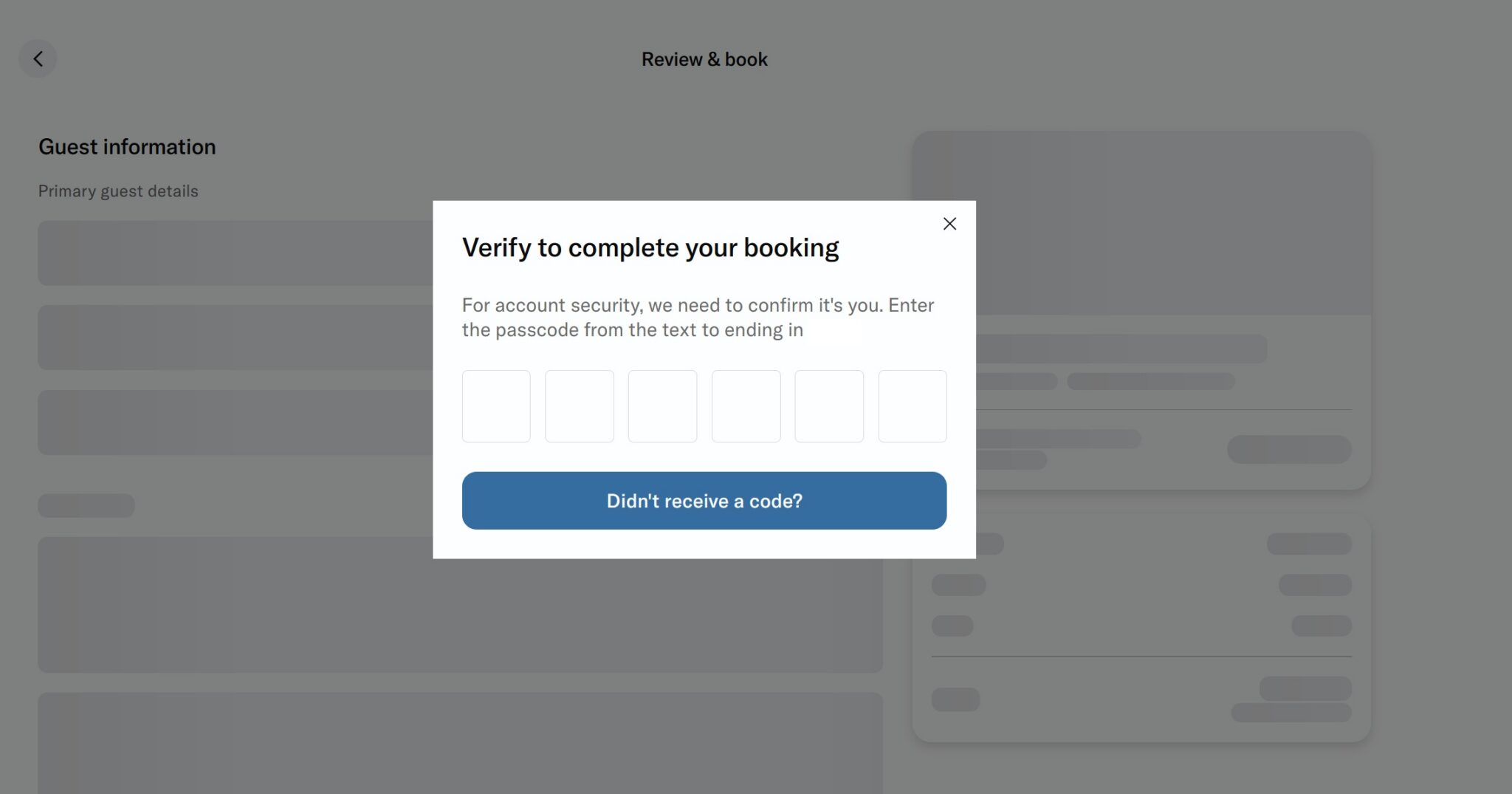

Annoyingly, Bilt makes it really hard to see the entire price of a hotel. While you can see the room types listed above along with prices in initial search results (as shown above), it doesn’t show a full breakdown with taxes and fees unless you click “Book”. I find that really misleading. Labeling the button with the word “Book” makes it seem like clicking that button will force the booking, which may not be what you want to do. In fact, if you do decide to chance it and click that button in the hopes that it will take you forward to a checkout page, the next thing you see is a pop-up asking you to confirm with a text message code to make your booking.

The background makes it look like you would have a place to enter guest information and see a full price, but the wording certainly makes it sound like the hotel is going to be booked if you enter that text message code. That would make me really nervous about any sort of non-refundable booking.

However, in this case, the hotel would be refundable, so my wife went ahead and entered the text message code.

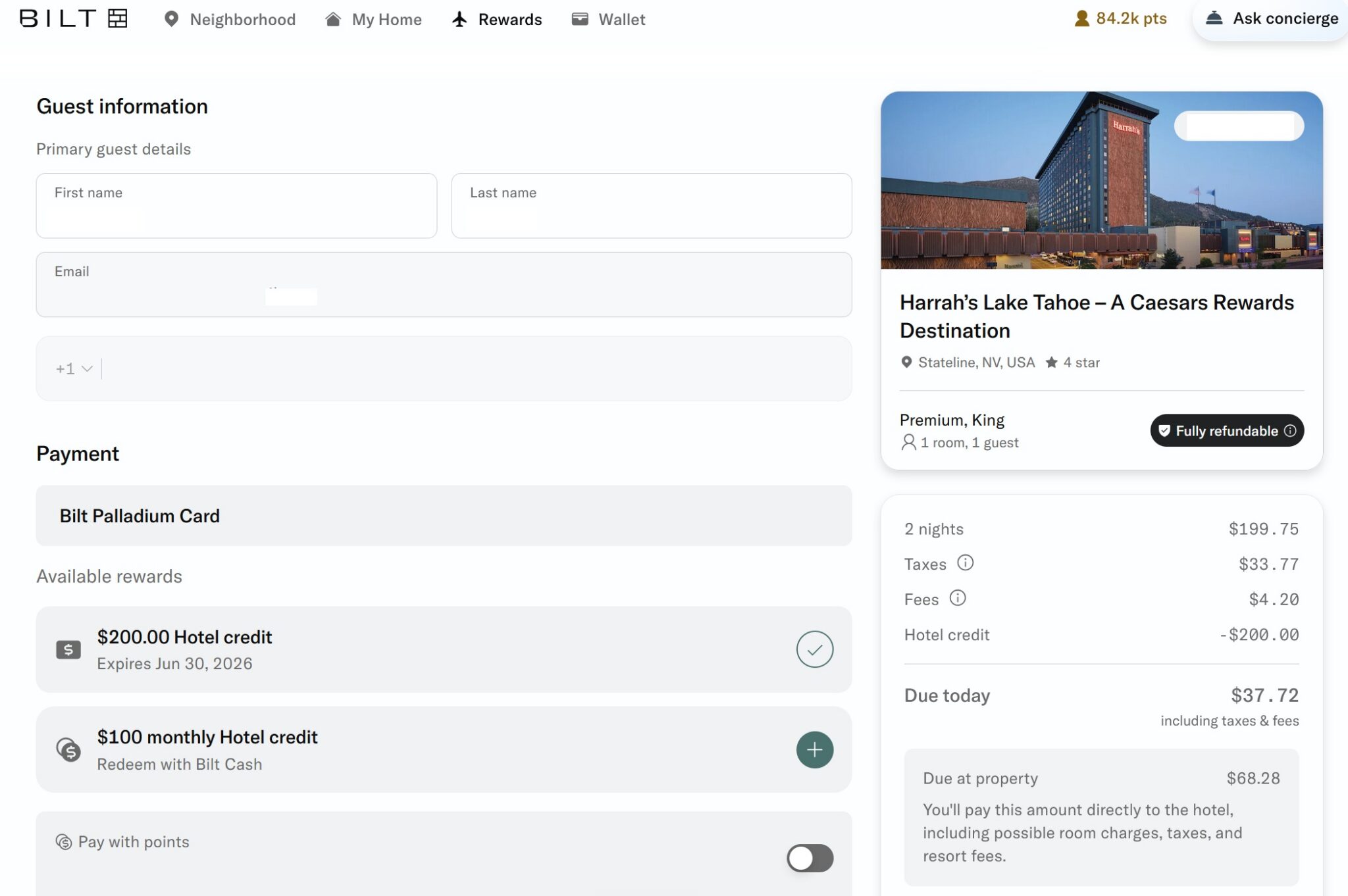

As you can see above, by booking through Bilt, we could use my wife’s Bilt Palladium hotel credit. Since Bilt’s price was higher than Citi’s price, I’d have to come out of pocket for another $37.72 in addition to the $68.28 due at the hotel for the resort fee. I thought that this would be the perfect opportunity to use a little Bilt Cash to cover the $37.72 overage. Not so fast . . .

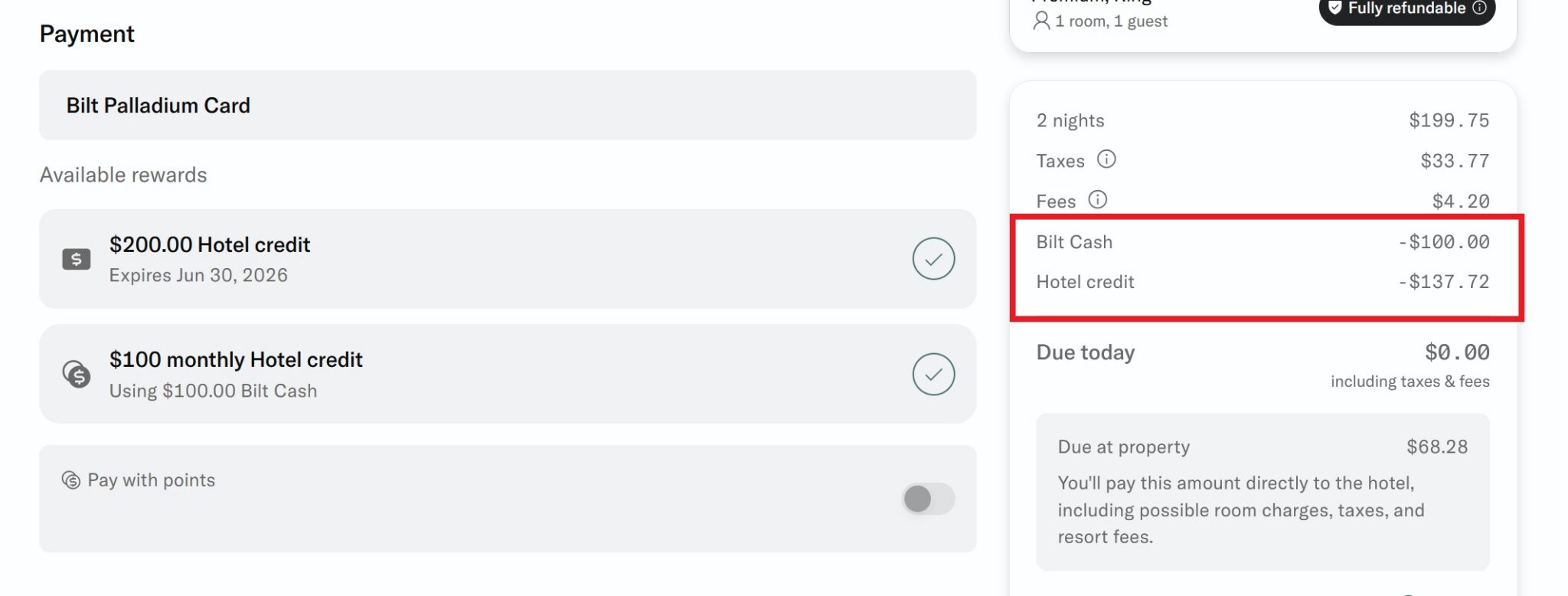

It is possible to toggle on both the hotel credit and the $100 monthly hotel credit that you can cover with Bilt Cash. However, that $100 monthly hotel credit via Bilt Cash has to be used as a whole. It wasn’t possible to use just $37.72 in Bilt Cash.

Instead, if I wanted to use the $100 monthly built cash hotel credit, it would reduce the amount going toward the Palladium Cards hotel credit. Instead of using the $200 Palladium Card hotel credit, it would only use $137.72 of Bilt Palladium hotel credit plus the $100 in Bilt Cash hotel credit.

That would leave me with ~$62 of unused hotel credit that expires on 6/30/26 and can only be used to book a hotel stay of 2 nights or more. I didn’t particularly like that idea.

A potential solution would have been to have booked an upgraded room that had a price closer to $300, so I could use the entire credit in one shot. I didn’t prefer that here as I hope we’ll be able to put the Bilt Cash to use in some better way (like via a transfer bonus).

AA Hotels with Citi AA Globe Splurge Credit

The option I almost completely forgot until the very end was that I could book via AA Hotels. The main draw here for me would be that the Citi AAdvantage Globe Card has a $100 Spurge credit. One of the options for that credit is booking prepaid hotels through AA Hotels.

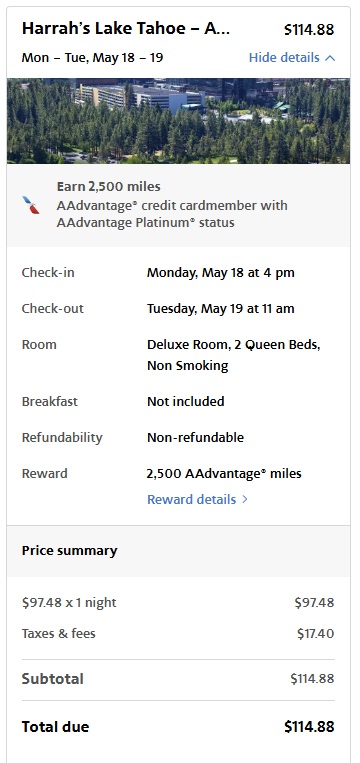

My wife and I both had Barclays Aviator Silver Cards that were recently converted to the Citi AA Globe Card, so we each have one of those Spurge credits to use. As you can see above, the first night would have been $114.88 plus resort fee. After my $100 Spurge credit on a Globe Card, this night would cost me $14.88 out of pocket, plus the ~$34 resort fee and resort fee taxes. Additionally, I’d have earned 2,500 American Airlines miles (and Loyalty Points). Those miles are worth almost as much as the cash outlay in this case, making the first night feel almost net free.

Unfortunately, the same room type was significantly more expensive the next night at $183.82 plus resort fee. It would have come with more miles at 3,400 American Airlines miles, but even after the credit, it would cost me about $118 between the leftover portion of the room charge and the resort fee for that second night.

Even with the price differential, this can be a contender. Consider that it breaks down pretty well:

- Night #1: Net $14.88 + $34 resort fee, earn 2,500 miles

- Night #2: Net $83.82 + $34 resort fee, earn 3,400 miles

- Total: $166.70 out of pocket for 2 nights + 5,900 miles/Loyalty Points

According to our Reasonable Redemption Values, the miles are worth $82.60, making the “net” cost here $84.10. That’s certainly a contender.

With cash rates I had been seeing earlier in the week, I might have been able to cover the room rate portion of a 2-night stay with a single card credit if I had thought of this a few days prior (paying just resort fees out of pocket).

Summarizing the options

To sum things up, I could:

- Book direct, paying a “net” $225.75 (accounting for the value of Rove Miles)

- Use 24,090 Caesars Rewards credits to cover the room in full (possibly still earning ~$16.50 in Rove miles and over $2 in Caesars Rewards), paying nothing out of pocket

- Pay a net $48.28 out of pocket (after $20 back from Retailmenot) + $187.49 in Capital One Shopping cash

- Pay $68.28 out of pocket + a net $120.89 in Capital One Shopping rewards (using $200.89 in Capital One Shopping rewards initially and getting $80 back later)

- Pay $78 out of pocket at the hotel + 19,775 Chase Ultimate Rewards points

- Pay $78.28 out of pocket at the hotel + use $179.46 in Citi hotel credit (leaving us with $120.54 in hotel credit through Citi that can only be used on a stay of 2 nights or longer)

- Pay $106 out of pocket ($37.72 via Bilt + $68.28 at the hotel) and use $200 of Bilt Palladium hotel credit

- Pay a “net” $84.10 through AA Hotels ($166.70 out of pocket, getting back 5,900 miles)

The right answer there doesn’t necessarily seem super simple to identify. I suppose it really came down to:

I kept finding myself coming back to the expiration dates. The Bilt hotel coupon expires in six weeks, and we have no other plans to use it, which created a sense of urgency. Keeping my Capital One shopping rewards available for redemption later feels like it makes sense since those don’t expire, and there are a lot of different ways I can use them, not just for hotels.

Booking via AA hotels is the one alternative that seems particularly interesting. We aren’t under a time crunch to use those hotel credits, but I don’t anticipate where we’ll use them yet otherwise. It’s a really strong contender here, particularly because I do value American Airlines miles pretty highly. It would also get me a chunk of the way to requalifying for American Airlines status. AA Hotels is intriguing here!

Ultimately, I booked via Bilt, but I’m still within the cancellation window. AA hotels certainly has me reconsidering what to prioritize here.

I think this really illustrates the problem with expiring hotel credits and the reason why you really shouldn’t value them at full face value. The $200 Bilt Palladium credit simply is not saving me $200 in actual cash in this situation. In fact, it cost me a little cash over what I would pay via some of the other booking channels, but it gave me the opportunity wipe the soonest-expiring credit off the books. It wasn’t worthless, but it was worth significantly less than $200.

I was pleasantly surprised to see that Citi once again showed strength in pricing. Citi’s all-in rate was not only better than the rate I would get booking directly with Caesars as a Caesars Platinum member, but it was also better than Hotels.com after using RetailMeNot’s 8% discount code. The 12% in cash back through RetailMeNot would drop the net price lower until you consider the 12 Citi ThankYou points per dollar spent on a booking through Citi, were it not for the credit being used to cover the stay.

Not very surprising is the fact that Chase Travel was overpriced. Unfortunately, we’ve seen that pretty consistently (though not always).

Very surprising was the fact that Chase Travel is offering a variable points boost at a single property on a single set of dates, depending on which room type you select. In this case, the least desirable room type yielded the highest value per point, with higher room categories offering less value per point with the points boost. That’s really disappointing to see.

Overall, I hate that it takes this much effort to figure out the best way to book a hotel. The amount of time I spent comparison shopping credits here really soured me on having so many, or at least on the value of having more than one or two to consider. I’ll keep that in mind as cards come up for renewal.

")

Nick, regarding Bilt, don’t forget about the ability to stack a monthly $100 Bilt Cash redemption on top of the semi-annual $200. For a total of $300.