The average American has three or four credit cards. Of those, about half of them carry a balance from month to month which results in them paying high rates of interest and thereby taking longer to pay off that kind of unsecured debt.

It’s therefore not too surprising that many people are of the belief that if you open lots of credit cards, it’ll have a negative impact on your credit score. In reality though, that’s not necessarily the case. In fact, in some circumstances having lots of credit cards can improve your credit score.

That can be particularly pertinent when getting into the world of points and miles because one of the best and easiest ways to earn travel rewards is via multiple credit card welcome bonuses, as well as everyday spending in bonused categories.

In this post we’ll explore how and why, contrary to popular belief, having lots of credit cards can be good for your credit score.

Before continuing, an important thing to point out is that we advocate responsible credit card usage by ensuring that you pay your credit cards in full each month in order to not carry a balance. Interest fees from not paying off balances will far exceed the value you’ll get from the points and miles you’ll earn.

What factors affect your credit score?

There are several factors that affect your credit score. Some of those can improve your score if you have multiple cards, while others might have a negative impact to some extent.

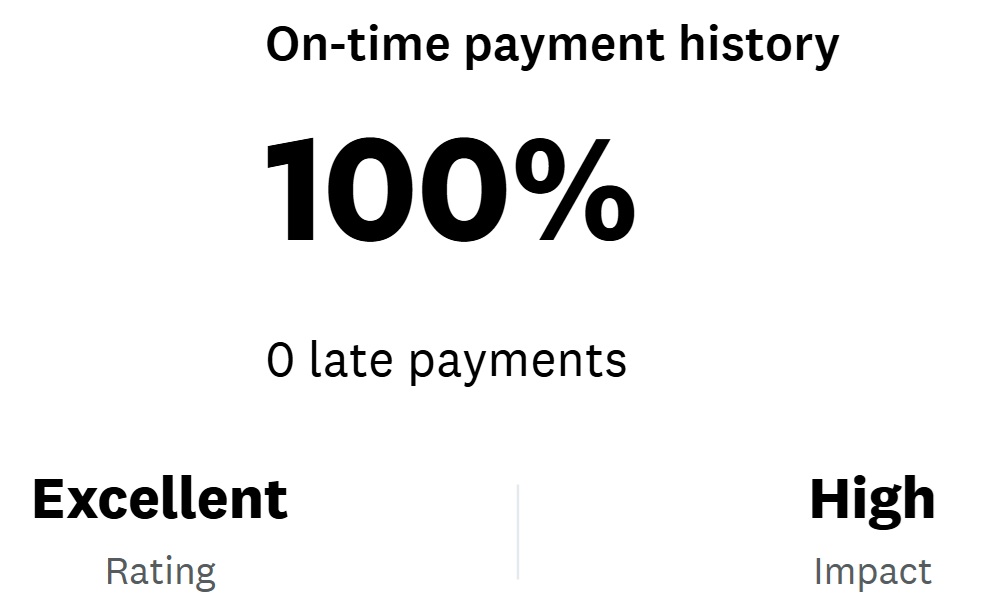

Payment history

The biggest factor affecting your credit score is payment history, representing a third of your score or more. If you have numerous credit cards where each one has a blemish-free history of on-time payments, that’ll improve your score.

Credit utilization

Another significant factor in the makeup of your credit score is credit utilization which makes up close to a third of your score. Credit utilization refers to how much of your credit lines you use, both on individual credit cards and across your credit card portfolio as a whole, based on your balances when your statements cut.

For example, let’s say you have a card with a credit line of $10,000. If you have a balance of $2,500 when the statement cuts, that would represent 25% credit utilization on that card.

The optimal credit utilization percentage varies depending on who you talk to. Most would agree that below 30% is the aim, below 10% utilization being ideal, with some suggesting 3% as being the optimal percentage rather than 0%. It’s thought that financial institutions looking at your credit report like to see some element of utilization, but not too high. 3%-10% utilization indicates that you’re using credit responsibly and that you’re using at least some of your cards. Consistent 0% utilization across all your cards can make it look more like you’re not actually using your credit cards.

There are a couple of things to particularly bear in mind regarding credit utilization. One relates to the fact that it’s based on your balances when your statements close, not necessarily how much you’ve spent in any given month. Let’s say you have a card with a $10,000 credit limit and you spend $9,000 on it in a month. If you pay $8,700 off before your statement cuts, it means only a $300 balance (i.e. 3% utilization) will be reported to the credit agencies once it does cut.

The other thing to bear in mind is that utilization on any given card could have a bigger impact on your credit score than utilization across all your cards. To demonstrate this, let’s suppose you have ten credit cards, each of which have a credit limit of $10,000. If each of those statements close with a $1,000 balance, that’ll represent 10% utilization overall.

If, on the other hand, nine of those cards close with a zero balance and the other closes with a $10,000 balance (i.e. maxed out), that too represents 10% utilization overall. However, despite both percentages being identical, the latter scenario with one card maxed out will likely be looked upon less favorably than if that spending was spread out equally across all the cards.

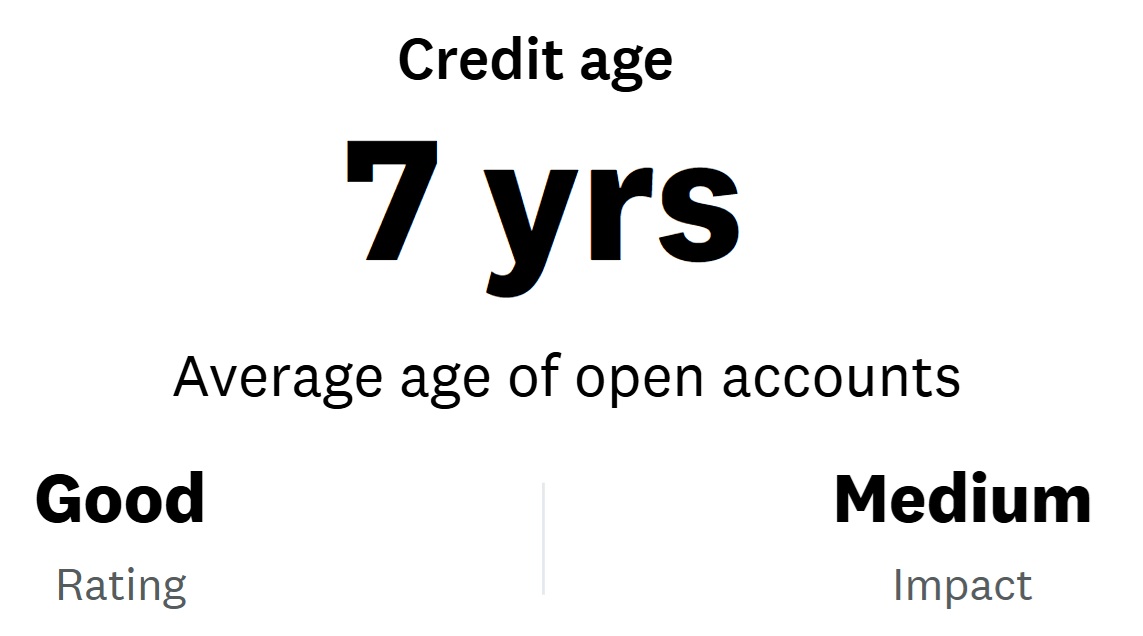

Average age of accounts

Another factor that affects your credit score is the average age of your accounts, with the longer that your credit cards have been opened the better.

That means that opening a new credit card reduces your average age of accounts to some extent, so opening lots of new credit cards to earn multiple welcome offers can have an even bigger impact on this aspect of your credit score.

The good thing is that the average age of your accounts only contributes ~12%-15% to your credit score, so its overall impact is far less than credit utilization and payment history.

Closing cards doesn’t affect your average age of accounts, at least not in the short term anyway. Credit cards tend to remain on your credit report for ten years after you’ve closed them and the age of those closed accounts count towards the average age of accounts in the same way as open ones.

That means that you don’t have to worry about closing credit cards and having it affect this metric, although closed accounts will have an effect on your overall credit utilization as you’ll have a lower credit limit overall. As a result, it’s still worth keeping cards open where possible rather than closing them.

If those cards have no annual fee, it’s best to simply leave them open seeing as they’re not costing you anything, even if you don’t plan to use them for purchases. These are what’s known as ‘sock drawer cards,’ alluding to the fact that you could stick them in your sock drawer and forget about them. That said, you don’t want to completely forget about them; instead, make a purchase with them every 6-12 months to ensure they don’t get involuntarily closed due to inactivity.

For cards that do have an annual fee but which you no longer want, look into downgrade options to a card that doesn’t carry an annual fee. That maintains your original card open date despite it being a different type of card, thereby not being detrimental to your average age of accounts. For more about that approach, check out this post: Downgrade paths: How to keep your card but break up with your annual fee or find a better fit.

Mix of credit types

There are many different ways that financial institutions provide credit in one form or another: mortgages, HELOCs, secured loans, unsecured loans, credit cards, and more. The more variety you have in types of credit extended to you, the better the impact on your credit score will be.

Your credit mix only has about a 10% impact on your credit score. If you already have a couple of credit cards open, it’s unlikely that opening several more cards will improve your score, but neither will it have a negative effect for this specific factor.

Hard inquiries

The other main aspect that affects your credit score is the number of hard inquiries (i.e. credit pulls) on your credit report.

As you might expect, this is another factor where opening lots of new credit cards can have a negative impact. After all, most banks do a hard credit pull when you apply for a new credit card (American Express is usually a notable exception if you’re an existing cardholder), so opening new cards inevitably result in more hard inquiries.

The good thing is that hard inquiries have a somewhat minimal, as well as a limited time, impact. When you apply for a new credit card, you might see an initial drop in your credit score of 3-10 points, but that’s usually only for a few weeks or months before later rebounding, even though the inquiries themselves might still show on your credit report for a couple of years. If you apply for many new cards over a short period of time, those 3-10 point drops for each card will have a larger overall effect, so it can be worth spacing out applications if it doesn’t mean you’ll miss out on limited time increased welcome offers.

Summary of impacts

As detailed above, opening many new credit cards can have a negative impact on your credit score when it comes to the number of hard inquiries on your report and your average age of accounts. The good news is that both those two factors have a lower overall effect on your credit score. Also, the former has a limited time impact, while the latter can be somewhat mitigated by keeping older accounts open where possible rather than closing them.

The factors that have a greater impact on your credit score—payment history and credit utilization—benefit from you having more credit cards provided you make payments on time and don’t have high utilization.

Other things to consider

We’ve focused so far on the effect that opening many new credit cards can have on your credit score. Your main reason for caring about that will likely be that your credit score affects your ability to get further lines of credit. As a result, there are some other things to consider before going on a credit card application spree.

Business credit cards

Most banks don’t report business cards to your credit report (Capital One is a notable exception, but only for some of its business cards). That means that new business credit cards don’t affect your payment history (provided you make the minimum payment at the very least each month) nor your overall credit utilization. While that means business cards won’t help your scores from that perspective, they also won’t have a negative impact on the average age of your accounts.

5/24 rule & similar bank rules

Even if you’re new to points and miles, there’s a good chance that you’ve heard of Chase’s 5/24 rule:

To determine your 5/24 status, see: Easy ways to count your 5/24 status. The easiest option is to track all of your cards for free with Travel Freely.

That means that even if you have an otherwise excellent credit score of 800+, it’s unlikely that you’ll be able to earn a welcome bonus on a new Chase credit card if five or more new credit cards have shown up on your credit report in the last 24 months.

Some other banks have their own rules akin to Chase’s 5/24 rule, although they aren’t always hard and fast. For example, it can be very tricky—but not impossible—to be approved for a new Bank of America credit card if you’ve opened three or more cards in the preceding 12 months. If you have deposit accounts with Bank of America, that rule is improved to seven or more cards in the past 12 months.

Even if a bank doesn’t have any specific rules about how many new cards you can have opened in the last x months, they might balk at the sight of many new credit cards on your report in the space of a short amount of time. You might therefore find yourself getting declined for new cards at times; if so, it can make sense to cool off on applications for new personal cards for a little while to reduce the impact all those hard inquiries and new accounts are having on your approval odds, even if those factors haven’t had an enormous effect on your credit score itself.

Mortgage applications

If you’re planning on applying for a mortgage, it’s often recommended that you don’t apply for any new credit cards in the two or three months leading up to closing. That’s because even though opening new credit cards can have a positive effect on your long term credit score, you’re more likely to see a drop in the short term due to the hard inquiry.

The mortgage interest rate you’re offered can be affected by your credit score, so even a drop of five points from a hard inquiry could potentially increase your mortgage interest rate. Over the course of the lifetime of your mortgage, that could lead to you paying thousands—or even tens of thousands—of dollars more in interest, so those new credit cards could come at an extreme cost.

Annual fees

Unless you’re solely applying for cards that have no annual fee or no annual fee in the first year, if you apply for many different credit cards over time, you’ll inevitably end up having numerous cards that carry an annual fee.

Those annual fees mount up, especially if you have even just one ultra premium credit card with an annual fee of $795+; depending on how many cards you have in your portfolio, you could end up paying thousands of bucks in annual fees each year.

If you’re certain that you’ll be getting value out of those cards that exceed the annual fees you’re paying, then great. Just be sure that you’re valuing those benefit appropriately and weigh up if it’s truly worth prepaying for all those benefits.

Here are a couple of posts that explore that concept in greater detail:

Question

What’s your experience with this? Have you found your credit score increasing over time the more credit cards you get? Let us know in the comments.

")

Steven, I neglected to mention that this post is really valuable. It’s just another reason I value FM so highly. You guys (including Carrie, of course) really are customer-centric. FM is the only travel email that I filter into my Gmail “Important and Unread”.

And Nick is simply hilarious.

Thank you!

You rarely discuss Amex’s policy of denying signup bonuses. I don’t understand the business justification for this policy. If I’m applying for the Delta Gold card, for example, that’s an indication that I want to fly Delta and I want to spend money on a card that results in revenue to Amex. If I want to open a Schwab Plat card, it obviously means that I do business with Amex’s partner Schwab, etc. The result of these denials is I’ll continue to use Citi and Chase cards and fly American and United. Makes no sense to me and it’s a slap in the face to me as a long-time (30+ year) Amex customer. Our credit profiles are very similar to YoniPDX in this thread.

Is there any appeal/reconsideration process for these denials? Amex executive customer svc?

Popup prison—where Amex states that you’re not eligible for a welcome bonus—is a tricky one because there’s no knowing the criteria behind why it’s being declined.

Sometimes it’s simply because you already have/have had the card. Other times though, there’s no knowing. I’ve been able to get the Hilton Business card before, but my wife has been declined every time she’s applied. Some people get declined for a card when applying using a referral link, but then get approved if they use a direct link.

Other times people are declined possibly due to their previous cardholder experience of opening a card and closing it after a year. Other times, it seems like Amex might like to see you put more spend on a card.

It’s all seemingly random, although there presumably is some kind of method/algorithm in their madness.

We currently have a 57 total open cards and even more cards opened/closed over the past Decade+. Our pace has slowed as fewer cards available with SUBs that are interesting – we both have recenty churned AA/CSP(100K).

That said last fall we got a HELOC always nice to have on hand- esp when traveling – some Int’l hospitals want money up front (our KP insurance covers us globally – but thru reimbursement) so having easy access to low intrest liquid funds makes sense for us.

I digress P2s EQ FICO was 849/850 I was 847/850. We have opend a few cards since but typically we have been in 830±/850 on EQ/TU/EXP on FICO 8 MODELS

We tend to be at 3%-4% credit useage month to month (rolling statement balances).

RE: Insurance credit is more concerned about high credit useage (more likely to file a claim than those with low credit useage) they don’t carry about number of cards.

I think Credit Karma or WalletHub offer(ed) Insurance scores .

Current: you won’t be approved if you are over 5/24.

Suggested: you won’t be approved if you are at or over 5/24.

Good point – I’ve updated that.

I had one car insurance guy tell me that my many credit cards was causing my car insurance to be higher than it would be otherwise.

I wonder if they are confusing number of credits cards with credit card debt. There is something called a credit based insurance score that is a little different than your regular credit score, but the factors in its calculation appear to be very similar. I wouldn’t think number of credit cards by themselves would be an issue although new credit could (similar to regular credit score).

Closed cards continue to age on your credit report for 10 years after closing, contributing to AAoA.

Thank you – I’d somehow missed that that was the case. I’ve updated the post to fix that.

I’m a medium level player (maybe 20 or so open cards). I don’t check often, but I recently did and had an 850 score on Experian.