NOTICE: This post references card features that have changed, expired, or are not currently available

Our government recently approved an economic stimulus bill to fight the Coronavirus caused recession. Among its provisions are cash payments to be sent directly to individuals. Most adults earning less than $75,000 can expect $1,200 plus $500 per child.

This post is for those who don’t qualify for a stimulus check or simply would like even more money. The stimulus check I’m proposing here is funded by big banks rather than the federal government…

Regular readers of this blog already know how this works. The basic idea is simple: sign up for credit cards that offer huge welcome bonuses, meet minimum spend requirements, and then cash in your rewards. Next year, when annual fees come due, you can cancel or downgrade to avoid new annual fees. In this post I’ll guide you step by step through this process…

Do you have a business? (Yes!)

Please don’t brush past this section assuming that the answer is “no”. The best credit card offers are almost always for business cards. And yes, in order to sign up for a business credit card, you must have a business. That said, it’s common for people to have businesses without realizing it.

If you sell items (or plan to sell items) at a yard sale, or on eBay, for example, then you have a business. If you make music, art, or poetry and hope to profit from your work, you have a business. Similar examples include: consulting, writing (e.g. blog authorship, planning your first novel, etc.), handyman services, owning rental property, renting on airbnb, driving for Uber or Lyft, etc.

Select the best offers

Credit card offers change all the time. You can always find the latest and greatest offers on our Best Credit Card Offers page. Or, if you’re only interested in cash back, check here: Best cash back credit card offers. Note that we always publish the best public offers even if that means that we lose out on earning referral revenue. We firmly believe in publishing what’s best for our readers even if it means less revenue for this business.

Best business cash back offers

As I write this, the overall best credit card offer is for the Chase Ink Business Preferred Card. The current offer is for 100,000 points (worth at least $1,000), but it requires massive spend: $15,000 in 3 months. Fortunately, we currently list an alternate offer for 80,000 points (worth at least $800) after $5,000 spend.

| Card Offer and Details |

|---|

ⓘ $1277 1st Yr Value EstimateClick to learn about first year value estimates 100K points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer 100K after $8K spend in the first 3 months$95 Annual Fee Recent better offer: 120K after $8K spend (expired 9/4/24) FM Mini Review: Great card for welcome offer and 3X categories. Also consider the Ink Business Cash for its 5X categories, and the Ink Business Unlimited to earn 1.5X everywhere. Earning rate: 3X travel, shipping, internet, cable, phone, and advertising with social media sites (up to $150K spend per year) ✦ 5X Lyft through September 2027 Card Info: Visa Signature Business issued by Chase. This card has no foreign currency conversion fees. Noteworthy perks: Points worth up to 75% more when redeemed for travel with Points Boosts ✦ Transfer points to airline & hotel partners ✦ Cell phone protection against theft or damage See also: Chase Ultimate Rewards Complete Guide |

Another fantastic offer is for the U.S. Bank Business Leverage® Visa Signature® Card. Currently, US Bank is offering $750 after $7,500 spend in 4 months. That’s a lot of spend, but stick with me as I’ll show you later in this post how to achieve it.

| Card Offer and Details |

|---|

ⓘ $474 1st Yr Value EstimateClick to learn about first year value estimates 60K Points Non-AffiliateThis is NOT an affiliate offer. We always present the best offer even when it means less revenue for Frequent Miler 60K points (worth $600 as a statement credit or deposit into eligible account) after $6K spend on the account owner's card in first 120 days$0 introductory annual fee for the first year, then $95 Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Recent better offer: 75K (worth $750 as a statement credit or deposit into eligible account) after $7,500 spend in first 120 days (Expired 4/11/26) FM Mini Review: Since the points are worth 1c each, this card isn't terribly rewarding for ongoing spend. Note that points can not be combined with the Altitude Reserve. Earning rate: 2x on top two categories where you spend the most each month Base: 1% Card Info: Visa Signature Business issued by USB. This card has no foreign currency conversion fees. Noteworthy perks: Earn 2x in the two categories in which you spend the most each month. Full list of categories can be found here. |

Other current business card offers worth considering include two other Chase Ink cards: Ink Business Unlimited and Ink Business Cash. Each offers 50,000 points (worth at least $500) after $3,000 spend:

| Card Offer and Details |

|---|

ⓘ $1074 1st Yr Value EstimateClick to learn about first year value estimates $750 cash back* ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer $750 (*awarded as 75,000 points) after $6k spend in the first 3 months.No Annual Fee Recent better offer: $900 (*awarded as 90,000 points) after $6k spend in the first 3 months. (Expired 11/13/25) FM Mini Review: Great welcome offer for a no annual fee card. Good option for earning 1.5X everywhere. Good companion card to Ink Business Preferred, Sapphire Reserve or Sapphire Preferred. Click here for our complete card review Earning rate: 1.5X on all business purchases ✦ 5X Lyft through September 2027 Base: 1.5X (2.25%) Card Info: Visa Signature Business issued by Chase. This card imposes foreign transaction fees. Noteworthy perks: Complimentary Instacart+ for 3 months (must activate by 12/31/27) ✦ $20 monthly Instacart credit See also: Chase Ultimate Rewards Complete Guide |

ⓘ $1029 1st Yr Value EstimateClick to learn about first year value estimates $750 cash back* ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer $750(*awarded as 75,000 points) after $6k spend in the first 3 months.No Annual Fee Recent better offer: $900 (*awarded as 90,000 points) after $6k spend in the first 3 months. (Expired 11/13/25) FM Mini Review: This one should be in everyone's wallet. Incredible welcome offer for a no-annual-fee card. Great card for 5X categories. Excellent companion card to Sapphire Reserve, Sapphire Preferred, or Ink Business Preferred. Click here for our complete card review Earning rate: 5X office supplies and cellular/landline/cable (on up to $25,000 in total purchases in 5x categories annually) ✦ 2X on the first $25K in combined purchases at gas stations and restaurants each cardmember year ✦ 5x Lyft through September 2027 Card Info: Visa Signature Business issued by Chase. This card imposes foreign transaction fees. Noteworthy perks: Complimentary Instacart+ for 3 months (must activate by 12/31/27) ✦ $20 monthly Instacart credit See also: Chase Ultimate Rewards Complete Guide |

And here are a few business card offers which, at the time of this writing, offer $500 cash back for approximately $5,000 of spend:

| Card Offer and Details |

|---|

ⓘ $890 1st Yr Value EstimateClick to learn about first year value estimates $1,000 Cash Back ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer $1K bonus cashback after $10K spend in the first 3 months from account opening$0 introductory annual fee for the first year, then $95 Recent better offer: $1,500 after $15,000 spend in the first 3 months from account opening (Expired 8/11/25) FM Mini Review: A good option for business owners who prefer simple cash back rewards. Earning rate: 5% on hotels and rental cars booked via Capital One Business Travel ✦ 2% everywhere Base: 2% Portal Hotels: 5% Card Info: Mastercard issued by CapOne. This card has no foreign currency conversion fees. |

Best consumer cash back offers

As I write this, the best consumer cash back offer is for the Chase Sapphire Preferred Card. The current offer is for 60,000 points (worth at least $600).

| Card Offer and Details |

|---|

ⓘ $985 1st Yr Value Estimate$50 prepaid hotel credit valued at $35 Click to learn about first year value estimates 75K Points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Earn 75,000 bonus points after spending $5,000 within the first three months from account opening.$95 Annual Fee Recent better offer: Expired 5/14/25: 100K after $5K spend FM Mini Review: Great welcome offer. Unlocks ability to transfer points to hotel & airline partners. Solid option to pair with no annual fee Ultimate Rewards cards such as the Freedom cards, Ink Business Cash, and Ink Business Unlimited. Earning rate: 5X Travel booked through Chase Travel℠ (2X all other travel) ✦ 5X Lyft through 9/30/27 ✦ 3X Dining ✦ 3X Select streaming services ✦ 3X Online grocery ✦ 10% annual point bonus Base: 1X (1.5%) Travel: 2X (3%) Flights: 2X (3%) Portal Flights: 5X (7.5%) Hotels: 2X (3%) Portal Hotels: 5X (7.5%) Dine: 3X (4.5%) Card Info: Visa Signature issued by Chase. This card has no foreign currency conversion fees. Noteworthy perks: Primary auto rental collision damage waiver ✦ Free DoorDash DashPass (min. one year, must activate by 12/31/27) ✦ $10 off each month on one non-restaurant orders from DoorDash ✦ Transfer points to airline & hotel partners ✦ Up to $50 back for hotel stays booked through Chase per cardmember year in the form of a statement credit ✦ Each account anniversary earn bonus points equal to 10% of total purchases made the previous year. |

Another terrific offer is for the Bank of America Premium Rewards Card. The current offer is for 50,000 points (worth $500) after $3,000 spend in 90 days. This also happens to be one of my favorite “everywhere else” cards (see: What’s in Greg’s wallet?)

| Card Offer and Details |

|---|

ⓘ $531 1st Yr Value Estimate$100 airline incidental fee credit valued at $90 Click to learn about first year value estimates 60K points 60K points (worth up to $600) after $4K spend in the first 90 days$95 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. FM Mini Review: This card has best-in-class earnings for those with $100K+ invested with BOA. With that level of investment, you would earn 3.5X travel & dining and 2.62X everywhere else. Earning rate: ✦ 2X travel and dining ✦ 1.5X everywhere else Base: 1.5% Travel: 2% Flights: 2% Hotels: 2% Dine: 2% Card Info: Visa Signature issued by BOA. This card has no foreign currency conversion fees. Noteworthy perks: $100 annual airline incidentals fee reimbursement ✦ $100 Airport Security Statement Credit towards TSA Pre✓ ® or Global Entry Application fee, every four years ✦ Up to 75% bonus for Preferred Rewards banking customers |

Sign up for two cards

Business card applications

For the rest of this post, for demonstration purposes, I will assume that the reader selected the 80K Chase Ink Business Plus offer, and the $750 US Bank Leverage card offer.

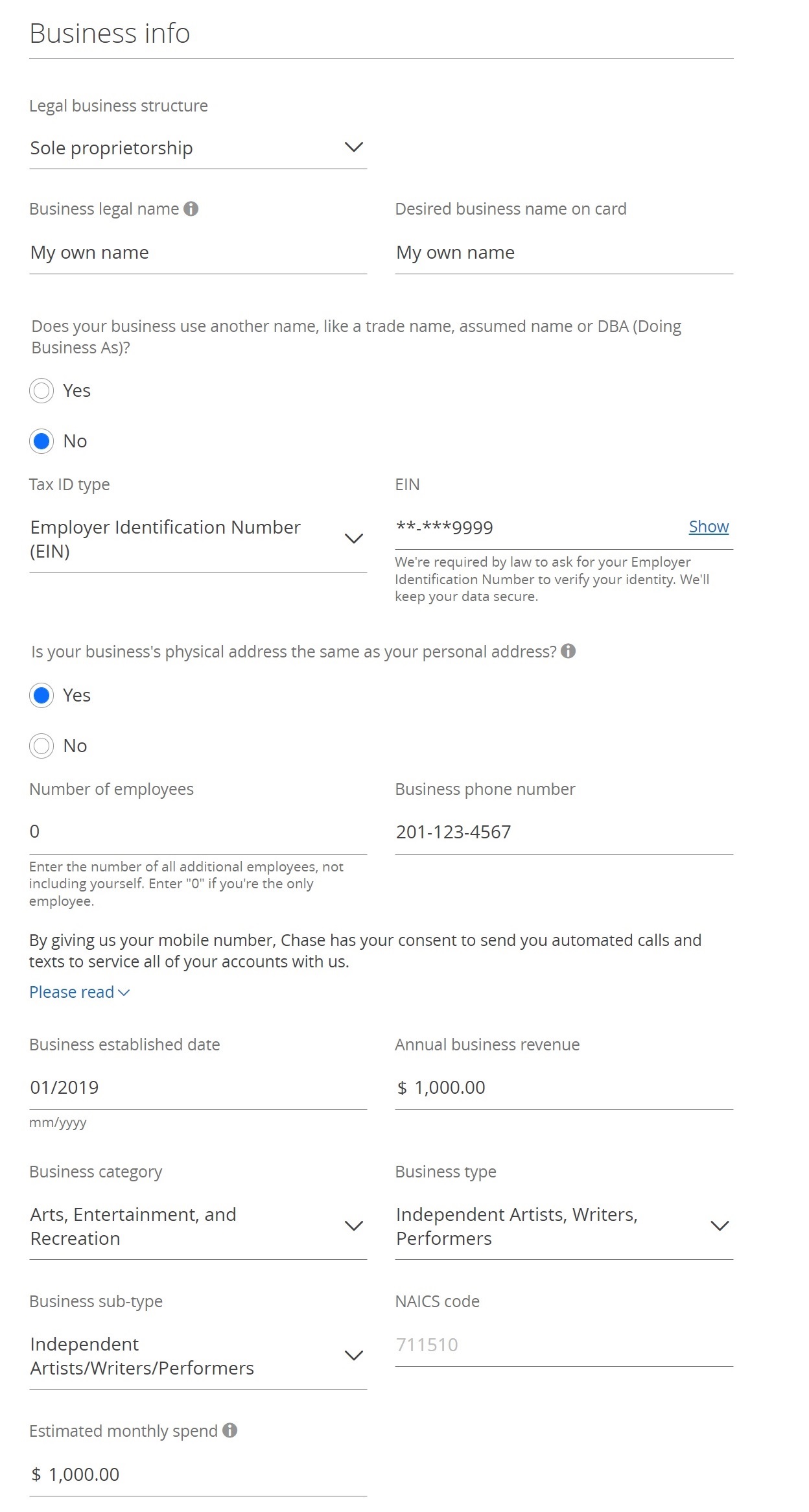

Below are details about applying for a Chase Ink card. Applying for business cards from other banks should be similar.

- Legal business structure: Sole Proprietor

- Business legal name: If you don’t already have a business name, I recommend using your own name as the business name.

- Desired business name on card: Again, this can be your own name if you don’t have a business name to use.

- Does your business use another name? No

- Tax ID type: EIN (you can get an EIN quickly and for free from the IRS here) If you'd prefer to use your social security number as your tax ID, select SSN rather than EIN.

- Is your business's physical address the same as your personal address? Yes

- Number of employees: 0 (the instructions say to enter the number of employees you have, not including yourself)

- Business phone number: Your phone number

- Business established date: When did your business start? If you've been doing your business for years (selling stuff at yard sales, for example), it's fine to estimate the starting date.

- Annual business revenue: $0 (or project an amount based on expected revenue)

- Business category, Business type, Business sub-type: Pick whichever categories are closest to your business. For example, an aspiring author, artist, or musician might choose: "Arts, Entertainment, and Recreation" and "Independent Artists, Writers, Performers."

- Estimated monthly spend: $3,000 (Use your judgement here. A higher number might lead to a larger credit line, but if it's too high it might negatively affect approval).

If your Chase Ink application is denied, I recommend calling for reconsideration (1-888-270-2127). It’s surprising how often denials can be changed to approvals just by asking.

Consumer card applications

Click through below to find more information and signup links for each card:

| Card Offer |

|---|

ⓘ $531 1st Yr Value Estimate$100 airline incidental fee credit valued at $90 Click to learn about first year value estimates 60K points 60K points (worth up to $600) after $4K spend in the first 90 days$95 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. FM Mini Review: This card has best-in-class earnings for those with $100K+ invested with BOA. With that level of investment, you would earn 3.5X travel & dining and 2.62X everywhere else. |

ⓘ $985 1st Yr Value Estimate$50 prepaid hotel credit valued at $35 Click to learn about first year value estimates 75K Points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Earn 75,000 bonus points after spending $5,000 within the first three months from account opening.$95 Annual Fee Recent better offer: Expired 5/14/25: 100K after $5K spend FM Mini Review: Great welcome offer. Unlocks ability to transfer points to hotel & airline partners. Solid option to pair with no annual fee Ultimate Rewards cards such as the Freedom cards, Ink Business Cash, and Ink Business Unlimited. |

Track card applications

When signing up for new cards, it’s very important to keep track of the basic details: which card did you sign up for and on what date? This information will come in handy in the future when you consider signing up for new cards. In many cases, you can sign up for the same cards again, but there are often restrictions. For example, with the Sapphire Preferred card, you can sign up again but only if you no longer have the card and 48 months have elapsed since you last received a welcome bonus.

To simplify this kind of thing, I highly recommend signing up for the free tool: Travel Freely. Travel Freely helps with the whole process. It will remind you when time is running out to meet spend requirements. It will notify you when a card’s annual fee is about to come due (in case you want to cancel or downgrade to no-fee card). And its Card Genie feature will let you know which offers you qualify for based on previous card applications. Note that Frequent Miler has a financial relationship with Travel Freely.

Meet spend requirements

Meeting spend requirements can be a challenge at any time, but these days when many are stuck at home it can be much harder. Fortunately, there are a number of relatively easy tricks to help get it done. Please see this post for details: 7 ways to increase credit card spend from home.

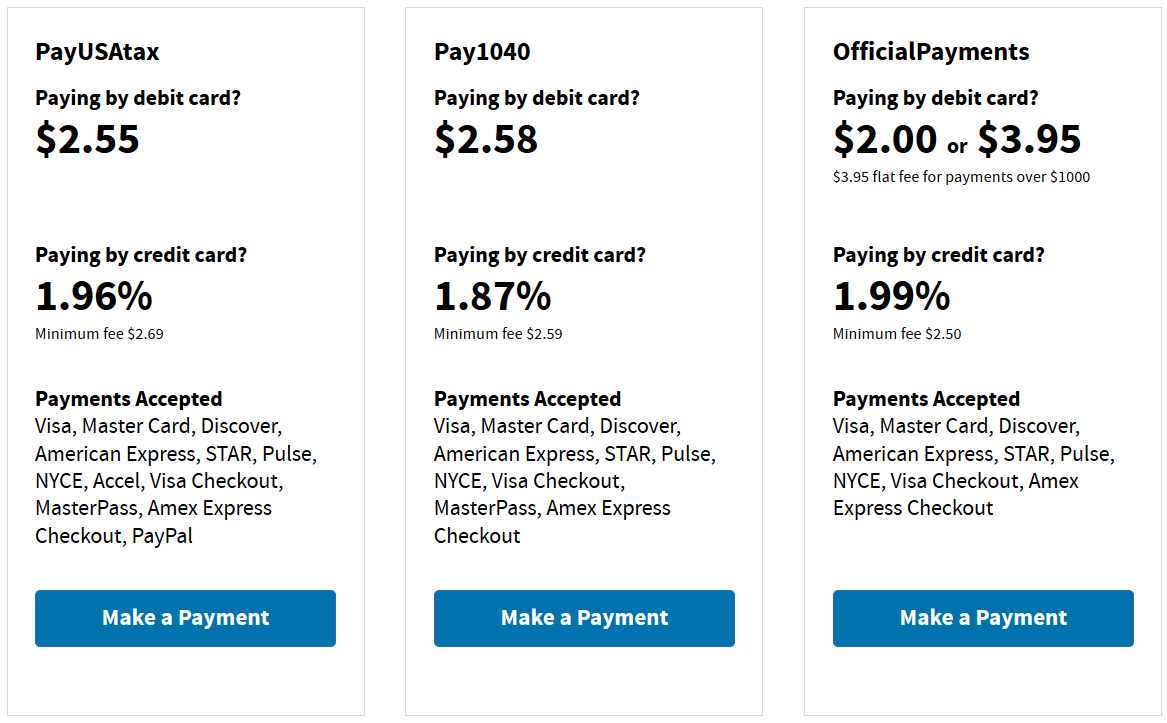

For this post, I’ll highlight one timely trick: Pay Federal Taxes.

There are several payment services that work with the IRS to let you pay your taxes by credit card. At the time of this writing, the cheapest option is Pay1040 which charges only 1.87% in fees. The other two options are barely more expensive at 1.96% and 1.99%. For each type of tax payment, you can make 2 payments per processor, so you can make 6 separate payments towards your year-end taxes (more can be done towards quarterly estimated taxes).

Here’s why this option is particularly timely:

- The IRS doesn’t mind people overpaying taxes and will refund the extra to you after you file annual taxes.

- If you pay (or overpay) taxes immediately before filing, you may be able to get your refund before your credit card bill is due.

- End of year taxes are usually due by April 15, but this year the deadline has been extended until July 15. As a result, there’s plenty of time to sign up for cards before filing your taxes.

Keep in mind that both the payment and the fee count towards your credit card’s minimum spend requirements. If you want to meet minimum spend all in one shot without going much over, here’s how much to pay in taxes (this is based on paying 1.87% in fees):

- $3,000 spend requirement: Pay $2,945 in taxes + ~$55 in fees.

- $4,000 spend requirement: Pay $3,927 in taxes + ~$73 in fees14725*

- $5,000 spend requirement: Pay $4,909 in taxes + ~$92 in fees

- $7,500 spend requirement: Pay $7,363 in taxes + ~$138 in fees

- $15,000 spend requirement: Pay $14,725 in taxes + ~$275 in fees

Full details about paying taxes with your credit card can be found here: Complete guide to paying taxes via credit card, debit card, or gift card.

Cash out rewards (or not)

Once you meet your minimum spend requirements, your promised welcome bonus should be applied to your account soon after the current credit card statement closes. At that point, you can withdraw those rewards as cash or a statement credit towards your account.

If you think you may travel within the next year, though, you might not want to withdraw your Chase points yet. With the Chase Sapphire Preferred or Ink Business Preferred card, points are worth 25% more when used to book travel through Chase. Or, if someone in your household has the Chase Sapphire Reserve card, points can be moved to that account and are then worth 50% more towards travel. With either Preferred card (or the Reserve card) you can also transfer points to a number of airline and hotel partners. In that way it is sometimes possible to get far more value for your points when you find particularly valuable awards.

Add it all up

The following calculations assume that all minimum spend requirements were achieved through paying (or overpaying) taxes at 1.87%. Additionally, I’ve made assumptions about which cards you signed up for…

Business Card Total: $1,350

Assuming you signed up for the Ink Business Preferred 80K after $5K spend offer and the US Bank Leverage $750 after $7,500 spend offer, then you’ll have incurred the following costs:

- Annual fees: $95 (the Ink Business Preferred card has a first year annual fee, but the US Bank card does not)

- Tax payment fees: $92 (Ink card) + $138 (US Bank card) = $230

- Total fees: $325

You’ll also have received the following rewards:

- Ink Business Preferred welcome bonus: 80,000 points = $800

- Ink Business Preferred rewards earned on $5,000 spend = 5,000 points = $50

- US Bank Leverage card welcome bonus: $750

- US Bank Leverage card rewards earned on $7,500 spend: $75

- Total rewards: $1,675

Net gain: $1,675 – $325 = $1,350

Consumer card total: $887

Assuming you signed up for the Sapphire Preferred 60K after $4K spend offer and the Bank of America Premium Rewards $50K after $3K spend offer, then you’ll have incurred the following costs:

- Annual fees: $95 x 2 = $180

- Tax payment fees: $73 + $55 = $128

- Total fees: $308

You’ll also have received the following rewards:

- Chase Sapphire Preferred welcome bonus: 60,000 points = $600

- Chase Sapphire Preferred rewards earned on $5K spend = 5,000 points = $50

- Bank of America Premium Rewards welcome bonus: 50,000 points = $500

- Bank of America Premium Rewards rewards earned on $3K spend = 4,500 points = $45

- Total rewards: $1,195

Net gain: $1,195 – $308 = $887

Q & A

How does this affect my credit score?

In most cases, signing up for credit cards causes credit scores to temporarily dip a small amount, but that effect usually only lasts for a few months. In the long term, scores tend to increase. This happens because a large part of your credit score is your utilization ratio. The more credit that is available to you, the better your utilization looks on your credit report.

Can I charge non-business expenses?

Anecdotally, almost everyone I know uses business cards for personal expenses. That said, the terms in most business card applications state that you should use the card only for business use. Also, some consumer credit card protections do not apply to business cards. My advice: use the card for personal expenses only if you’re comfortable doing so. Tax payments can be a combination of personal taxes and business taxes and so should be considered legitimate business spend.

Can my significant-other and I both do this?

Yes! A couple can easily double rewards by signing up for the same cards. In fact, it’s often possible to do even better by referring each other. For example, the Ink Business Preferred currently has a 20,000 point ($200) refer-a-friend offer. So it may be possible, for example, for you to sign up for the card for the welcome bonus and then for you to get 20,000 more points by referring your significant other.

I have a Chase Ink card already, can I get another?

Yes. Unlike Chase Sapphire consumer cards, Chase Ink Business cards do not have rules barring you from getting the bonus if you’ve had this or another Ink card in the past 48 months. Further, it’s possible to get the same Chase Ink card and welcome bonus for each business you own (if you have more than one business). Similarly, it’s possible to get all three Ink Business cards (and the welcome bonuses) for each business you own.

Isn’t this too good to be true?

It does seem that way! But it really works. The reason that banks offer huge welcome bonuses like the ones described here is because they believe that it’s worth it to get your business. They are counting on eventually getting back their money plus much more through fees and interest payments. The way to avoid that is to be smart and organized. Be careful to pay your credit card bills on time and in full, every month. And when the second year annual fee comes due, cancel or product change to a fee-free card.

COVID Credit Card Enhancements Ultimate Guide: Now with Amex dining & wireless credits…")

How many credit card links are in this post? My goodness!! It really comes off as a money grab on your site’s part.

I’m sorry if it comes across that way. The post is about getting cash from signup offers so of course we would list those offers. Most of the cards in this post do not give us affiliate commission. Also, FYI, there actually aren’t any direct application links in this post. The links go to pages with more information about each card (and application links are found there).

TheUSB biz leverage card is fairly difficult to get approved for. Most that apply get denied. I personally got denied for not having a Dun & Bradstreet credit file. I’ve fixed that, will try to recon again in a week.

What if you have already filed but not paid. Then over pay. Will they send you a check/direct deposit it into your account?

Don’t have high taxes this year but looking to get a business card sign up. Holding off on personal as almost under 5/24 and avoiding not transferable currencies till the current climate changes.

Yes, in my experience, they’ll refund the over payment eventually

A chase rep once FREAKED OUT and lectured me when I asked if the bank cared about using business card for personal expenses.

Of course, I applied my standard response: “Are you trying to insult me or are you just that stupid”

PSA – BofA seems to be stricter with Biz approvals – applied first week of February (2 year biz bank acct with 5K parked, BofA, 2 year Biz AS card – all under SP EIN legit biz with 3 other business CC lines from other issuers under same EIN and my SSN for PG – not a “Business” application and 800+ FICOs) FACTA reasons were a joke .

Hitting a wall even though were under 5/24 for new cards to apply DOC did post about the USB Infinite Visa both personal and business which has attractive travel bonus with points.

Good to know.

Regarding USB: Yep, we need to add those cards to our database!

[…] Last week I published an easy way to earn $1,100 by signing up for two credit cards. I even included an easy way to meet minimum spend requirements from home. See: Build your own $1,100 bank-funded stimulus check. […]

For taxes, you still hafe to file by April 15, but the payment deadline has been extended 90 days

That was what was originally reported, but the IRS changed it to allow filing up until July 15. Details here: https://www.irs.gov/newsroom/tax-day-now-july-15-treasury-irs-extend-filing-deadline-and-federal-tax-payments-regardless-of-amount-owed

This is way too much work!

If you have IRA’s or traditional brokerage accounts, just open new accounts at JP Morgan and Chase, transfer whatever amount you want, and sit back for 3 months (Chase) or 6 months (JPM) and collect the $600 bonuses. You don’t have to trade anything, just park the money there. Then after you receive the bonuses, you can either use their trading services, just let the cash and securities sit there, or transfer it back to your original brokerage. Simple, no credit score hit, no minimum spend, no recordkeeping except for a few key dates (read the fine print of course so you know what those dates are). Google Chase Brokerage Bonus and JP Morgan Yes Account for current offers.

I know this is slightly off-topic for Frequent Miler, but i make the contribution with confidence that your readers are savvy to all sorts of bonus programs and may not have thought about this angle.

Why not do both? One does not preclude the other.

$600 brokerage bonus requires $250,000 in funds. Applying for credit cards requires none if you’re savvy.

If I want to repeat this or any other card offer in two years, when do I cancel the original card and how does that impact my credit score.

Each bank has different rules about how long you need to wait before becoming eligible for the same card again. See our Best Offers page where we have application tips at the beginning of each bank section: https://frequentmiler.com/best-credit-card-sign-up-offers/

Impact on credit score when you cancel a card:

Most business cards aren’t reported to the consumer credit bureaus and so opening those cards does not help your score and closing those cards does not hurt your score. One significant exception is with Capital One business cards which ARE reported to credit bureaus just like consumer cards.

When cancelling a consumer card (or a Capital One business card), your utilization ratio may be negatively impacted. There are two ways to avoid this:

1. If you have other cards with the same bank, call to see if they’ll move your available credit from the card you plan to cancel to one that you want to keep. Or…

2. Rather than cancelling, product change to a fee-free card and keep that card long term.

What about its impact on credit utilization or in reducing the total amount of your authorized credit when you drop a $10-$20k limited card?

Oops. You’re right. I’ve updated my answer to you above. Thanks for pointing that out.

Will product changing then allow you to reapply for the original card 24 months after obtaining the original card?

Quick answer: Yes.

Longer answer, part 1:

Usually product changing has the same effect as cancelling. e.g. afterwards, you no longer have the card. One exception I can think of is with Citi cards where they have rules about signing up for cards within 24 months of either cancelling or receiving a signup bonus. In that case, product changing can be better than cancelling (except that sometimes Citi issues a new credit card number when you product change and then will treat it as a cancellation even though it doesn’t show up that way on your credit report)

Longer answer part 2:

Each bank has different rules. Waiting 24 months isn’t always necessary nor is it always enough. For example, Amex has their lifetime rule: if you’ve had the same card before then technically you’re not qualified for a new signup bonus no matter how long ago you had that card. That said, Amex is known to “forget” you had a card about 7 years after you’ve cancelled or product changed it.