NOTICE: This post references card features that have changed, expired, or are not currently available

Update: While accurate at the time of publication, some of the offers mentioned in this post have since expired. See our Best Offers page for up-to-date offer information.

Now that the SPG Luxury Card is available, there are five credit cards that offer welcome bonuses between 75K and 100K points. Here is a list sorted descending by estimated first year value (click through any link to get to our dedicated page to learn more about that particular card):

| Card Offer |

|---|

ⓘ $1275 1st Yr Value Estimate5 Marriott 50K Free Nights valued at $1540 Click to learn about first year value estimates Up to 5 x 50K Free Night Certificates ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Earn 3 Free Night Awards after you spend $6k in purchases and an extra 2 Free Night Awards after you spend an additional $3k in purchases on the Card within the first 6 months of Card Membership. Each award has a redemption level up to 50K Marriott Bonvoy® points. Terms apply. (Rates & Fees)$125 Annual Fee Recent better offer: 5x50K free night certificates after $8K in spend (expired 10/16/24) |

ⓘ $1075 1st Yr Value Estimate3 Marriott 50K Free Nights valued at $924, Marriott 50K Free Night valued at $308 Click to learn about first year value estimates Up to Four 50K Free Night Certificates + $100 airfare credit ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Earn 3 Free Night Awards after spending $3k on eligible purchases within 3 months of account opening, and earn 1 additional Free Night Award after spending $4k total on eligible purchases within 4 months of account opening. Plus, get up to $100 in statement credits after spending $500 on eligible airline purchases. $95 Annual Fee Recent better offer: None |

ⓘ $1066 1st Yr Value Estimate$300 dining credit ($25 per month) valued at $270 Click to learn about first year value estimates 200K Points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Limited Time Offer: Earn 200K points after $6k in eligible purchases within your first 6 months of card membership. Terms apply. Rates & Fees (Offer Expires 5/13/2026)$650 Annual Fee Recent better offer: None. FM Mini Review: Decent ultra-premium option for Marriott fans, especially those aiming for lifetime status tiers |

ⓘ $1020 1st Yr Value EstimateClick to learn about first year value estimates 175K Points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer Limited Time Offer: Earn 175K points after $5k in eligible purchases within your first 6 months of card membership. Terms apply. Rates & Fees (Offer Expires 5/13/2026)$250 Annual Fee Recent better offer: None. |

ⓘ $342 1st Yr Value EstimateClick to learn about first year value estimates 85K points ⓘFriend-ReferralThis is a friend-referral offer. A member of the Frequent Miler community may earn a referral bonus if you are approved for this offer 85K points after $4K total spend in first 3 months$250 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. |

ⓘ $208 1st Yr Value EstimateClick to learn about first year value estimates 30k Points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer 30K points after spending $1k on eligible purchases within the first 3 monthsNo Annual Fee This card is subject to Chase's 5/24 rule. Click here for details. Recent better offer: 60K points + Free Night Certificate after $2K spend (Expired 7/17/25) FM Mini Review: The best use for this card is probably to downgrade from the Ritz or Boundless card to avoid the annual fee. That way, you can always upgrade again when you need the annual free night or other perks |

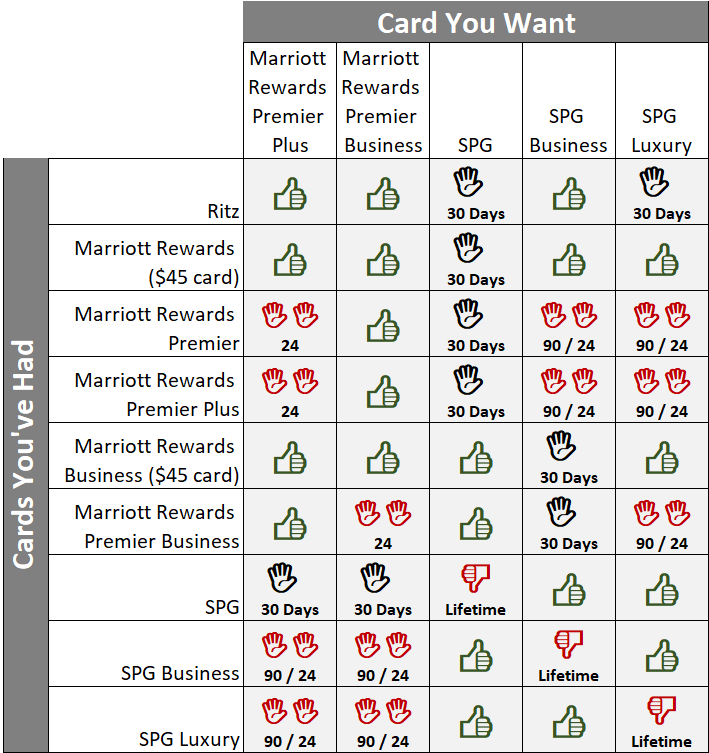

Amex / Chase Cooperation

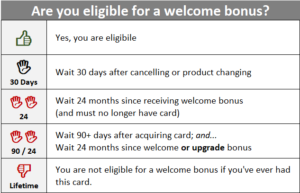

Beginning August 26th, something unprecedented will happen. Amex and Chase will limit welcome bonuses based on your experience with holding cards and/or receiving bonuses with the other bank.

The rules that begin 8/26 are complicated, so check out this post for full details: Navigating Marriott’s Byzantine Credit Card Rules. The basic idea is that you may not be eligible for a Chase Marriott welcome bonus if you have certain SPG cards or have received bonuses on those cards in the past 24 months. And, similarly, you may not be eligible for an Amex SPG welcome bonus if you have certain Chase Marriott cards or have received bonuses on those cards in the past 24 months.

The Window of Opportunity

The above rules do not kick in until Sunday 8/26. You can qualify for welcome bonuses if you apply before that date even if you have Chase cards or have earned Chase welcome bonuses that would later make you ineligible for Amex bonuses, or vice versa.

Note that you do not have to be approved before the 26th, you just have to submit your application before then. Be careful not to submit an application late on the 25th, though, as those applications may be recorded as having come in the next day.

Don’t forget Chase 5/24

Signing up for Chase or Amex consumer cards (not business cards) will add to your 5/24 count. Depending upon your current situation, that may or may not be a problem. In my case, I’m so far over 5/24 that I don’t really care. If I was under 5/24 or working towards getting under 5/24, though, I would probably stay away from the SPG and Marriott consumer card applications for now.

| Chase's 5/24 Rule: With most Chase credit cards, Chase will not approve your application if you have opened 5 or more cards with any bank in the past 24 months. To determine your 5/24 status, see: 3 Easy Ways to Count Your 5/24 Status. The easiest option is to track all of your cards for free with Travel Freely. |

Who should get what?

Here are my recommendations for each of the currently available offers:

- SPG Business:

With 100K points on the table and no first year annual fee(note: this offer has since expired), this is the single best offer available right now. If you have a business and have never had an SPG Business card before (or it has been 7+ years since you cancelled the card), then this is a great choice. Keep in mind that getting this card will limit your ability to get Chase Marriott welcome bonuses in the future (unless you sign up for those cards too before 8/26). See our SPG Business Credit Card Page for more information about this card. - SPG Consumer: Is there anyone out there who hasn’t had this card in the past 7 years? If so, it’s worth considering. My primary hesitation would be if you are under 5/24 (or trying to get under 5/24). In that case, this card will add to your count and make you less eligible for Chase cards in the future due to 5/24. Interestingly, unlike the SPG Business card, this card does not specifically stop you from getting a bonus on Chase Marriott cards in the future. You would just have to cancel this card 30 days prior to applying. See our SPG Credit Card Page for more information about this card.

- SPG Lux: Since this card is brand new, and the new Amex/Chase/Marriott rules haven’t yet taken effect, virtually everyone is eligible for this card. That’s the good news. The bad news is that the $450 annual fee is not waived the first year. You will get $300 back if you spend $300 at Marriott/SPG properties (including room rates) though, so it’s not as bad as it seems. Like the SPG Business card, this card will limit your ability to get Chase Marriott welcome bonuses in the future (unless you sign up for those cards too before 8/26). And like the SPG consumer card, this will add to your 5/24 count. See our SPG Luxury Card Page for more information about this card.

- Marriott Business: Even though the welcome bonus isn’t as high as it’s been in the past, it’s a great choice for many: This is one of the few Chase cards that is not subject to 5/24 rules. Plus, since it is a business card, it won’t add to your 5/24 count. Beginning 8/26 getting this card will limit your ability to get the welcome bonus on the SPG Luxury card. See our Marriott Rewards Premier Business Card Page for more information about this card.

- Marriott Premier Plus: This one is subject to 5/24 and it will add to your 5/24 count if you get the card. Plus, it will limit your ability to get welcome bonuses on the SPG Business and SPG Luxury Cards in the future. Overall, I don’t recommend this one. If you’re under 5/24, then there are more valuable Chase offers that you should consider first (see our Chase application tips and best offers here). For more information about the Marriott Premier Plus card, click here for our dedicated card page.

What will I do?

I’ll probably go for the SPG Luxury card because I do want to build my point totals up in order to book top tier 60K properties before they jump up to 85K or 100K in 2019. I personally value the $300 in Marriott/SPG credits at close to face value since we have definite plans to stay at Marriott/SPG properties and will no doubt spend much more than $300 in the next year even with award stays (stupid resort fees alone might do it). So, my net first year cost for the SPG Luxury card is $450 – $300 = $150. Is it worth paying $150 (or even $200 if I value the credits much less) for 100,000 Marriott points? Absolutely.

I’m also waiting to see what happens with my recently (and somewhat accidentally) acquired SPG and SPG Biz cards. I’ve finished the minimum spend on each, but haven’t received new SPG membership yet for those cards (see this post for details about this craziness).

My wife may also get the Luxury card. She isn’t qualified to earn bonuses on any of the other cards (she has them all!), but she will qualify for the Luxury card bonus even after the new rules kick in on 8/26. It has been more than 24 months since she received bonuses on her Marriott cards (and she hasn’t yet upgraded her Marriott Premier to Premier Plus).

My son hasn’t successfully signed up for any new cards since his Discover It Student card. I’m thinking that it’s time for him to start a business and try for the SPG Business card. Maybe he’ll try the Marriott one too, but I think that approval from Chase is a long shot. Either way, I’ll help him meet the minimum spend requirements. If he does apply and get approved for the Marriott Business card, he might also consider the SPG Luxury card before 8/26 since he would otherwise be shut out from that bonus for 24 months after getting the Marriott Business card bonus. On the other hand, Chase rarely approves business cards that quickly, so maybe he should skip that one altogether. Now I’m leaning towards him signing up for both the SPG Business and SPG Luxury cards. Still pondering… Update: I think my son will do the SPG business card now and the SPG consumer card sometime later. Neither should exempt him from getting the Lux card in the future.

| Applying for Business Credit Cards Yes, you have a business: In order to sign up for a business credit card, you must have a business. That said, it's common for people to have businesses without realizing it. If you sell items at a yard sale, or on eBay, for example, then you have a business. Similar examples include: consulting, writing (e.g. blog authorship, planning your first novel, etc.), handyman services, owning rental property, renting on airbnb, driving for Uber or Lyft, etc. In any of these cases, your business is considered a Sole Proprietorship unless you form a corporation of some sort. When you apply for a business credit card as a sole proprietor, you can use your own name as your business name, use your own address and phone as the business' address and phone, and your social security number as the business' Tax ID / EIN. Alternatively, you can get a proper Tax ID / EIN from the IRS for free, in about a minute, through this website. Is it OK to use business cards for personal expenses? Anecdotally, almost everyone I know uses business cards for personal expenses. That said, the terms in most business card applications state that you should use the card only for business use. Also, some consumer credit card protections do not apply to business cards. My advice: don't use the card for personal expenses if you're not comfortable doing so. |

")

")

If my spouse is an authorized user of my SPG card but never got the sign up bonus herself, do you think she is eligible for the Marriott Premier plus bonus? She is under 5/24

Yes, being an AU doesn’t affect your eligibility for new card bonuses

Is there a benefit to NOT combining accounts? Someone offhandedly mentioned something about lifelong status, but I’m not sure what the specifics were about what this person was talking about

I’m not aware of any benefit.

Greg, thanks for this wonderful post. I applied SPG business (approved), Marriott Business (pending), SPG business for wife (approved) Marriott business premier plus for wife (pending) and Marriott premier plus for wife (pending). Wife is under 5/24 and I am right at 5/24. Will be using Plastiq to meet all min spend. This is a total of 425,000 points. 75k x 3 + 100k x 2 = 425k!!! Although I am not a big fan of Marriott devaluing our points year over year, this is still the best alternative to fill up on points. Thank you so much. I find all of your articles valuable.

I received upgrade offer for 100k good till October. Will this offer bypass the spg /Marriott restriction if I wait until October to upgrade ?

Yes. The upgrade offer doesn’t list these restrictions

So if I applied for the Ritz card on the last possible day (28 days ago) can I apply for the 100K amex? I am condused by the 30 day rule.

It doesn’t apply until the 26th so you should be good if you apply today. Once the 30 day rule takes into affect tomorrowyou will have to actually cancel your Ritz card and wait 30 days before you can apply for the Lux.

I don’t have neither the Marriott Business nor the SPG Luxury. I would have to apply for both tomorrow, but if I wait after 8/26, I can still get both cards if I apply on the same day

I’ve had the SPG business before. Do you think having it under another business name will qualify when i use my own SSN? Looking at your chart, probably not 🙁

No. That used to work with Amex but it doesn’t work anymore (at least not usually)

I got the Marriott premier plus in early June, so in the last 90 days. Can I still get the 100k from spg luxury if I sign up by tomorrow?

Yes

Four Amex cards currently. one the personal SPG I’ve had for over 5 years. one chase Marriott premier business less than 2 years old.

Applied for SPG business and warning came up before final submission stating I was not eligible for the offer.

I’m not at all sure the popup is working correctly

I received the personal Marriott 100k about 2 months ago. Is it possible to apply for both the Marriott business and the spg lux in the next 2 days and receive both bonuses?

Yes

Greg, I signed up for Chase Marriott card almost a year ago when offering 120k points on up to $12k spend. So, when considering waiting for 24 month after the bonus date, when should the clock start in my case? The date when I receive the latest point from that 120k? Thanks.

I don’t know. I wouldn’t trust a phone rep to know either. So, if you’re interested in getting one of the SPG cards, I’d recommend doing so today or tomorrow, otherwise you may have to wait a very long time.

Any one with a referral link for the Marriott Business?

I’d like to trade for an SPG business referral or for Chase Ink Preferred, Chase Southwest, Chase IHG, or one of many Amexes.

My friend has a Marriott Business but is unable to get any referral links at present.

How old is your son? (Thinking about possibilities for my kids)

He turned 18 in November. Here’s the post about it: https://frequentmiler.com/2017/12/01/teens-first-credit-card-2/

Although the card is launched today , how do u know the terms are applicable only for accounts open from 26th , not today . I think the card open date doesnt matter and at the time of points posting , if u r not in co ordnance with the rules , u may be denied for the bonus quoting the same.

They always apply the offer terms that are in place at the time they receive the application

Seat back and relax and wait for DPs.