Update 4/23: The Barclays-to-Citi transition will begin tonight at midnight. You won’t be able to access your AA Barclays accounts after that point, and you won’t be able to open a new Citi account until 4/27 (if Citi’s dates are accurate).

It’s worth taking a screenshot of any companion certificate numbers you currently have in your Barclays account, as well as any other info you want to be able to verify post-transition.

Note that any autopay or future payments scheduled after 4/24 will be canceled. Don’t forget to reschedule those once the Citi card goes live, and/or initiate a payment now if it’s due on 4/25 or 4/26.

~~~

We now have a clearer picture of the details regarding the transition of Barclays Aviator and Aviator Silver cardholders to Citi accounts. The accounts will move to Citi in April 2026, and Barclays cardholders will get a bit of a “best of both worlds” by keeping both legacy and new benefits.

There are many granular details we don’t yet know, but it is worth understanding the finer points. More details have been announced for Aviator Silver cardholders. Those cardholders will keep the same annual fee ($199) and keep the ability to earn up to 15K Loyalty Points at least until Feb 28, 2027. Click here to jump to the detailed update.

![]()

High-level details of the Barclays -> Citi transition

Barclays Aviator cardholders recently received word from Citi outlining coming changes to their cardmembership. Key details include:

April 24, 2026, the bank that issues your AAdvantage® credit card is changing from Barclays Bank Delaware to Citibank, N.A. (Citi)

- Continue to use existing card after April 24.

- Citi card will be sent within 6-8 weeks beginning April 27, 2026

- Your cardmember anniversary date will remain the same.

- If your account has an annual fee, it will be assessed on or after your next anniversary date.

- Your existing credit limit will stay the same at the time of transfer. Over time, we may review your account as part of our standard practices.

- You can keep enjoying the legacy Barclays benefits for a limited period of time

In short, you’ll get a Citi card sometime after April 24th, and you’ll get access to some new benefits on the Citi side, while also keeping some of your legacy benefits for some unknown amount of time.

I’ll dig into legacy vs new benefits in a moment, but it is worth calling out that the email and associated documentation from Citi made no mention at all of the annual fee apart from the fact that it will be assessed on your next anniversary date. It is not at all clear whether the fee may increase or when that will happen.

Digging into the details of the transition

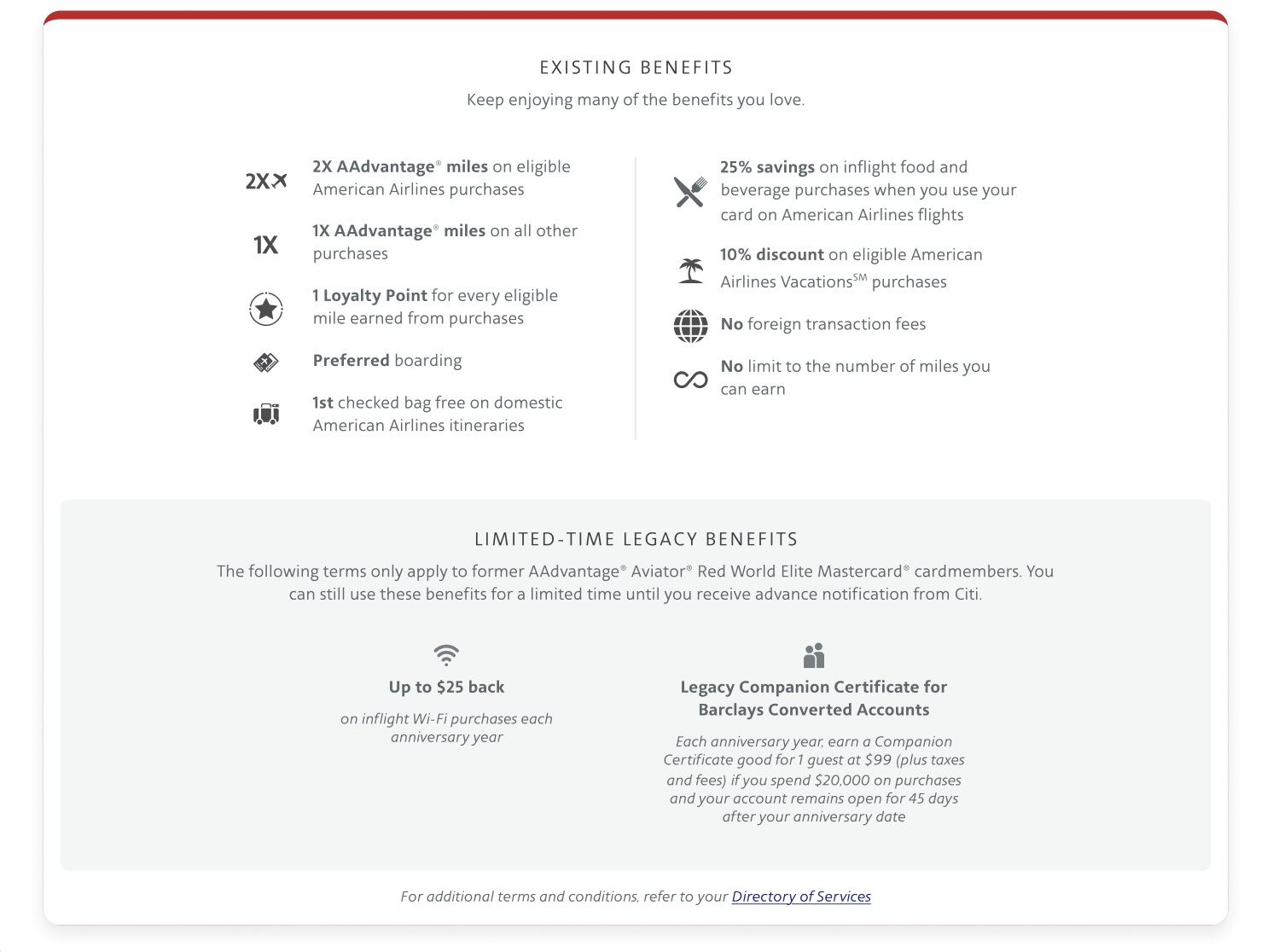

Barclays AAdvantage® Aviator® World Elite Mastercard® to American Airlines AAdvantage® MileUp® Card

Link to details from Citi about this transition

The following chart shows the high-level details of these two cards, with key differences underlined.

| Card | Annual Fee | Category Bonuses | Key Benefits |

|---|---|---|---|

| Citi AAdvantage Mile Up | $0 | 2X AA, Grocery Stores | 25% savings on in-flight food & beverage |

| Barclays AAdvantage Aviator World Elite Mastercard (Aviator “White”) | $0 | N/A | 25% savings on in-flight food & beverage |

The Aviator “White” as it was sometimes known was a no-annual-fee downgrade option (I don’t believe it ever existed for new applicants). Those with the Aviator White will transition to the Citi AAdvantage Mile Up card, picking up 2X on American Airlines and at grocery stores. Keep in mind that the AA cards only earn 1 Loyalty Point per dollar spent (even in bonus categories). That said, the Mile Up is probably a slight upgrade for most cardholders.

Barclays AAdvantage® Aviator® Red to Citi AAdvantage Platinum Select transition

Link to details from Citi about the transition

The following table lists the core benefits of the Citi AAdvantage Platinum Select card and the Barclays AAdvantage Aviator Red card. Note: Those benefits that are underlined are unique to the respective card.

| Card | Annual Fee | Category Bonuses | Key Benefits |

|---|---|---|---|

| Citi AAdvantage Platinum Select | $99 | 2X AA, Gas, Dining | $125 AA Flight Discount with $20K membership year spend |

| Barclays AAdvantage Aviator Red | $99 | 2X AA | $99 + tax domestic companion certificate after $20K membership year spend; $25 annual inflight Wifi Credit; |

As you can see in the chart, the Barclays Aviator red will pick up a couple new category bonuses, with 2x gas and dining, when the card transitions to Citi. Note also that the Barclays card and the Citi card both offer benefits after $20,000 in purchases in a membership year, though the type of benefit is different.

The good news is that the documentation from Citi indicates that existing Aviator Red cardholders will hang onto legacy benefits “for a limited time”, until they receive advance notification from Citi.

We don’t yet know exactly how this will work in practice. Will it be possible to earn both the Companion Certificate and the $125 flight discount? We expect that it likely will be possible to earn both for some time (until Citi provides advance notice otherwise), but will spend that a cardholder has completed before the transition count for the Citi flight discount benefit, or will they only count spend from the time the card becomes a Citi card? What about those who have partially completed spending toward this year’s Barclays Companion Certificate? Will that spend carry over?

We don’t yet know the answers to those questions. My best guess is that spend completed since last anniversary will continue to count, even if that spend was completed before the card moves to Citi.

Note that the Citi Platinum Select also offers the ability to earn up to $30 in statement credits for each eligible Turo trip completed from April 24, 2026 to October 18, 2026.

Barclays AAdvantage® Aviator® Silver to Citi® / AAdvantage® Globe™️ card

Link to details from Citi about the transition

This transition is perhaps the one with the most potential to win or lose.

As we covered on a podcast episode last year, at a very high level, the Citi AA Globe card has similarish benefits to the Aviator Silver card. As you dig into the details, the benefits of the two cards (and their ongoing annual fees) differ significantly.

Here is a chart showing the key details, with key differences between the cards underlined.

| Card | Annual Fee | Category Bonuses | Key Benefits |

|---|---|---|---|

| Barclays AAdvantage Aviator Silver | $199 | 3X AA, 2X Hotel, Car rental | $25 per day inflight food and beverage credit; $50 annual inflight Wifi credit; $99 Companion certificate good for 2 guests after $20K membership year spend. Up to 15K bonus Loyalty Points: 5K at $20K spend, 5K at $40K spend, and 5K at $50K spend during the status qualification period; $100 Global Entry application fee credit |

| Globe | $350 | 6X at AA Hotels ✦ 3X American Airlines purchases ✦ 2X restaurants ✦ 1X everywgere else | Four Admirals Club Globe passes per year Up to 15,000 additional AAdvantage Loyalty Points per year: Earn 5,000 bonus Loyalty Points after every four qualifying American flights, for up to 15,000 bonus Loyalty Points each status qualification year ✦ $99 Companion Certificate starting in your second year after card renewal, valid for a single round-trip domestic economy trip each year $100 in statement credits for in-flight purchases per calendar year ✦ Up to $100 Splurge credit per calendar year: (choose up to two): AAdvantage Hotels bookings, 1stDibs, Future Personal Training, and Live Nation ✦ Up to $240 annual Turo credit (up to $30 in statement credits for each eligible completed trip on Turo, up to $240 per year) |

It is interesting that benefits will apparently overlap for at least some period of time. For instance, we expect that existing Aviator Silver cardholders will receive the Admirals Club passes and splurge credits after the cards transition in April. It also sounds like it will be possible, for at least a limited time, to earn both the spend-based Loyalty Point bonuses from the Barclays card and the bonus Loyalty Points offered by the Globe card based on flight activity. That could make it far easier to qualify for elite status for those who can manage to meet both sets of requirements.

We wonder whether transitioned cardholders will receive both the Globe card’s automatic $99 Companion Certificate at renewal and the Aviator Silver card’s Companion Certificate, which is valid for two companions, if they have met the $20K spending requirement. As things stand, we expect that it should be possible to get both. It is also worth noting that while those benefits sound similar, in practice, Citi companion certificates have carried fewer restrictions than Barclays certificates, including being valid on a wider range of fares and not subject to Barclays’ blackout dates.

The big question, of course, is whether and when existing Aviator Silver cardholders will be subject to the Globe card’s $350 annual fee. As with the Aviator Red card information, it is interesting and probably notable that Citi has made no mention at all of the annual fee apart from noting that one will be assessed at renewal.

As an educated guess, I would suspect that Citi probably needs to provide advance notice of an increase in the annual fee. Furthermore, since many existing Barclays Aviator Silver cardholders have presumably already made progress toward the companion certificate, and that certificate is contingent upon renewal, it would be at least customer-unfriendly to move the goalposts by increasing the required renewal fee. It may be that there are regulatory considerations there also. I think it’s possible that Aviator Silver cardholders could keep the $199 annual fee at the next renewal, at least for near-term renewals. However, that is only a guess. Time will tell how that shakes out.

Update 3/11/26

Citi has advised the following:

Certain benefits tied to your existing AAdvantage® Aviator® Silver World Elite Mastercard® will continue for a limited time. You will be notified in advance of any changes to these benefits. You’re still eligible to earn up to 15,000 additional Loyalty Points during the status qualification period through February 28, 2027.

As you can see, the ability to earn up to 15,000 additional Loyalty Points through spend will continue until at least the end of the current elite qualification year. There’s certainly a chance they’ll extend this card feature beyond then, but it’s more likely they’ll notify existing cardholders later this year or very early next year that the benefit will be going away.

Barclays AAdvantage® Aviator® World Elite Business Mastercard® to Citi® / AAdvantage Business™ Card

Link to a document from Citi with transition details

The following chart outlines the key details of these two cards, with those features unique to one card or another underlined.

| Card | Annual Fee | Category Bonuses | Key Benefits |

|---|---|---|---|

| Barclays AAdvantage Aviator Business | $95 | 2X AA, office supply, telecommunications services, and at car rental agencies | First checked bag free ✦ Preferred boarding ✦ 5% bonus on miles earned the previous year after AF is paid ✦ 25% statement credit on in-flight purchases |

| Citi® / AAdvantage Business™ World Elite Mastercard® | $99 | 2X AA ✦ 2X certain telecommunications merchants ✦ 2X car rental merchants ✦ 2X gas | First checked bag free ✦ Priority Boarding ✦ Save 25% on inflight purchases |

As is the case with all of the other cards, the Citibusiness AA card is keeping legacy benefits “for a limited time”.

Of particular interest here is that both versions of this card include a Companion Certificate after $30,000 in purchases in a cardmember year and renewal of the card. However, that benefit is listed both under new card benefits in the Citi document and under legacy card benefits.

Maybe that’s just a coincidence. On the other hand, is it possible that this card will earn both certificates for those who meet the spend?

That probably won’t happen. However, I can’t count it out entirely. Barclays Companion Certificates have historically come with a host of blackout dates and a list of eligible fare classes. Citi-issued Companion Certificates have not had blackout dates and have been applicable to a wider range of fare classes. It is possible that these are being treated as different benefits because of those differences in the features of the product. I definitely wouldn’t count on earning both, but neither will I be caught completely off guard if that happens for those who meet the spend and keep the card through the next renewal.

Should you keep your Barclays card or cancel it before the transition?

In short, I think it won’t make much sense to cancel before the transition in most cases.

That’s because existing cardholders will get a combination of legacy and new benefits that will add some amount of value in most cases without adding any immediate measurable cost. Even if the annual fee ultimately increases on the converted Aviator Silver cards, it wouldn’t happen until at least next renewal (and maybe later).

We don’t believe that having a converted card will preclude anyone from getting a new card bonus on another Citi AA card with regard to welcome bonus restrictions. Here are the pertinent sections of the terms for the AAdvantage Platinum Select card and the Globe card with regard to eligibility for a new cardmember bonus:

*AAdvantage Platinum Select terms: “American Airlines AAdvantage® new cardmember bonus offer not available if you received a new account bonus for or if you converted another Citi credit card account on which you earned a new account bonus into a Citi® / AAdvantage® Platinum Select® account in the last 48 months.”

Citi AAdvantage Globe terms: “American Airlines AAdvantage® new cardmember bonus offer not available if you have received a new account bonus for or converted another Citi credit card account to a Citi® / AAdvantage® Globe™ account in the past 48 months.”

As we read that, you should be eligible for either new card bonus so long as you haven’t received a new cardmember bonus on that specific card or converted another Citi credit card account to it within the past 48 months. Since this is a conversion from Barclays, we don’t expect it will prevent you from getting a new cardmember bonus on the same card in the future.

Among the biggest potential disadvantages to allowing your Barclays card to convert is the fact that it is possible that the Citi card will be reported as a new account, increasing your 5/24 count. To be clear, we don’t know that will happen — it certainly may be that the account carries over your existing history and does not cause a new account to be added.

The other key disadvantage to allowing conversion is that it will add to your total exposure with Citi. If, for example, you have a large Barclays credit line that gets moved to Citi, you could reach your maximum exposure with Citi in terms of the credit they are willing to extend to you. That could make it harder to get approved for another new Citi account in the future.

However, we think that the advantages of allowing the conversion to proceed likely outweigh the disadvantages for most folks.

For starters, you’ll get access to both sets of benefits for at least a while. There is also the chance that existing Aviator Silver cardholders get grandfathered into the lower annual fee and legacy benefits for longer than expected. Stacking Loyalty Point bonuses could be useful for those chasing elite status. And, even if you ultimately do not want a Citi AA card, it should be possible to product change down the line.

In my own household, my wife is an Aviator Silver cardholder and probably won’t keep the Globe card long-term. However, she will gladly use the splurge credit, and it is possible that the Admirals Club passes and in-flight purchase credits could come in handy (note that the Aviator Silver will continue to offer up to $25 per day in statement credits for in-flight purchases, but maybe that will stack with the new $100 statement credit offer). However, in the long run, she will look to product change. She currently has a Citi Double Cash card with a relatively low limit. The limit on her Aviator Silver card is significantly higher. She’s probably going to request a credit limit increase from Barclays and hope to product change the resulting Globe card to a Double Cash card with a more useful limit down the line. Then, she could downgrade her existing Double Cash to a Custom Cash card. If we get data points of the automatic companion certificate posting and people renewing and $199, maybe she’ll keep the Globe card for another year before product changing. We’ll keep options open.

I don’t see enough upside in cancelling before transition in most cases, though there will be some fringe cases where cardholders decide that they don’t want to be transitioned to Citi for one reason or another. I expect those to be the minority of cases here, at least until next renewal on these cards.

American Airlines shopping portal promo: Earn up to 2000 bonus miles")

Haha unlike some commenters below I understand that this is the best points/miles website of all and not the actual Citibank website! My Aviator to Citi experience has been bizarre. I did not want my Red to go to Plat Select because I feared it would add to my 5/24 and maybe mess with bonus eligibility so I cancelled the Red on 4/23/26 and got confirmation that it was closed: it was removed from Barclays login and got cancel confirmation letter in mail. However, I just received from Citi a $0 paper statement in the mail of a Plat Select card with last 4 digits of card (I don’t have another Plat Select and never got that card). That seems like pretty clear evidence that Citi still opened a new account since there are those 4 digits. However, I don’t see the account in any of my credit reports and no new Citi inquiries. Should I call Citi? The best case scenario would be a new account that did not add to my 5/24 and did not have an inquiry, that I could eventually product change to a Custom Cash (or at least ATT which may become a Custom Cash later). But I don’t want to call Citi and have them somehow “activate” this ghost Plat Select (which doesn’t show up in my Citi login – I have a Strata Elite – and no box to add a new Citi card), which will then result in it adding to my 5/24. Anyone please help?!?!

Is it absolutely certain that the bonus 15K miles you can achieve through spend is valid on the CITI Globe that replaces the Barclays Silver?

@Nick Reyes – I just received a Citi AAdvantage Business MC in the mail as a replacement for my old AAviator Business MC. I already have one Citi AAdvantage Business MC (or maybe two, need to check the sock drawer), I certainly don’t need another one. Are there any Citi cards I can Product Change this to, or is my only way to make it useful and/or avoid the AF to simply close the thing and shred it?

So Citi has been pushing updates in regards to the new cards to Amazon, Apple Pay, Google Pay ect.. However there is now a delay on issuing the new cards. Ours was supposed to ship May 5th and still hasn’t been mailed. Unfortunately the new card is not activated and now payments are being declined by the above listed. Citi’s customer service suggested deleting the card and re-entering the old Barclay information until the new cards arrive and are activated.

I want to make a payment for an item that wa on my Barlays account to new Citi acct. What is my new Citi CC number and billing address?

This isn’t a Citi or Barclays website, so we don’t have any insight into your account. You’ll want to contact Citi directly.

I will add to what Tim said that you should be able to easily either add your card to your existing Citi login or create a new Citi login by clicking the banner at the top of the Citi home page for Barclays Aviator card holders and entering your Barclays card information to create a Citi Online login. You don’t need to have received the Citi version of the physical card to create your Citi login. Then you should be able to simply pay through Citi.

I tried this an if did not work – no way to make my payment – pretty amatuerish

How are we able to pay our balance if we do not have our card

I can not see my charges please respond

Very concerning last four didgets 5491

This isn’t a Citi or Barclays website, so we don’t have any insight into your account. You’ll want to contact Citi directly.

How can I pay my credit card that I don’t have and is due 05/03/26

and I do not want any late fees or bad credit score

You just create a login at Citi using your Barclays card number. There’s a link right on the Citi home page to create an account using your barclays card info: https://citicards.citi.com/usc/Digital-Welcome-Kit/WYNTK/Default.htm

that did not work for me.. tried 3 times

I am trying to do that too! I can’t find a phone number in any of the correspondence that they sent!!

They moved our existing Barclays balance this weekend to Citi, but there is no way to pay it off because you can’t register for a Citi online account until you have your new card. That means that your balance could be sitting at Citi for up to 8 weeks! This is extremely concerning.

You don’t need the new card to register for a Citi account. You can register for a Citi account with your existing Barclays Aviator card number. It says so in the messaging on the Citi website, and I did that. I was able to create a login and set up a payment method without the new card.

Is it necessary to create a new login? Or can the Barclays card number be added directly to existing Citi logins?

I just added it to my existing Citi login.

Did you have any issues? it is telling me my info is incorrect. The card is in my hand, so I know it isn’t incorrect.

My citi account shows my new globe card. Now under benefits, I see $100/year for inflight credits but nothing about the $25/day. Is that perk still available?

I believe it is still available for now. I expect that Citi’s benefits page will only show you the benefits that all Globe cardholders get, not the extra benefits you get due to having had the old Aviator Silver card

I need to download my transaction from jan1 to present but it is no longer available through barclay sign in. Where do i go to review and download. Also, I don’t see how I can schedule my payment for the 5th. Does anybody have the web address for this??

I woke up this morning and my Barclay’s AA cards (the Red and the no-AF card) are gone from my account login. I only see my Wyndham Biz card. Anyone know how to see old Barclay’s statements/transactions? I have not dug around too much yet because I am supposed to be working.

And I have no (obvious) indication in my Citi account that I have two new cards.

Cancelled my Aviator Red yesterday so as not to risk increasing my 5/24, exclusion from SUB on Platinum Select, and not being able to product change to Custom Cash. Citi made a mistake here by not informing the credit card community of what the conversion would entail and made me rethink my whole strategy. I was thinking about moving to Strata Premier and 3 Custom Cash but now especially with point sharing ending I don’t think I will move to this and I don’t even know if Citi will let me product change to the Custom Cash. And AA has a great loyalty program, but terrible flight experience. Twice in last three flights we had to deplane due to last minute maintenance issues.

Update: Even though I cancelled well before the transition date 4/27, it appears that Citi forced me to have an AA card that I did not want mailing me a statement (but not the actual card) with the last 4 of the card # and a tiny credit limit. I wanted to keep eligibility for the Platinum bonus and not add to 5/24 (Happy 5/24 day btw!). What should I do?

My Barclay AA card got converted to a Barclay Juniper card. Not sure what benefits that card has

I have had Aviator since right before it was discontinued in Sept 2025. Received email months back it would become a Citi card. Then end of March same message with dates. In April, I got notice it would become a Barclays Arrival card. Low and behold, it shows as Barclays Arrival in Barclays app, don’t think I’m getting Citi after all. I have no idea what happened. P2 from beginning was listed to get Barclays variant and she did.

I have seen some other reports with the same switcheroo. Perhaps Citi decided they didn’t want you as a customer? Do you already have a Citi AA card?

I’m in the exact same situation. I also received a new Arrival card which I haven’t activated yet.

I’m taking a wait and see approach.

I seem to recall that Citi would start mailing new cards after 4/27, so hopefully a new Citi card will show up in my mailbox.

I suppose I could also make some test purchases after the transition with my AA Aviator card and see if they post to my Barclays account under the Arrival card.

One week to go and getting worried. I got approved for the Aviator Red in October 2023. Even if it DOES add to 5/24, will it not matter for me and correctly show the account open date or will the 5/24 clock reset to zero on conversion? This would be my worst case scenario because it would stay on my report for a full 24 months. I am torn because Nick’s article leans towards not canceling and I eventually want a Custom Cash without opening a new one but I will probably want a Hyatt premium card and I am already at 5/24 now. I also never got a bonus on a Platinum Select. What would you do? I should add that I don’t need any of the benefits or rewards of the Platinum Select since I have the Biz AAdvantage which overlaps.