NOTICE: This post references card features that have changed, expired, or are not currently available

I give up; I am part of the way to a welcome bonus that I won’t even try to finish earning. It’s just not worth it.

Amex has absolutely ruined my wallet in a way that is totally changing the game for me at the moment. I have so many bench players just dying to get in the game that the cards I thought were perfect for specific purposes have been relegated to the minor leagues of my sock drawer for the next several months.

I thought that my wife and I had finally put together the perfect wallet: we had 8x at gas stations, 4x grocery and dining, 2.625% cash back on unbonused spend, and co-branded cards with each of the major hotel chains that would be best for spend at their respective brands. Then Amex came in like a wrecking ball with the +4 referral promotion that we have written about and we talked about on the podcast this past weekend. Then, over the weekend, I stayed at a Marriott property and realized that I shouldn’t pay with a Marriott credit card. After checkout, I was standing at the gas pump ready to use the Wyndham Business Earner card for 8x when I realized that even at 8x it wasn’t the best card in my wallet for that purchase. Then, I got to doing the math and I realized that it won’t even be worth finishing the spending requirement for the welcome bonus on the World of Hyatt credit card that we opened a few months ago.

For the next 3 months, my wallet will be almost entirely Amex cards.

The awesome +4 referral promotion

For those unfamiliar, the short of the current Amex referral promotion is this: Most cards that earn Membership Rewards points are currently offering a referral bonus of +4 points per dollar on up to $25K in purchases for 3 months from the date your referral is approved. You must take advantage of this promotion by 12/1/21. See more detail in this post about how it works and on the podcast about why this deal is so awesome.

My displaced cards

The Bank of America Premium Rewards became the king of my wallet for unbonused spend about a year ago thanks to moving our IRAs to Bank of America to trigger Preferred Rewards Platinum Honors status. That status provides a 75% bonus on earnings on Bank of America’s in-house cards, so we earn 2.625% cash back on the Premium Rewards card, which makes the prospect of earning points instead of cash kind of an expensive value trade.

Still, at times I have used the Capital One Venture card to earn 2x miles per dollar to transfer to partners I love like Turkish Miles & Smiles or Wyndham Rewards despite the expensive trade-off.

However, using either of those cards now seems preposterous for the next 3 months.

That’s because my wife has triggered the +4 offer on her Blue Business Plus card. That means she’ll earn 6 points per dollar over the next few months because the Blue Business Plus card offers 2x on the first $50K in purchases per year (then 1x) and she’ll get 4 points per dollar on top of that on up to $25K in purchases from the referral promotion. At a base level, those 6 points per dollar could be cashed out for 6.6c with her Schwab Platinum card. In other words, her Blue Business Plus offers a return of 6.6% on all purchases while she has capacity for 2x and 4x. That’s nuts.

At that rate of return, it beats the best you’d ordinarily do with most credit cards in most situations.

For instance, I stayed at a Ritz-Carlton property over the weekend. I thought for a moment to myself about using one of our many Marriott credit cards for incidentals. However, the Marriott cards offer 6x Marriott points at Marriott properties. With the Blue Business Plus, we can earn 6x everywhere right now. Membership Rewards points can transfer 1:1 to Marriott or to an array of (more valuable) airline programs. Using the Blue Business Plus and earning 6 Membership Rewards points per dollar is far superior to using a Marriott credit card (and indeed that’s what we did since we needed to provide a credit card at check-in and the incidentals weren’t significant enough for me to want to dig through my bag for one of my Marriott gift cards).

The same situation is true with IHG, Radisson, and Choice Privileges: earning 6x Membership Rewards points easily beats what those cards offer even on-brand. That really isn’t as much a slam on those credit cards as much as it is a testament to the strength of the +4 offer. It would be tough to beat six Membership Rewards points per dollar spent in a normal world.

Yet 6x Membership Rewards points isn’t even the best option in my wallet right now for “everywhere else” spend and won’t be for a while.

My best “everywhere else” cards right now

I was standing at the gas pump the other day ready to pop in our Wyndham Earner Business card when it dawned on me that not even 8x Wyndham points was enough return to beat out my best current Amex card(s).

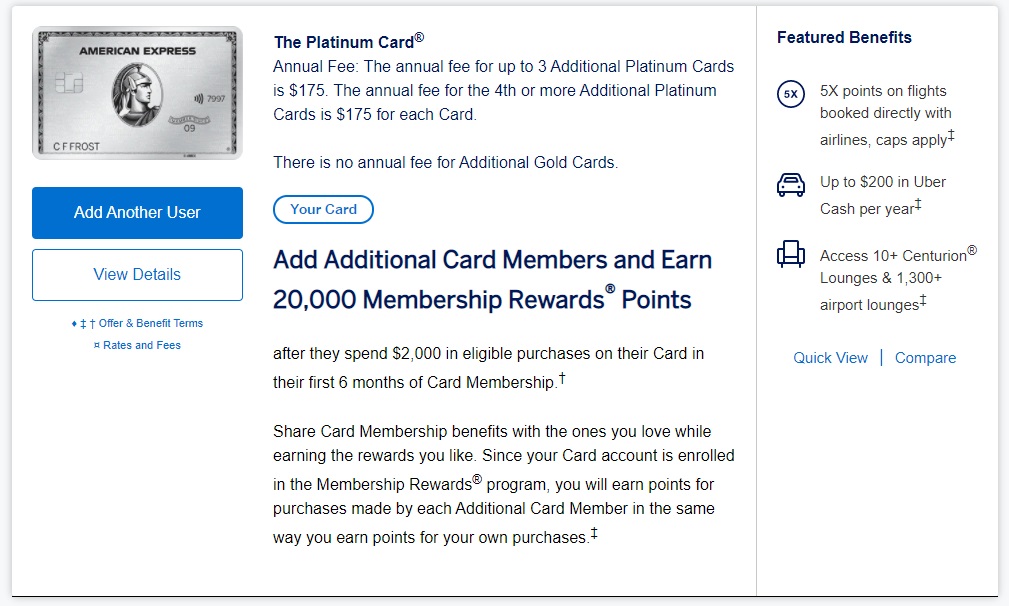

That’s because my wife added me as an additional Gold card user on her Platinum account recently. She had an offer to earn 20,000 points by adding an additional cardholder who spends $2,000 in the first 3 months.

Most Amex Platinum cards charge $175 for up to 3 additional Platinum cardholders who each get benefits like Centurion lounge access, Delta SkyClub when flying Delta, and access to stuff like Fine Hotels & Resorts. However, you don’t need to add an additional Platinum cardholder; you can add a Gold authorized user for free. Note that the Gold-colored additional cardholder card on a Platinum card is not to be confused with the Amex Gold card. An “additional Gold card” on a Platinum account does not have any of the Amex Gold card’s bonus categories or benefits. Instead, it has the same bonus categories as the Platinum card, it’s just Gold in color to make it clear that it doesn’t have any of those extra Platinum card benefits like lounge access.

My wife had added me as a Gold additional cardholder on her Platinum account, so if I spend exactly $2K on that card, the effective return will be 10x when she receives her bonus (and I haven’t yet completed that spend, so we’re in that “10x” period). Earning 10x flexible Membership Rewards points is better than 8x Wyndham points. But it gets better.

My wife also referred someone from her Platinum card to trigger the +4 referral bonus on her Platinum card. That means she is earning 4 extra points per dollar for the next 3 months on up to $25K in purchases. The bonus also applies to purchases made by an additional cardholder.

That means that all of my purchases on that additional gold card are currently earning an effective 14x until I reach the $2K bonus threshold (at which point I’ll stop using the card for now since I have so many players on the bench itching to get in the game).

When that runs out, I still won’t need to settle for just 6x Membership Rewards points for quite a while.

Welcome bonus spend is (almost) always well-bonused

Any time I point out a good “everywhere else” type of card, a few readers always chime in to make the (good) point that if you’re willing to open a new credit card, you never need to settle for just 2 or 3 percent back.

That’s because welcome bonuses almost always represent a return of something more like 8-10% back or more. Depending on individual spending needs, I bet that most people could open 3 or 4 new credit cards per year and if they space out the applications, they could probably always earn a return in at least that 8-10% range. With more than 150 cards on our Best Offers page, you could play long ball and maintain that rate of return for decades if the game stayed the same.

It just so happens that we’ve recently opened a number of new cards in my household that offer the opportunity to get great return. Since this is spend we’ll have to do in order to earn large welcome bonuses, we’ll obviously prioritize this spend. At least, we’ll prioritize most of it.

The most significant minimum spending requirement of those opportunities is the Capital One Venture X card. This card currently offers 100K Capital One miles after spending $10K in the first 6 months. Combined with the 20K miles earned from $10K in unbonused purchases, we’ll have at least 120K miles after meeting the minimum spend. That’s a total return of 12x. While not quite as good as the return I’m earning right now on my Gold authorized user card, that is still entirely respectable and will be a great deal when we get to it. At a base level, that 12x is like getting at least 12% back since the Capital One miles could be used to erase travel at a rate of $0.01 per point.

That said, we probably won’t get to spending serious money on the Venture X until late February. That’s because the +4 offer that we have triggered on a number of our cards is only available for 3 months from the date the person you refer is approved. Since we’ll have incredible opportunities on Amex cards for the next 3 months, I’ll probably leave the Capital One spend until the latter half of the 6-month spending window.

And I’ll probably bow out of finishing the spend for the World of Hyatt card welcome bonus altogether – even forgoing the Category 1-4 free night award that I could earn with enough spend. It just isn’t worth it right now. back to that in a minute.

Amex Business Green was my luckiest mistake lately

I wrote a section in a post last week about how I opened the Amex Business Green Rewards card recently solely for the purpose of triggering my wife’s +4 offer on her Gold card without picking up an annual fee this year (the Business Green has no fee the first year, then it’s $95).

Within a few days of approval, I was targeted for an offer to add up to 5 employee cards and get 20K bonus points after $4K spend on each within 3 months. That’s like a return of 5x bonus points on top of the 1x that the earn ordinarily earns for an effective 6x everywhere on exactly $4K spend on each employee card. Before the +4 referral promotion ends on 12/1, I intend to refer someone from my Business Green Rewards.

That will add an additional 4 points per dollar on all spend on my Business Green Rewards card for the next few months, including for the additional cardholders. In other words, those cards will be earning an effective 10x on all spend if they each get exactly $4K in spend. Actually, since I haven’t even started spending toward the welcome bonus yet (which is 25K points after $3K in purchases in the first 3 months), the first $3K in spend will juice things up a bit further yet. Once we complete $4K spend on the first of those additional cardholders, we’ll earn:

- The 25K welcome bonus

- 20K bonus points from the additional cardholder bonus

- 4K points at the standard 1x

- 16K points from the +4 promotion

That’s a total of 65K Membership Rewards points after $4K on one of those additional cards. That’s good for a return of 16.25x. On the Business Green Rewards card.

Each additional card thereafter on which we meet the $4K spending requirement will earn a total of 40K points (20K bonus points from the additional cardholder bonus, 16K points from the +4 promotion, and 4K base points at 1x on $4K in purchases), an effective return of 10x provided that we meet the $4K spending requirement exactly (falling short would mean missing the 20K bonus and spending beyond $4K would mean reducing the rate of return per dollar spent).

All this adds up to the Hyatt card not making sense

I also noted in my post last week that my wife opened the World of Hyatt credit card a few months ago. The current welcome bonus on the card is awful, but she was about to go over 5/24 and wanted to grab it while she could.

I say that the current welcome bonus is awful because it offers 30K points after $3K in purchases plus 2x everywhere for the first $15K in purchases. After meeting $15K spend, we’d have 60K World of Hyatt points. The card also offers a Category 1-4 free night certificate with $15K in purchases in a calendar year. While the welcome bonus isn’t great, surely it made sense to spend toward the free night certificate anyway, so we’d make out OK.

Except now we won’t meet the spend.

Unfortunately, we didn’t prioritize meeting the spending requirement early on this card and we are now facing about $10K spend left to do. There was some laziness here: I had figured that we’d make a tax payment or two through Plastiq (I have a lot of fee-free dollars) with this card to knock out the spend without much effort. But now, I am questioning whether it’s worthwhile at all. My instinct is that it isn’t thanks to all of this incredible bonused spend from Amex.

The $10K in purchases we have yet to do on the World of Hyatt card would yield us 20,000 World of Hyatt points (because we are in the welcome bonus period) and a Category 1-4 free night certificate. If we put that $10K in purchases on my wife’s Blue Business Plus card, we have a minimum return of 6.6% (the rate at which we could redeem the points for cash via Schwab). That means the opportunity cost of spending on the Hyatt card is at least $660.

Is 20K points and a Category 1-4 free night certificate worth more than $660?

Before you start thinking of your best Category 1-4 free night certificate redemptions, let me stop and remind that the maximum value of the certificate is 15K points (the cost of a Category 4 night). Even that would be an overly generous valuation since points don’t expire but the certificate does. But let’s be generous and say that it is worth 15K points: is it worth giving up $660 on the Blue Business Plus for 35K World of Hyatt points (the 20K from spend + 15K from the certificate)?

I obviously know that 35K Hyatt points can be redeemed for a room (or rooms) costing more than $660, but would I actually pay $660 for 35K points? That’s a cost of almost 2 cents per point.

And that’s comparing against the Blue Business Plus, which I’ve already noted is a bench player in the current environment.

Between the Amex Platinum I opened through the Resy offer (which I plan to use to buy a car at 19x on $25K spend) and the other offers mentioned in this post so far, I have the following capacity to earn better than 6x Membership Rewards points everywhere:

- Almost $2K at 14x (Additional Gold card on my wife’s Platinum card)

- $4K at 16.25x (Business Green with welcome bonus, employee card bonus, and referral bonus stacked)

- $16K at 10x (Business Green other employee cards with the employee card bonus and referral bonus stacked)

- $20K at 10x (My wife’s Business Platinum card also has the offer to add up to 5 employee cards and earn 20K after $4K in purchases on each which stacks with the +4 referral offer)

- $10K at 12x with the Capital One Venture X (welcome bonus spend)

- $25K at 8x at US Supermarkets on the Gold card (which ordinarily earns 4 points per dollar on up to $25K at US Supermarkets per year, then 1x, but added with the referral promotion is yielding 8x for us right now)

When you add 19x at restaurants and small businesses on my Platinum card on up to $25K in purchases over the next 3 months (see more detail in this post), I’m looking at more than $75K worth of spending capacity at 10x Membership Rewards points (or a minimum of 11% cash back via Schwab) over the next few months and another $25K at 8x at US Supermarkets.

I almost surely won’t do all of that spend. I’m not sure which I’ll complete, but I know which one I won’t: it feels impossible to justify $10K spend on the World of Hyatt card for a best-case value of 35K Hyatt points. At a minimum of 11% back on most the cards above, my opportunity cost for spending on the Hyatt card right now is really $1100 for $10K spend. There’s just no way I’d pay eleven hundred bucks for 35K World of Hyatt points.

And so it just isn’t worth it. For the first time ever, I am going to miss the spending requirement for a welcome bonus and it isn’t going to be an accident. It’s just not worth spending for it in my current world.

Bottom line

The incredible Amex +4 promotion has made it hard for me to justify spend on other cards in my wallet, including the spend required to earn the full welcome bonus on the World of Hyatt credit card. Even with the chance to earn a free night certificate, it just doesn’t make sense to use the Hyatt card in situations where I can use an Amex right now — and even in situations where I can’t use an Amex I’ve got far better return available on the Venture X card. I just can’t see displacing any spend at the moment for a return worth less than 8x Membership Rewards points for the next several months. Maybe we’ll spend our way to a Hyatt free night certificate next year, but if Amex keeps showering us with points, it might continue to be hard to justify.

It’s okay to not meet the spend. I would have done Simon since that doesn’t work with Amex but it does require time I know. I loop it in with groceries so it’s not a big deal for me. Taxes are nice given you have fee free dollars but IRS can be slow giving your money back. Hyatt spend is important to me too so I can hopefully re-qualify for status or get some milestone rewards. Regardless your wife will get an annual free night so the card is worth having. Personally I bowed out of the +4x as it just seemed like too much stress. I knew I would be too tempted pushing the envelope with Amex and I would rather stay low. Sure 19x is better than 15x but I decided waiting until the end of the year for triple dip appealed to me more. If the +4 was still around by the end of the year, I likely would have added a charge card to my portfolio like you did.

All right, got my bro-in-law to sign up for an AMEX using player two’s AMEX Platinum referral (I can’t get AMEX Plat because I’m being pop-up boxed during app).

When do purchases become eligible for +4 points? Immediately after his approval (aka right now) or do I need to wait to get an email from AMEX or something? Have some large transactions (e.g. property tax) that I don’t want to pull the trigger on until I know the bonus is working.

(Also, loved this article Nick. It seems sacrilegious not to complete any sign up bonus but your logic tracks completely)

Amex sends an email a day or two after the approval to the referrer that you’re now earning +4

I actually called amex and ask this exact question. The rep told me the +4 applies after the person that got the referral gets their first statement on the card they applied for. Meaning it takes about a month and a half.

It never ceases to amaze me the ridiculously wrong answers that phone representatives can give you.

The email sent from Amex when you get your referral says you will start earning +4 the day the email was sent. That email sometimes takes up to 24-48 hours from the time when the person you refer is approved. Sometimes it is faster – when I used my wife’s link, she got the email almost instantly after I was approved. She started earning +4 that very day.

We have several cards from which we have referred to trigger the +4 offer. I can assure you that the “month and a half” or “first statement” answer they gave you is just completely wrong.

Unfortunately, that’s very common with phone customer service. I always half joke that I never ask a phone customer service representative a question that I don’t already know the answer to. They frequently either don’t know and just make something up or make an assumption about what makes sense in their mind or they are reading an answer off a computer screen with no experience actually doing what you’re asking about.

For an accurate answer about something like that, I always recommend asking someplace like our Frequent Miler Insiders group where you’ve got access to a large number of people who have actually done what you’re asking about and can answer based on experience rather than assumption. You’re infinitely more likely to get an accurate answer that way.

I’m so glad I commented on this random comment and you replied. You are ompletely right. I just looked through my email and found the email from amex about the +4 being added to my business platinum after my friend got approved from my link. It was dated the day after I sent out and after he got approved for his card.

Im in the middle of an expansion at work and was planning to use a 3x card for a big purchase instead of my plat since the rep told me the +4 wasn’t active on my platinum yet. Thank you for saving me from loosing 20k MR points.

I actually got a request to rate the service I got from “Debora” so maybe I should let them know they are giving wrong formation.

When spend capability approaches infinite none of these things are mutually exclusive. I sort of hope this article is written for an audience you’re not a member of. I spent $6k today before lunch without buying supplements or really even knowing what I’m doing. Anyway.

How on earth can you spend THAT much? I am sure there are som deals out there that I am not aware of. It kind of sucks that back in the days all these deals were blogged about in the open. For you average reader like me. Having 4x with a few thousand dollars of spend will mean almost nothing. An extra 2-3% over the standard cashback card? I mean you have to scale out and without manufactured spend that avenue is very limited. (unless you have a wedding coming up smh)

“unless you have a wedding coming up smh”

Or a car purchase. Or a home improvement project. Or kids in college with tuition. Or taxes to pay. Or a big vacation to book. Or a holiday party to plan. Or rental properties that need maintenance. Or another type of business. Or you’re having a baby or other expensive medical procedure. Or you’re upgrading to an energy efficient HVAC system and getting most of it rebated by the local power company (as one member of Frequent Miler Insiders recently posted about). Or you’re willing to resell some stuff. Or you have family members who will let you pay some of their bills on your cards (we recently paid school taxes for a couple of family members, one of whom owns a couple of rental properties — they paid us and we paid the taxes to earn rewards). Or a lot of other situations.

There are a lot of reasons you might have more than a few thousand dollars worth of spend. I one hundred percent understand that none of those may apply to you and as such you may not be interested in the +4 promo, but at least one or two of them apply to many readers to say nothing at all of MS.

One quick math correction — you equated +4 with an extra 2-3% over a cash back card, but remember that the referral promo adds 4x on top of what your card ordinarily earns. Assuming you value Membership Rewards points at least at 1.1c per point (the value at which they can be redeemed for cash via Schwab), this promo adds 4.4% on top of whatever you ordinarily earn. That’s an incredible addition on top of both existing bonus categories (think 8.8% back total on dining and US Supermarkets with the Amex Gold card or 9.9% back on flights and hotels at Amex Travel with a Platinum card, etc).

In a game where 2.625% cash back everywhere is considered an excellent cash back deal, Amex is blowing the lid off of it with a base level of 6.6% back on the Blue Business Plus with this +4 promo and lots of better opportunities as outlined here.

You don’t really have to scale it far for the difference to add up. If you’re using a card that earns 2.625% back everywhere, that’s $26 per $1,000 spent. With the Blue Business Plus you could be earning 6x everywhere with this promo and redeeming via Schwab for 6.6c per dollar spent, which is $66 cash back per $1,000 spent. That’s forty bucks more for every thousand you spend — 2.5 times as much as you’d earn with what is generally considered the best cash back return for unbonused spend.

In my opinion, that’s huge.

Nick wrote about his he’s going to knock out $25k of spend by buying a car. I know people who could easily make all the spend that Nick has lined up on food and beverage alone. And others who could make it on reimbursable business travel. For me, some heading system repair and home heating fuel will cover about $10k; auto maintenance maybe $2k; dentistry and medical for a family of four a few k. And, as a schedule C earner I always have the option of pissing tax with a 2% fee — 100% worth it if I’m earning 19 MR points per dollar (although I’ve never yet had to resort to paying fees).

LOL not even a wedding or car. We just spent $5k total on ours. The car I bought in 2020 cost under $4k (*did* use my biz plat tho!)

I live in an area where MS isn’t the best and I got burned by KF, there are still some opportunities in buying groups and bank bonuses, tho not like the good ol days. So it is prudent to be intentional about signup bonuses. Wish there were more blogs still like TIF…it’s hard for me to relate to posts that are v casual about spending the big buxx

Sometimes an offer comes up that you didn’t anticipate. I’m in a similar boat with the Hyatt personal card, was gonna try for globalist especially once the biz version was introduced, but now just focused on the initial bonus since the Venture X and new Chase biz came up (got the FNBO biz in there too for quick $$). You know what tho? In the end you are still profiting. I’ve had incredible travel experiences and now saving money, that 100% wouldn’t have been possible without churning. It’s still a win, don’t beat yourself up too badly.

Depending on your spending a lot of cards make no sense beyond sign up/retention bonuses. I thought Blue Cash Preferred wasn’t bad but with my limited spending on groceries and gas, it isn’t worth $95 so that will go next.

I already got rid of the Hyatt, Marriott cards, Green card, a business card and some others over the last 2 years.

Due to a lack of travel, and never a big traveller, I have probably 1.5-2M points between Chase, Amex, BA and AA. That is plenty for me with an occasional big bonus.

Isn’t Amex’s regular referral offer of 30k, 25k, 20k or even 15k MR without spend, a better offer than this (4X bonus upto 25k MR)? Assuming 2X return, you’d get at least 12.5k (TY, UR, AR etc.) points with 6.25k spend plus whatever MR you got without spend on the referee (?) card. If so, I’d wait until after 12/1 to refer my P2.

I don’t think I follow what you are saying. What do you mean by assuming 2X return?

Maybe what you’re missing is that the +4 is in addition to whatever you ordinarily earn for spend. So, for instance, if you use your Blue Business Plus card to refer a friend, you’ll then earn both the normal 2x return on spend *plus* earn 4 more points per dollar spent.

True that you will need to dedicate spend to this to make it better than earning 15K or 20K or 30K for no spend, but not that much money and you can refer from a card that you are ordinarily using anyway.

You don’t have to spend much to beat even the best old referral bonuses. If you’ll spend $7,500 or more on the card with the +4 offer, you’ll earn more than 30K points — the biggest regular Amex referral offer we’ve had in my household. And we have the opportunity to earn up to 100K from a single referral.

I’m not sure where your ThankYou points come into the calculation — I guess you’re somehow discounting the +4 by what you would earn by spending on the Double Cash instead? But that doesn’t make sense. If you refer someone from the Blue Business Plus, you’re going to earn the same 2x base points *plus also earn 4 more points per dollar spent*.

There is also the advantage that under the normal referral bonuses, you’ll get a 1099 and owe tax, whereas since this is additional points per dollar spent I expect it will be treated as a rebate and not taxable (I am not a tax expert, so consult with your own CPA on that).

Am I missing something that you’re arguing?

Oh you’re right, for some reasons I thought it’s up to 25k bonus points, it’s actually 25k in spend! So, the real concern would be to have enough organic spend (I’m sure RAT will be checking) to beat the regular 25k/30k offer etc. And another great point you mentioned – very unlikely to get a 1099 with this offer.

How do you read the offer, does the referred need to apply by 12/1, or needs to be approved as well?

Nick, did you ever explain why you applied so soon for the Amex Platinum card when you could have waited a few more weeks and had better timing for better use of credits?

I completely forgot to explain! It was the Carnival cruise deal that I wrote about last week (the matching offer for a “free” cruise). We wanted to book two different European cruises that would each be about $1500 for our family of four after the matching and so we wanted to use the $400 back on $1500 Amex Offer twice, but I didn’t have it on an Amex card with good travel protections (and trip cancellation / interruption seemed important to me because I don’t know what’s going to happen between now and then).

Obviously I could have booked with a Chase Sapphire Reserve or Ritz card for good travel protections, but to get both good travel protections and the $400 back via Amex Offer, I figured I would need a Platinum card (we didn’t see the $400 back offer on all of our cards, but it was on all three of my wife’s Platinum cards and also on another family member’s Platinum card).

My wife could only sync the offer to one card, so I figured I needed to open a Platinum card to stack. There was some gamble in whether or not I would get the Amex Offer, but I figured it was a safe-ish bet since it was on all of the other Platinum cards in the family. And I didn’t want to wait until after I published the post because we wanted a specific sailing and I wasn’t sure if that cruise would still be available if I waited until December. Since I stood to get $400 back from the Amex Offer, I figured that negated the $400 I would be missing in airline fee incidentals and FHR credits.

However, that all fell apart: I didn’t get that Amex Offer on my Platinum card and when my wife’s match came though it was only for an interior room, not an ocean view….so we didn’t end up booking it. There goes my entire justification for applying early. And if I had waited, I would stand to potentially get $400 more in airline fee and FHR rebates, so if I’d have just booked the $1500 cruise on the CSR, the net result would have been about the same. Ooops.

However, the +4 offer comes in for the save: this offer had to be triggered before 12/1, so I couldn’t have waited a lot longer to apply. I probably could have waited until now.

Ok, you win. My timing was bad 🙂

Great reply!

If it’s any solace, using that many FHR credits can be a pain I’m sure you could do without. I sure can’t find a way to use all mine!

Thanks for the thorough explanation, Nick! I was simply curious about it because you had mentioned it would be in a future post (and I read all FM posts, but didn’t find the explanation post!). So yes thanks so much for the clarification; it really helps to see how the true points/miles geniuses think! And yes, luckily the +4 offer makes up for the not-so optimal timing 😀

Quick follow up question: Do you think if I applied now, would the second annual fee be due January 2023?

Try your friend Simon for the Hyatt card.

See my response about this below.

I asked this on the Insiders group on Facebook, but repeating here for more data points:

Has anyone with the Resy Amex Platinum seen a bonus offer for adding authorized users? Asking because we’ll be pulling the trigger on this offer for P2 (assuming no denial) this week and I will want to give up my own Platinum card (if there’s no retention benefit) and become an authorized user on my wife’s — and would prefer to do that under an extra-points-for-authorized-user offer.

Yes, I got the Platinum through Resy in early July and was sent an authorized user offer about 4 months later – 20K points after the AU spends $2K in 6 months.

Nice! Good data point.

Aren’t you off by 1x on that authorized user card your wife signed you up for? $2k spend will net 22,000 points, or 11x (not 10x) effective return.

Also, if you completed the $3k spend on the Hyatt card and earned the 30K points, I’d call that already earning the bonus. The 2x points are irrelevant in this (or, really, any) market and the 15K certificate is a recurring feature of the card.

I sure am off by 2K points. BOOM! Thank you.

Yeah, I won’t agree on the Hyatt card. The free night at 15K spend is an additional free night cert, but I agree that the 2x points are irrelevant in this market. That’s the point here — it’s a poor bonus that just doesn’t hold a candle to all the points Amex is passing out right now.

Personally I would do Simon since you know that doesn’t work with Amex. That’s what I did with my hyatt card this year. But if you choose not to, at least you get a free night every renewal year so all is not lost. Plus hopefully chase comes out with more bonus spend offers. My hyatt card used to never get any targeted offers. But when they switched it to the new card early this year, and I started spending a ton for the new perks, I finally got targeted. So maybe don’t sock drawer it.

Yeah, time / capacity just becomes an issue. You’re right that I could do Simon with Hyatt (and not with Amex), but with a lot of volume / capacity on Amex, I only have but so much time / float / mental bandwidth to spread around. It’s not that I physically couldn’t meet the Hyatt spend, it’s that any time I’m spending buying Simon cards and running around to liquidate them is time I could be spending figuring out how to spend more on Amex cards at much better return. Any float I’m doing on Simon cards could be better floated on Amex cards.

Yeah I totally can see that. I’ve been doing some pajama MS and my float has gone beyond my real comfort zone. So I’ve been taking a little break especially since I need to catch up on my accounting for friends and family that help. In fact I want to pull the trigger on Resy soon with a family member but I’m hesitating a bit bc it still requires some work. I enjoy our hobby but sometimes it’s good to sit some stuff out. I still haven’t decided for sure tho.

I almost jumped at the 4X add on bonus but for me it was too much of a spend on the card we would refer so not much chance of meeting the spending bonus for the welcome bonus. Really it came down to bad timing as I had finished the Citi offer right as I got the Platinum Card.

That being said, I do concur the Platinum Card offer from Resi is just amazing. I cant wait for it to post after a recent vacation, the 15X at all restaurants I am sure will add up.

Nick, buddy, I’m here for ya! Just hop on over to the Simon website and buy $25K of $1,000 VGC’s with your Hyatt CC and FedEx them to me and I’ll liquidate them for you! Right now they are offering a substantial discount on fees as well. Look at the money you’ll save! If this isn’t enough help you can just repeat the process and I’ll gladly assist you further. I’m doing you a solid here and I know you won’t forget it!

Thanks for your generous offer :-).

It’s just coming down to a situation where I only have but so much time / capacity and Amex is pouring points by the bucketload. Obviously I’m not using them for Simon, but if I’m putting time and effort into earning the Amex points it limits how much extra time and effort there is for Simon. So thanks again for your offer, but I think I’ll pass on FedExing those cards to you :-).

Ok, but just remember, I’m here for you!

Nick, I must admit you’re being tone-deaf about these referral bonuses. Those of us in the real world, who cannot just drop a referral link out there for 50,000 readers to feast on, do not appreciate your bragging about how wonderful your life is now that you can benefit from the +4 program. I used up all my goodwill a few years back after I heard back some of my from my relatives that they did not appreciate the referral (some of them feel that it triggered more SPAM from Amex; maybe yes, maybe no).

That said, the tidbit you offered about adding a Gold user to my Plat Amex is news to me and I do appreciate that. However, that probably deserves its own post rather than getting buried in your tedious post about all the mental gymnastics you’re doing at the gas pump, the check-out, etc. My head would explode if I had to live my life like that.

Good lord, biting the hand that feeds you!

I strongly suspect that the large majority of people reading are easily capable of taking advantage of the Amex +4 offer by referring in their own household. Is there some portion of the audience that has trouble finding a second player? Sure, but I bet it’s a minority (and a small one at that). Using this offer is definitely not something that’s restricted to bloggers. Dollars to donuts Nick’s triggering referral was a personal one and not through the blog (I think he states this directly).

There are referral offers that bloggers (including those here) have an extra ability to take advantage of — mostly the “get $15 for referring friends to a shopping service” type offers and also “fee-free payment” offers on Plastiq (or however the heck it’s spelled) which I bet makes up a fair amount of MS liquidation for some of the writers. But they rarely mention them, and never tout them as a major vector for points earning by people without access to their large referral base.

This is a game to those who enjoy it, so the (relatively lightweight) “mental gymnastics” at the pump are fun, not a cause of head-explosion. Just like it appears that the fault-finding, which would be soul exploding to me, is an enjoyable pastime for you.

As Larry notes, I opened the Business Green card through my wife’s referral link specifically to trigger +4 on her Gold card. Yes, I am very fortunate to be a blogger and be able to share my referral links widely, but if I weren’t my wife and I would continue opening as many Amex business charge cards as they would allow using each other’s links to trigger +4 on each of the cards we wanted. It also helps to make friends with others who are into this hobby because then you could achieve the same type of effect with others as well.

What makes this referral bonus special is that it only takes one referral to get the +4, so you don’t need a network of 50,000 readers, you just need a second player. Not everybody has a second player, but then like I said it helps to make friends with people who are interested in this because you are not likely to make someone who isn’t interested get interested. It is worth the time invested in making a second-player connection.

Much to Larry’s point, there are a lot of things I don’t write much about because they won’t apply to a wider audience, but the +4 is something that can be triggered relatively easily for most people. We talked about ways to do that during the podcast to which I linked.

In terms of a post about adding a Gold authorized user to a Platinum card, we did post about that back in June.

https://frequentmiler.com/20k-membership-rewards-bonus-with-new-authorized-user-and-2k-spend-targeted/

Why not use PayPal to send $10K to your wife on the Hyatt card? The $300 fee should be worth the cat 1-4 plus 20K Hyatt points. And you wouldn’t be cannibalizing any of your true spend away from Amex.

I’ve always avoided using PayPal for stuff like this not only for its fees but because I find PayPal useful and I don’t want my account shut down / money locked up there. But your general idea makes sense that it would be worth the fees to do that sort of thing.

I have used PP to help meet the minimum spend on 3-4 Chase cards in the last few years and never had a problem. Good problem to have deciding which boatload of points/SUB’s to pursue!

At $300 it would be worth it, but you’d be getting maybe about $500 of value depending on how you redeemed (I know you could do a lot better, I rarely manage to). Value for money, but not a slam dunk in my mind.