NOTICE: This post references card features that have changed, expired, or are not currently available

Ever since I documented how to get 5X points pretty much anywhere using a Chase Ink Bold credit card (see “One card to rule them all”), I’ve been asked many times how many Prepaid Amex cards each person can have. Confusingly, I have two answers:

FAQ Answer

According to the Amex FAQ, you can order 3, but only have 1 in your name:

An adult over the age of 18 may order and manage up to three American Express Prepaid Cards in total (including if one is purchased for him/herself). Each American Express Prepaid Card User can have only one Card in his or her name.

Live Answer

Before I read the FAQ shown above, I ordered a second prepaid card for myself. It arrived without any trouble. Once I received the card, I called to make sure I wasn’t doing anything wrong. The Amex rep assured me that each person can have up to 3 for themselves. Since then, I’ve happily used two cards in my name without any trouble. It is worth mentioning though that one card lists my name as “Greg” whereas the other lists my name as “Gregory”. I did that, not to trick Amex, but to have a way to differentiate between the two cards.

So, I don’t know which of the above answers is really right. Have you tried ordering more than one for yourself? What has your experience been?

Order online for free

Here’s my referral link to signup for a free prepaid card: American Express® Prepaid Card

| Chase's 5/24 Rule: With most Chase credit cards, Chase will not approve your application if you have opened 5 or more cards with any bank in the past 24 months. To determine your 5/24 status, see: 3 Easy Ways to Count Your 5/24 Status. The easiest option is to track all of your cards for free with Travel Freely. |

| Chase 5/24 semantics ("Subject to" vs. "Count towards"): Most Chase cards are subject to the 5/24 rule. That means the rule is enforced in making approval decisions. In other words, you probably won't get approved if your credit report shows that you opened 5 or more cards in the past 24 months. Meanwhile, most business cards (such as those from Chase, Amex, Barclaycard, BOA, Citi, US Bank, and Wells Fargo) are not reported on your personal credit report. These cards do not count towards 5/24. Example: Chase Ink Business Preferred is subject to 5/24, so you likely won't get approved if over 5/24. If you do get approved, it won't count towards 5/24 since it won't appear as an account on your credit report. |

| Amex credit and charge card limits: If you apply for a new Amex credit card, you may get turned down if you already have 5 or more Amex credit cards; or 10 or more Pay Over Time (AKA charge) cards. Both personal and business cards are counted together towards these limits. Authorized user cards are not counted. See also: Which Amex Cards are Charge Cards vs. Credit Cards? |

| Applying for Business Credit Cards Yes, you have a business: In order to sign up for a business credit card, you must have a business. That said, it's common for people to have businesses without realizing it. If you sell items at a yard sale, or on eBay, for example, then you have a business. Similar examples include: consulting, writing (e.g. blog authorship, planning your first novel, etc.), handyman services, owning rental property, renting on airbnb, driving for Uber or Lyft, etc. In any of these cases, your business is considered a Sole Proprietorship unless you form a corporation of some sort. When you apply for a business credit card as a sole proprietor, you can use your own name as your business name, use your own address and phone as the business' address and phone, and your social security number as the business' Tax ID / EIN. Alternatively, you can get a proper Tax ID / EIN from the IRS for free, in about a minute, through this website. Is it OK to use business cards for personal expenses? Anecdotally, almost everyone I know uses business cards for personal expenses. That said, the terms in most business card applications state that you should use the card only for business use. Also, some consumer credit card protections do not apply to business cards. My advice: don't use the card for personal expenses if you're not comfortable doing so. |

| Manufacturing Spend Caution: Many, many things can go wrong when manufacturing spend. If you suddenly increase credit card spend, your accounts may get shut down. If you cycle your balance often (e.g. spend to your limit, pay the bill, repeat) within a billing cycle, your accounts may get shut down. If you repeatedly pay your credit card bill from an anonymous bill payment source, your accounts may get shut down. If you buy lots of gift cards you may lose money due to gift card fraud, theft, loss, or simply mishandling those gift cards (e.g. maybe you thought you already used a gift card and tossed it into your “used” bin). If you rely on only one method to liquidate gift cards, you may be stuck unable to pay your credit card bill when that method gets shut down. In other words, don’t try this at home unless you know what you’re doing, and you understand and accept the risks.. |

| Chase Ultimate Rewards points are super valuable and super flexible. At the most basic level, points can be redeemed for cash or merchandise, but you'll only get one cent per point value that way. A better option is to use points for travel. When points are used to book travel through the Ultimate Rewards portal, points are worth 1.25 cents each with premium cards (Sapphire Preferred or Ink Business Preferred, for example) or 1.5 cents each with the ultra-premium Sapphire Reserve card. Another great option is to transfer points from a premium or ultra-premium card to an airline or hotel program when high value awards are available (see this post for details). If your points are tied to a no-fee "cash back" Ultimate Rewards card, then first move those points to a premium or ultra-premium card before redeeming them in order to get better value. |

| Amex Membership Rewards points can be incredibly valuable if you know how to use them. In general, if you use Membership Rewards points to pay for merchandise or travel, you won't get good value from your points. One exception is with the Business Platinum card where you'll get a 35% point rebate when using points to book certain flights. This gives you approximately 1.5 cents per point value, which is pretty good. Another exception is with the Business Gold Card where you'll get a 25% point rebate when using points to book certain flights. This gives you approximately 1.33 cents per point value. If you don't have either card, then your best bet is to transfer points to airline miles in order to book high value awards. More details can be found here: Amex Membership Rewards Complete Guide. |

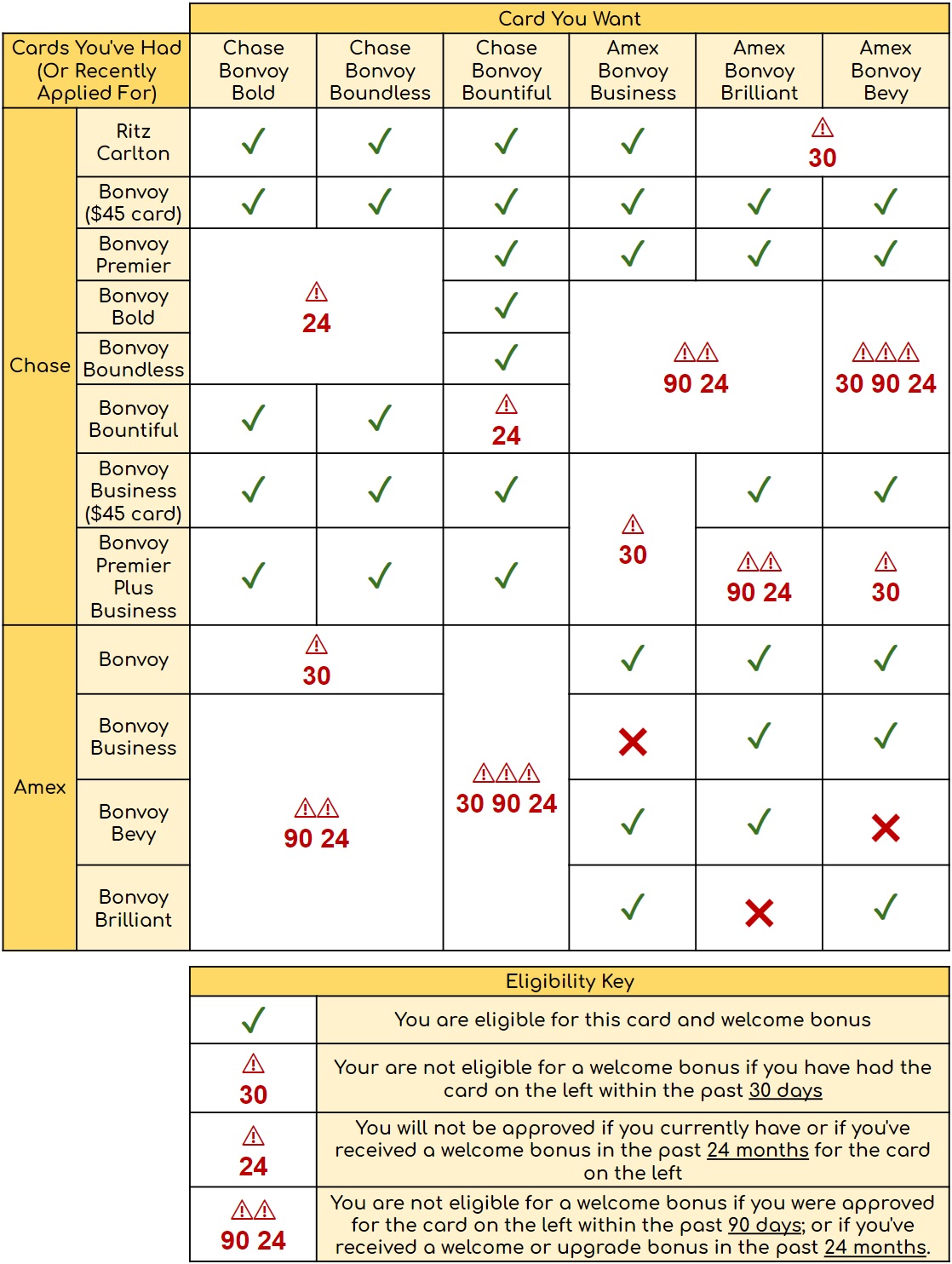

| Marriott points can be redeemed for free night awards, travel packages, airline miles, or experiences. 5th Night Free Awards: When redeeming points for free nights, the 5th night within a single reservation is free. Airline miles: Points can be converted to airline miles at a rate of 3 points to 1 mile. With many programs, a bonus is added on when you transfer 60,000 points at a time, such that 60,000 points transfers to 25,000 miles. Also, you'll get a 10% bonus when transferring points to United Airlines. Everything you need to know about Marriott's rewards program, Bonvoy, can be found here: Marriott Bonvoy Complete Guide |

| Editor’s Note: This guest post was written by the same guy who showed you how to fly round trip to Africa (DC to Senegal) for 50,000 points, how to book business class to Europe for 80,000 miles roundtrip, and more. You can find John’s website and award booking service here: theflyingmustache.com/awardbooking. -Greg The Frequent Miler |

Amex Application Tips

Check application status here. |

Chase Application Tips

Call (888) 338-2586 to check your application status |

Citi Application Tips

Check application status here. |

Bank of America Application Tips

Click here to check your application status |

Barclays Application Tips

Consumer: Click here to check your application status |

Capital One Application Tips

Call (800) 903-9177 to check your application status |

Discover Application Tips

Click here to check your application status |

TD Bank Application Tips

Call (888) 561-8861 to check your application status |

US Bank Application Tips

Call (800) 947-1444 to check your application status. |

Wells Fargo Application Tips

Check application status here. |

Under certain circumstances consumer Visa cards don't work with Plastiq. The following payments are fine:

|

In order to meet minimum spend requirements, people often look for options to increase spend in ways that result in getting their money back. These techniques are referred to as "manufacturing spend". American Express has terms in their welcome offers that exclude some manufactured spend techniques from counting towards the minimum spend requirements for the welcome offer. For example, most new cardmember offers have terms like this:

Eligible purchases to meet the Threshold Amount do NOT include fees or interest charges, purchases of travelers checks, purchases or reloading of prepaid cards, purchases of gift cards, person-to-person payments, or purchases of other cash equivalents.That said, many techniques for meeting minimum spend are perfectly fine. Here are some techniques that are safe for meeting Amex minimum spend requirements (click each link for more information): |

|

| We have added this to our running list of Black Friday deals, which will be constantly updated through Cyber Monday with a mix of gift card deals, merchandise deals, and travel deals. Check back often. |

[…] How many Amex prepaid cards can I have? […]

When you say 3 is the max, what do you mean?

– Is it three of the very same AMEX card e.g. 3 AMEX Prepaid or 3 AMEX target

or

– Is it three prepaid AMEX product, whichever they may be e.g. 2 AMEX for Target and 1 AMEX Prepaid

This could be a big difference.

This post is based on old Amex prepaid cards that are no longer available for new applicants. They didn’t have a name like Bluebird or Serve. They were simply called American Express Prepaid cards. Named cards have specific limits of their own. You can have 2 Target Amex cards. You can only have one Bluebird OR one Serve card.

[…] How many Amex prepaid cards can I have? […]

Does anyone have an idea about how long it will take to get the cards in the mail? I ordered 3 of them June 28th and have had each of the $200 amounts taken out of my bank accounts but have not received any emails about the cards being shipped and only 1 of them shows up online after I set up the account. Just curious if anyone has previous experience with this time frame…

@J

How long have you had your Ink? And approximately how much of your monthly office depot purchases consist of gift cards? I just want to get an idea of how much I can spend in gift cards.

I had obtained 3 of the amex blue prepaid cards last year, well before the ‘one card to rule them all’ strategy was masterfully discovered by FM. I used the same browser, and my same info for all 3 cards and received them, along with 3 $50 gift cards (a promo last year), without a problem. Amex had the promo again at a later date and I tried to apply for another 3 but was denied. It seems like Amex has no problem giving 3 per person.

As far as spending on the IB, i’ve been doing between 2 to 5k per month at office depot. Last year, when I initially was approved for the ink bold, I did get a call from them because my usage was very high (i put maybe 5 or 6k on it in the first few weeks). I basically told them that my spending will be all over the map and that if I ever get denied on that card that I’ll happily use my amex gold biz. I haven’t had an issue since.

Unfortunately, no one (except maybe someone at Chase) knows what is safe and what’s not. Each person needs to figure out the level that is likely to be safe for them, for their situation, and for their risk tolerance. If the fear of getting shut down by Chase is overwhelming you, then don’t do this — extra points aren’t worth losing sleep over.

I’ve been spending $500-$1500 at OD every month with no problems. I always buy odd amounts on the cards so the totals come up just under an even hundred.

I highly doubt Chase cares about this scheme, more than they care about risk, otherwise they would have designed the program differently.

@Sandra

How much did your friend spend at Office Depot every month? And how much did your friend spend in total for the Bold every month?

I’m not sure if it makes sense to really spread around office supply spend…this isn’t realistic. Once you have a preferred vendor, you normally go to one place. Businesses don’t normally have the luxury of shopping around weekly or monthly for the best deals. They just hope to get a negotiated discount based on annual spend.

I think the magical shutdown algorithm involves looking at % of credit limit spent, which goes toward risk of an open account…or maybe there is a negative cost per point (internal for Chase) associated with accounts, and they monitor accounts that are negative for them. Accounts that accrue 20K+ UR pts/month with minimal fees can’t be very profitable for Chase, right?

@ rick,

yes $50k a year at office supplies stores on IB card BUT it is obvious that if the only office store you visit is OD and this is only place office or not where you spend $500 to $2K a month, this get’s their attention.

so unless you spend $500 to $2k a month at staples, officemax too, this maybe their so called ABNORMAL LARGE PURCHASES?

FM, it would be an interesting find to publish more specifics of what really happened when chase shut these accounts down. There is a lot of guessing, heresay, erroneous information, and not full disclosure of the facts/truth as any real evidence. Many people likely don’t want to disclose the exact reasons because of embarrassment, stupid moves, and purely pulling stunts far greater than the norm. Like doing OD at 10k a pop, etc. I’ve not read a single report with full disclosure nor any where when the OP was hard pressed for more accountability that they didn’t go silent and never address the questions. Others simply claimed ‘innocent’ behavior. Yeah right.

Sandra, your ink bold does have a CL, you are just not aware of it. Even though chase assigns this as a charge card and you can charge what you wish, they do have a CL associated with it in the background. You have to ask chase for it, it’s not disclosed like on your credit accts. I found this out as I moved some CL on the biz side around for a new acct opening. My ink old is at 48k and the new is at 30k.

Doh, I’m sufficiently worried now…how much is too much OD spend on an IB every month? $4-5K?

Because stock has been low at my OD, I feel the need to purchase more reloads. Maybe if I just buy 1 reload at a time?

my IB doesn’t have CL but I pay down my credit card bills every 2 weeks small or large and I don’t wait till the due date to pay my card balances.

all my cards have credit utilization ratio of only 1%.

Yes, becareful with the OD thing