NOTICE: This post references card features that have changed, expired, or are not currently available

Note that the offers mentioned in this post were current at the time of writing but have since expired. The temporary credits ended at the end of 2020 as noted within the body of the post. For current offer information, see our Best Offers page.

Now that Amex has announced a number of awesome, but temporary enhancements to their Platinum cards, many are wondering if it’s time to get one.

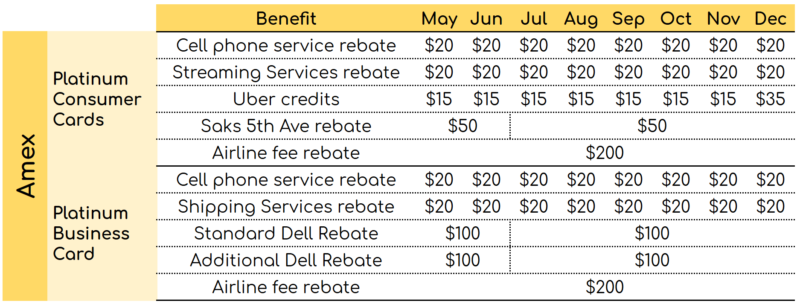

In addition to the usual perks that the Platinum cards offer, in the year 2020 only, Amex has added the following additional perks (note that these expired at the end of 2020):

- Consumer Platinum Cards (Amex Platinum Card, Morgan Stanley Platinum, Schwab Platinum)

- Up to $160 in cell phone service rebates

- Up to $160 in steaming service rebates

- Business Platinum Card

- Up to $160 in cell phone service rebates

- Up to $160 in shipping service rebates

- Up to $200 in Dell rebates

Are these sweeteners enough to justify the Consumer Platinum’s $550 annual fee (the annual fee has increased to $695 since the time of publication) or the Business Platinum’s $595 fee? If we don’t already have these cards, should we get them?

Existing Customer Recommendation: Keep

If you already have a Platinum card, my recommendation for most people is not to cancel it now. Instead, do your best to get full value from all of the available credits.

Additionally, Amex is offering incentives to many cardholders to renew. Overall, it’s a good time to be a Platinum cardholder.

Consider Dropping Authorized Users

While it makes sense for most Platinum cardholders to keep their cards for now, I don’t think it makes sense to keep paying for authorized users. When your next annual fee comes due, you may want to drop the authorized users in order to reduce the annual fee (one exception is the Morgan Stanley Platinum card which offers 1 authorized user for free).

The reason I’m not bullish on Platinum authorized user cards is that none of the currently useful credits apply to these cards. All of the authorized user card benefits are tied to travel. Authorized users get lounge access, elite status in a number of programs, and other miscellaneous travel related benefits (see our complete guide for details). As long as your authorized users aren’t traveling, those perks aren’t worth much.

For the record, here are the annual fees for authorized users:

- Business Platinum: $300 per year for each Platinum employee card

- Morgan Stanley Platinum: First Platinum authorized user card is free. Add up to 3 more for $175 per year.

- Other consumer Platinum cards: $175 per year for up to 3 Platinum authorized users.

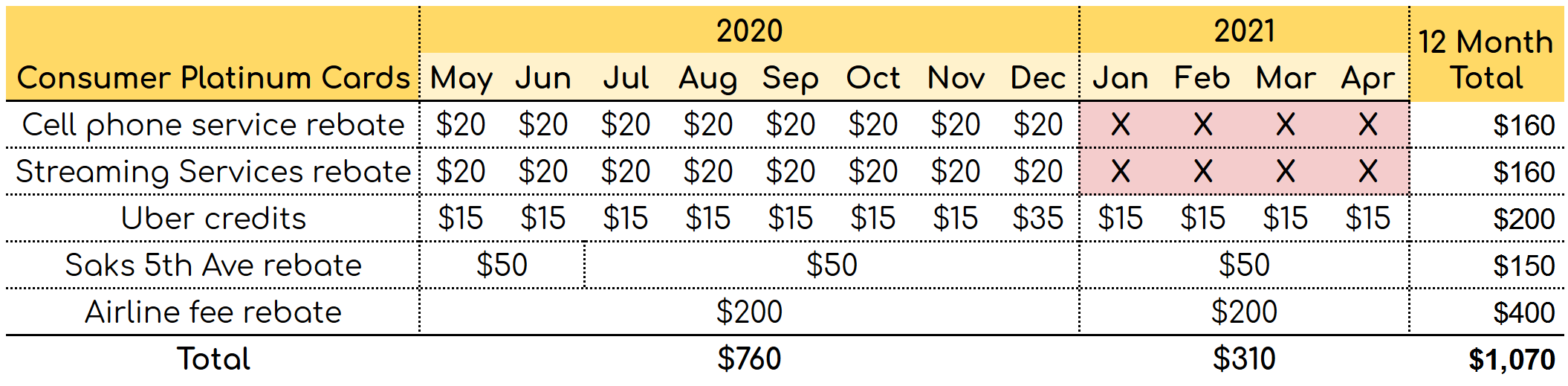

12 Month’s of Credits (over $1,000 face value)

If you sign up now (early May 2020) for a new Platinum card, you can get at least 12 months of rebates by the time the next annual fee comes due. At that point, you can decide whether to keep the card, or downgrade, or cancel to avoid the next annual fee. So, when deciding whether to pick up a Platinum card now, it’s worth looking at 12 months of potential credits…

Consumer Platinum: Up to $1,070

- Cell Service Rebate (2020 only): Up to $160

- Streaming Service Rebate (2020 only): Up to $160

- Uber Credits: Up to $200 ($15 monthly and $35 in December)

- Saks 5th Ave Rebate: Up to $150 ($100 in 2020 + $50 in first half 2021)

- Airline Fee Rebate: Up to $400 ($200 in 2020 + $200 in 2021)

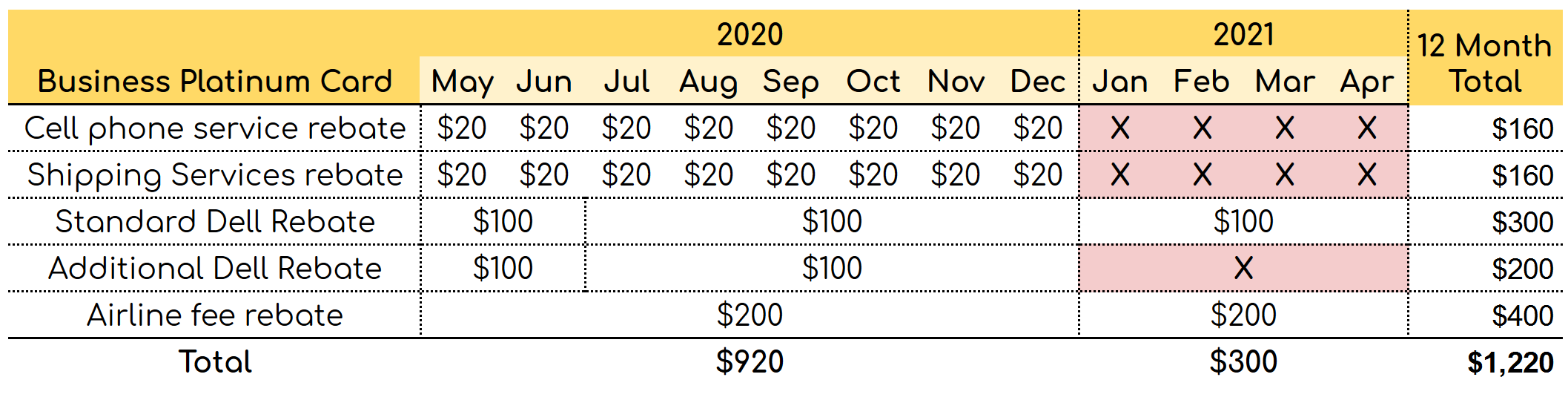

Business Platinum: Up to $1,220

- Cell Service Rebate (this year only): Up to $160

- Shipping Service Rebate (this year only): Up to $160

- Standard Dell Rebate: Up to $300 ($200 in 2020 + $100 in first half 2021)

- Additional Dell Rebate (this year only): Up to $200

- Airline Fee Rebate: Up to $400 ($200 in 2020 + $200 in 2021)

How much are the rebates worth, to you?

While Amex Platinum cards are absolutely loaded with great travel perks, the only perks worthwhile when not traveling are those that offer statement credits. At full face value, those credits are worth quite a lot, as shown in the previous section:

- Consumer Platinum: Up to $1,070

- Business Platinum: Up to $1,220

Those numbers are eye-popping and can easily justify signing up for Platinum cards for these credits alone even if you don’t consider welcome bonuses. But, you shouldn’t value these credits at face value.

Even if you manage to get all of the offered credits, you have to pay up front for them (in the form of the annual fee). And you almost certainly will have to sacrifice some other rewards. For example, by paying your cell phone bill with a Platinum card, you may be giving up 5X rewards with a Chase Ink Cash card.

The best way to value credit card rebates is to estimate how much you’d be willing to pay for them individually, up front. For example, if someone came to you and said “how would you like to buy $200 in Uber credits, dolled out $15 per month ($35 in December), for only $200?” You’d be crazy to buy that. Why spend $200 up front for the chance of getting $200 in value? You wouldn’t. You shouldn’t. The only reason to pay for credits up front is if you would get a significant discount.

Greg’s Valuations

Here is how much I would be willing to pay for each type of credit:

Consumer Platinum (Greg’s Valuations)

- Cell Service Rebate (up to $160): I’d pay $140

This is super easy. Each month when I get the AT&T email saying my bill is ready, I’ll log in and pay $20 with each Platinum card. The remaining balance will be auto-paid with my Chase Ink Cash card for 5X rewards. - Streaming Service Rebate (up to $160): I’d pay $145

I’ve already switched my YouTube TV bill to charge to my Platinum card. No more work is required to get the full value of this rebate. - Uber Credits (up to $200): I’d pay $100

Uber credits can be used for Uber Eats food delivery, so that’s great. But since I also have DoorDash credits thanks to my Sapphire Reserve card and GrubHub rebates thanks to my wife’s Amex Gold card, I don’t always use up all of the Uber Eats credit. - Saks 5th Ave Rebate (up to $150): I’d pay $75

I like using these credits to buy gifts for family members, but I certainly wouldn’t pay full price. - Airline Fee Rebate (up to $400): I’d pay $300

I find it pretty easy to earn these rebates. Even though I’m not traveling soon, I’ve been able to earn the rebates for distant future travel. I suspect that most readers will value this much lower.

My Consumer Platinum 12 Month Value: $760

Business Platinum (Greg’s Valuations)

- Cell Service Rebate (up to $160): I’d pay $140

This is super easy. Each month when I get the AT&T email saying my bill is ready, I’ll log in and pay $20 with each Platinum card. The remaining balance will be auto-paid with my Chase Ink Cash card for 5X rewards. - Shipping Service Rebate (up to $160): I’d pay $80

I rarely ship stuff. Yes, I could buy $20 in forever stamps each month (and probably will), but I already have more forever stamps than I know what to do with. Who sends letters anymore? On the other hand, I’m sure I could recoup money by selling those extra stamps. But that’s a hassle. - Standard Dell Rebates (up to $300): I’d pay $200

The Dell credits come in very handy when I need them (and there are many things one can buy with them), but I often find myself buying things that I don’t need just to use up the credits. - Additional Dell Rebates (up to $200): I’d pay $130

- Airline Fee Rebate (up to $400): I’d pay $300

I find it pretty easy to earn these rebates. Even though I’m not traveling soon, I’ve been able to use them for distant future travel. I suspect that most readers will value this much lower.

My Business Platinum 12 Month Value: $850

Given my valuations, both the consumer Platinum card and Business Platinum card make sense for me to pick up right now. I cover other considerations (welcome bonus, whether you’ve had the card before, etc.) in later sections of this post.

Your Valuations

Fill out the following worksheet to determine how much you’d be willing to pay for each Platinum card’s rebates:

Consumer Platinum (Your Valuations)

- Cell Service Rebate ($20/month up to $160): ______

This probably won’t work with Google Fi, but should work with most major cell service providers. - Streaming Service Rebate ($20/month up to $160): ______

Works with Amazon Music Unlimited, Apple Music, Apple TV+, AT&T Now, Audible, CBS All Access, Disney+, ESPN+, Fubo TV, HBO Now, Hulu, iHeartRadio, Kindle Unlimited, Luminary, MLB.TV, NBA League Pass, Netflix, NHL.TV, Pandora, Prime Video, Showtime, Sling TV, SiriusXM Streaming and Satellite, Spotify, Stitcher, YouTube Music Premium, YouTube Premium, and YouTube TV - Uber Credits (up to $200 across rest of 2020 and first half 2021): ______

Uber credits can be used for Uber Eats food delivery, but that’s not worth much if you don’t have Uber Eats delivery in your area. - Saks 5th Ave Rebate (up to $150 across 2020 and first half 2021): ______

Rebates can be earned for in-store or online purchases. - Airline Fee Rebate (up to $400 across 2020 and 2021): ______

Given that airline gift cards no longer count, it takes more creativity than ever before to get value from these rebates when not traveling. I suspect that many readers will value this at or close to $0.

Your Consumer Platinum 12 Month Value: ________________

Business Platinum (Your Valuations)

- Cell Service Rebate ($20/month up to $160): ______

This probably won’t work with Google Fi, but should work with most major cell service providers. - Shipping Service Rebate ($20/month up to $160): ______

- Standard Dell Rebates (up to $300 across 2020 and first half 2021): ______

See this post for details about the many types of things that can be bought through Dell. - Additional Dell Rebates (up to $200, 2020 only): ______

- Airline Fee Rebate (up to $400 across 2020 and 2021): ______

Given that airline gift cards no longer count, it takes more creativity than ever before to get value from these rebates when not traveling. I suspect that many readers will value this at or close to $0.

Your Business Platinum 12 Month Value: ________________

None? One? Or Two?

If your valuations come out as high or higher than the annual fee for both the consumer and business Platinum cards, the question you should ask yourself is whether it makes sense to get both.

In my case, I value 12 months of credits at $760 (Consumer Platinum) and $850 (Business Platinum). When I compare to each card’s annual fee, I can see that both cards make sense for me:

- Consumer Platinum: $760 value is greater than the $550 annual fee

- Business Platinum: $850 value is greater than the $595 annual fee

How to interpret those numbers: Keep in mind that the valuations shown here represent how much I’d be willing to pay for the credits. For example, I’d be willing to pay $760 for the chance of getting $1,070 in 12 months worth of Consumer Platinum credits. If my valuation had been as low as $550, it would still make sense for me to get a consumer Platinum card. If my valuations totaled less than $550, though, it wouldn’t make sense.

Sign up new or upgrade?

If you have the Amex Green Card or Amex Gold Card you should be eligible to upgrade to the consumer Platinum Card. Similarly, if you have the Business Green Card or Business Gold Card you should be eligible to upgrade to the Business Platinum Card.

If you upgrade, you’ll be eligible for all of the credits discussed in this post, but of course you’ll lose the benefits associated with the old card. For example, if you upgrade from the Amex Gold Card, you’ll no longer earn 4X at US Supermarkets (up to $25K in purchases, then 1X) or 4X at restaurants.

The primary reason to prefer signing up new is to get a welcome bonus. But if you’ve ever had that same version of the Platinum card before, you won’t be eligible for a new cardmember bonus. Also, it’s possible that Amex would offer you a bonus to upgrade. To find out, call the number on the back of your Green or Gold card to ask.

One downside to signing up new for a consumer Platinum card is that it adds another account to your credit report. This can actually help your credit score in the long run, but it will also add to your 5/24 Status which can make it harder to qualify for new Chase cards. Fortunately, the Business Platinum doesn’t show up on your credit report and so it won’t hurt your 5/24 Status to sign up for that card.

Signing up new is usually the better way to go if you can qualify for a new cardmember bonus. But if you don’t qualify for a bonus, or if you are offered a good upgrade bonus, or if you want to avoid adding to your 5/24 Status (for consumer Platinum cards only) then upgrading may be the better way to go.

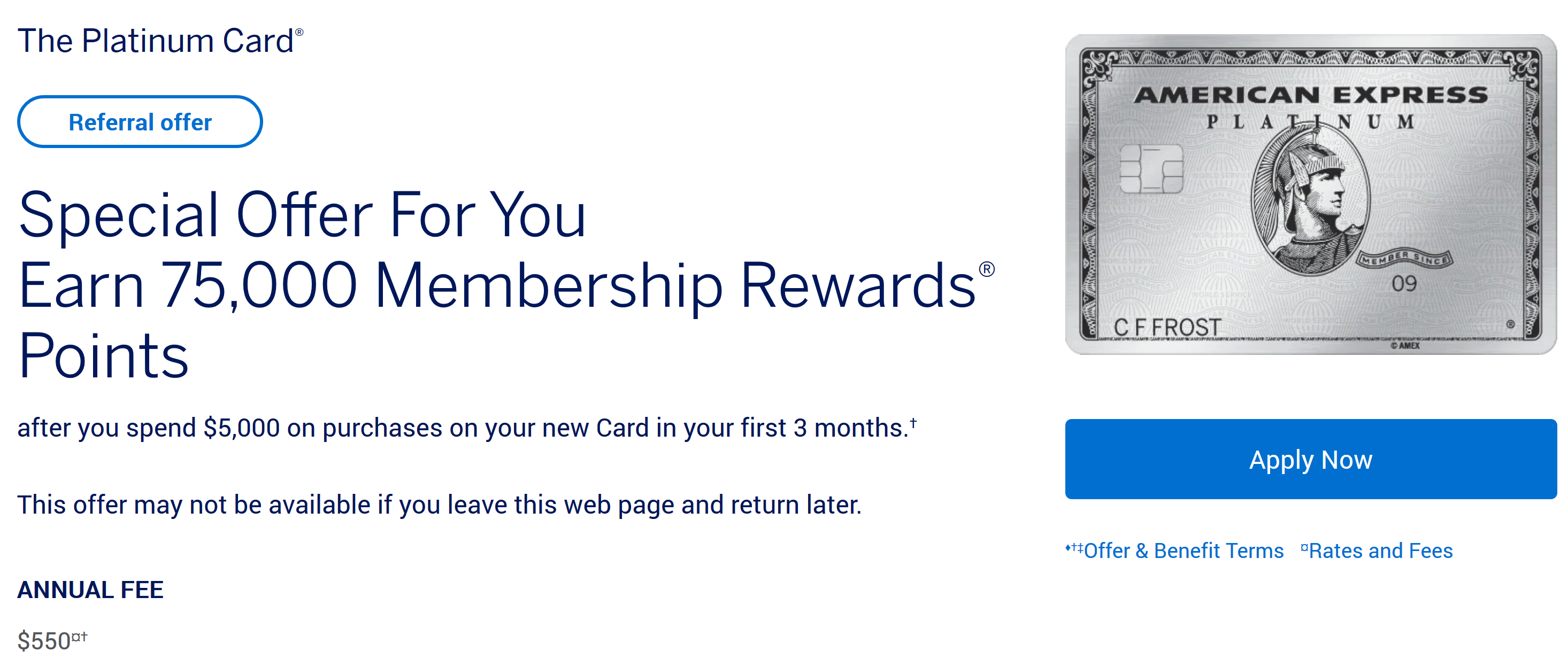

Welcome Bonus Offers

The standard welcome bonuses available today for consumer and business Platinum cards are shown below (this will update automatically when offers change). Keep in mind that you are not eligible for these offers if you’ve had the same exact Platinum card variant before. However, you can qualify if you’ve had a different one. For example, if you’ve had the regular Platinum card before, you can still qualify for the bonus on the Schwab Platinum card.

| Card Offer |

|---|

ⓘ $2217 1st Yr Value Estimate$200 airline incidental fee credit for select airline only valued at $140, $200 Uber credit ($15 per month, $35/December) valued at $100, $600 Fine Hotels + Resorts® credit valued at $300, $300 Digital Entertainment Credit ($25 per month) valued at $150, 400 Resy credit ($100 per quarter) valued at $85, $120 Uber One credit ($10 per month) valued at $48, $300 Lululemon credit ($75 per quarter) valued at $150 Click to learn about first year value estimates 150K points Non-AffiliateThis is NOT an affiliate offer. We always present the best offer even when it means less revenue for Frequent Miler 150K after $12K spend in first 6 months. Terms apply. (Offer Expires 7/8/2026)$895 Annual Fee This card is only available to clients that maintain an eligible Schwab brokerage account. Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Recent better offer: None |

ⓘ $2217 1st Yr Value Estimate$200 airline incidental fee credit for select airline only valued at $140, $200 Uber credit ($15 per month, $35/December) valued at $100, $600 Fine Hotels + Resorts® credit valued at $300, $300 Digital Entertainment Credit ($25 per month) valued at $150, $300 Lululemon credit ($75 per quarter) valued at $150, $120 Uber One credit ($10 per month) valued at $48, 400 Resy credit ($100 per quarter) valued at $85 Click to learn about first year value estimates 150K Points Non-AffiliateThis is NOT an affiliate offer. We always present the best offer even when it means less revenue for Frequent Miler 150K after $12K spend within first 6 months. Terms apply. (Offer Expires 7/8/2026)$895 Annual Fee Information about this card has been collected independently by Frequent Miler. The issuer did not provide the details, nor is it responsible for their accuracy. Recent better offer: 150K after $8k spend in the first 6 months. (Expired 11/12/25) FM Mini Review: In my opinion, this is the best of the consumer Amex Platinum cards when you need two cards thanks to Morgan Stanley offering one free authorized user. Unfortunately you do need to have a Morgan Stanley account to apply. |

ⓘ $4163 1st Yr Value Estimate$200 airline incidental fee credit for select airline only valued at $140, $200 Hilton credit ($50 per quarter) valued at $150, $120 wireless credit ($10 per month) valued at $90, $150 Dell credit valued at $37.5, $600 Fine Hotels + Resorts® credit valued at $300 Click to learn about first year value estimates As high as 300K points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer You may be eligible for as high as 300,000 Membership Rewards® Points after spending $20k in eligible purchases on your new Card in your first 3 months of Membership. Welcome offers vary, and you may not be eligible for an offer. Terms apply. (Rates & Fees)$895 Annual Fee Recent better offer: 250K after $20K spend - no "as high as language" (expired 2/10/25) FM Mini Review: This card is absolutely loaded with high end perks. Depending upon your situation, those perks may be worth the annual fee or much more. Click here for our complete card review |

ⓘ $2605 1st Yr Value Estimate$200 airline incidental fee credit for select airline only valued at $140, $200 Uber credit ($15 per month, $35/December) valued at $100, $600 Fine Hotels + Resorts® credit valued at $300, $300 Digital Entertainment Credit ($25 per month) valued at $150, $300 Lululemon credit ($75 per quarter) valued at $150, 400 Resy credit ($100 per quarter) valued at $85, $120 Uber One credit ($10 per month) valued at $48 Click to learn about first year value estimates As high as 175K points ⓘAffiliateThis is an affiliate offer. Frequent Miler may earn a commission if you are approved for this offer As high as 175K points after $12K spend in the first 6 months. Welcome offers vary and you may not be eligible for an offer. Terms apply. Rates & Fees$895 Annual Fee Recent better offer: Up to 175K points after $8K spend in the first 6 months. (Expired 2/4/26) FM Mini Review: This card is absolutely loaded with high end perks. Depending upon your situation, those perks may be worth the annual fee or much more. |

Better Offers?

Business Platinum

We’ve certainly seen better offers for the Business Platinum card in the past. As I write this, the current best offer is for a total of 85,000 points after $20K spend. Compare that to 100K points after $20K spend which has been common in the recent past.

But past offers didn’t include $160 in cell phone credits, $160 in shipping credits, and $200 in extra Dell credits. With that taken into consideration, I’d say that the 85K offer is way better.

Before you apply for this card, though, consider calling Amex to ask about offers for the card. Sometimes Amex makes better offers available over the phone.

Consumer Platinum

As I write this, 60K points after $5K spend is the best public offer for any of the three available consumer cards. That’s also the standard offer that has been in place for quite a while now.

While I don’t know of any ways to get a better offer for the Morgan Stanley or Schwab Platinum variants, there are several options with the standard Platinum card:

Consumer Platinum 125K Targeted Offer

Amex offers a way to check for pre-qualified offers. Through this website, some people have been targeted with an offer for 125,000 points after $5K spend. That’s incredible. Details here.

Consumer Platinum 100K Targeted Offer

Through the CardMatch Tool, people sometimes receive a targeted offer for 100,000 points after $5K spend. You’ll find a link to the tool here.

Try Another Browser 75K Offer

We currently list the offer for the Amex Platinum card as being 60K points after $5K spend. However, when I’ve clicked through the application link on our site from different browsers, I got different results. For example, when I clicked through our link yesterday from my Firefox browser I was surprised to find an offer for 75K points after $5K spend. From Chrome, though, I saw the standard 60K offer. I recommend clicking through from several different browsers to see if you get a better than 60K offer.

Conclusion

Whether or not it makes sense to pickup one or more Platinum cards today depends upon how much you value the statement credits each card offers. How much would you pay to get those credits if they were available individually for sale? Does the total add up to the annual fee, or more? If so, it makes sense to get the card.

In my case, both the consumer and business Platinum cards make sense. I already have a consumer Schwab Platinum card and I manage my son’s Business Platinum card. So, I’m already doing well with those credits. But I’m also planning on adding additional cards to the mix:

- Upgrade my Business Green Card to Business Platinum. I need to call Amex to ask whether I qualify for any upgrade offers. If not, I’ll do it anyway.

- Encourage my son to sign up new for the consumer Platinum card, especially if we can find that 75K offer again (but 60K would be OK too). 75K points plus more than $1,000 in statement credits is an awesome deal.

Get 2 ChatGPT Business seats for $25/mo total for 4 years! (probably won’t last)")

[…] your application: To snag $80 worth of streaming and wireless credits (up to $40 in November and $40 in December), you’ll need to apply right […]

[…] Is it time to get an Amex Platinum Card? […]

[…] the post “Is it time to get an Amex Platinum Card?” I showed that it not only makes sense to keep your Platinum card if you have one, but that […]

[…] Express recently added a couple of new credits on Platinum cards – $20 per month for wireless credits and $20 per […]

You mention it is not worth having Authorized Users right now. I agree, you pay extra for authorized user Platinum cards, and there are really no added benefits. One tip–you can downgrade a Platinum AU to a Gold card AU (which has no fee) and get a prorated refund. So if your AU’s are not up for a while, that is an option.

This is nice for your AU, since it will not count as a closed account, and you can upgrade them in 9 or 12 months without it counting as a new account for them. I called Amex, I they said a Gold Card AU (attached to your main Platinum account) can charge and utilize the streaming/cell credits, if that makes sense.

Great suggestion. Thanks!

What has been your strategy as of late to earn the airline rebates?

This is something that we don’t want to write up too explicitly because the card issuer reads these things and plugs up loopholes. Mostly this just requires creativity. I’m pretty sure we’ve discussed some techniques in our Frequent Miler on the Air series, but I don’t remember which episodes: https://www.youtube.com/playlist?list=PLp8T4WCju-UTwQquYpXA1aEAlYH4uo85r

Applied for personal Plat but got the AMEX pop-up. My guess is due to infrequent spend on existing AMEX cards. Currently putting spend on existing cards, will try again later this month (and in June if necessary).

anyone think we could split tender om phone bill between my personal Plat and my wifes plat?

Yes

@greg and @Nick Reyes can you do the same exact post but for Hilton $450 AF card? Thx

Yep, I probably will do so if Nick doesn’t beat me to it.

I was trying to cancel a different Amex card online but everytime I use the online chat I get an error. I much prefer Chase’s secure email system. They canceled my card within 24 despite warning me it might take longer. I’d rather not call in and get stuck on hold.

So you’re saying there is definitely value to be had even if you’re not earning a signup bonus.

So glad I ditched my Plat AMEX last summer as the AF climbed. Even with these new credits they’re still not worth it to keep the card. AMEX did nothing to keep my business, no retention offer at all, I don’t look back on the cancelation for one second.

Probably more beneficial after 6 months of stamps and post COVID19.

Stamps are still used and could probably be flipped or gifted to two groups that do mailings and included RSVP (which should be pre-stamped for weddings). Graduation announcements, and Wedding invitations, and then thank you notes, as well as holiday mailers.

So they could be gifted to newly engaged, find out if they will be doing printed invitations, could make a pragmatic gift, as well as a small token from the registry.

Donation (for tax purposes) or just gifted to a charity that targets Boomers that still mail letters and have a checkbook that they use. Charities often enclose a pre-stamped envelop to mail back that check

Grads (2021), Holiday mailings, and traditional wedding invitation, and pre-stampeed RSVP envelop (yeah I know that this is more Gen-X and Boomer parents thing than using social media or e-mail). Might be easier to flip the stamps if you know a wedding planner.

Saw an Amex offer for Envelops.com don’t know if it codes as Shipping.

Does anyone have any thoughts if the Chase Ink iPhone warranty would remain in effect after partially paying with AMEX to hit these credits?

I will be canceling my Platinum. About the only benefit I would use this year is streaming. Too bad they are dissing Google Fi cell plans.

Just cancelled mine since I am getting the cell phone benefit…